This is “In a Set of Financial Statements, What Information Is Conveyed by the Statement of Cash Flows?”, chapter 17 from the book Business Accounting (v. 2.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

Chapter 17 In a Set of Financial Statements, What Information Is Conveyed by the Statement of Cash Flows?

Video Clip

(click to see video)In this video, Professor Joe Hoyle introduces the essential points covered in Chapter 17 "In a Set of Financial Statements, What Information Is Conveyed by the Statement of Cash Flows?".

17.1 The Structure of a Statement of Cash Flows

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Describe the purpose of a statement of cash flows.

- Define cash and cash equivalents.

- Identify the three categories disclosed within a statement of cash flows.

- Indicate the type of transactions that are reported as operating activities and provide common examples.

- Indicate the type of transactions that are reported as investing activities and provide common examples.

- Indicate the type of transactions that are reported as financing activities and provide common examples.

The Importance of a Statement of Cash Flows

Question: Thus far in this textbook, the balance sheet and income statement have been studied in comprehensive detail along with the computation of retained earnings. By this point, a student should be able to access a set of financial statements (on the Internet, for example) and understand much of the reported information. Terms such as “FIFO,” “accumulated depreciation,” “goodwill,” “common stock,” “bad debt expense,” and the like that might have sounded like a foreign language at first should now be understandable.

Examination of one last financial statement is necessary to complete the portrait presented of a reporting entity by financial accounting and the rules of U.S. GAAP. That is the statement of cash flows. This statement was introduced briefly in an earlier chapter but will be covered here in detail. Why is it needed by decision makers? What is the rationale for presenting a statement of cash flows?

Answer: Coverage of the statement of cash flows has been postponed until now because its construction is unique. For this one statement, the figures do not come directly from ending T-account balances found in a general ledger. Instead, the accounts and amounts are derived from the other financial statements. Thus, an understanding of those statements is a helpful prerequisite when considering the creation of a statement of cash flows.

The delay in examining the statement of cash flows should not be taken as an indication of its lack of significance. In fact, some decision makers view it as the most important of the financial statements. They are able to see how corporate officials managed to get and then make use of the ultimate asset: cash. The acquisition of other assets, the payment of debts, and the distribution of dividends inevitably leads back to a company’s ability to generate sufficient amounts of cash. Consequently, presentation of a statement of cash flows is required by U.S. GAAP for every period in which an income statement is reported.

To reiterate the importance of this information, Michael Dell, founder of Dell Inc., states in his book Direct from Dell: Strategies That Revolutionized an Industry (written with Catherine Fredman): “We were always focused on our profit and loss statement. But cash flow was not a regularly discussed topic. It was as if we were driving along, watching only the speedometer, when in fact we were running out of gas.”Michael Dell with Catherine Fredman, Direct from Dell: Strategies That Revolutionized an Industry (New York: HarperBusiness, 1999), 47.

The income statement and the statement of cash flows connect the balance sheets from the beginning of the year to the end. During that time, total reported net assets either increase or decrease as does the entity’s cash balance. The individual causes of those changes are explained by means of the income statement and the statement of cash flows.

The purpose of the statement of cash flows is virtually self-evident: It reports the cash receipts (cash inflows) and the cash disbursements (cash outflows) to explain the changes in cash that took place during the year. However, the physical structure of this statement is not self-evident. As illustrated previously, all cash flows are classified within three distinct categories. Coverage here is designed to demonstrate the logic of this classification system and the method by which the reported numbers are derived.

Cash and Cash Equivalents

Question: Because current assets are listed in order of liquidity, most businesses present “cash and cash equivalentsShort-term, highly liquid investments with original maturities of ninety days or fewer that can be readily converted into known amounts of cash.” as the first account on their balance sheets. For example, as of December 31, 2010, Ball Corporation reported holding cash and cash equivalents totaling $152.0 million. This same terminology is used on Ball’s statement of cash flows which explains the drop of $58.6 million in cash and cash equivalents that took place during 2010. What constitutes cash and what are cash equivalents?

Answer: Cash consists of coins, currencies, bank deposits (both checking accounts and savings accounts) and some negotiable instruments (money orders, checks, and bank drafts). Cash equivalents are short-term, highly liquid investments that are readily convertible into known amounts of cash. They are so near their maturity date that significant changes in value are unlikely. Only securities with original maturities of ninety days or fewer are classified as cash equivalents. Cash equivalents held by most companies include Treasury bills,A Treasury bill is a popular U.S. government security with a maturity date of one-year or less. commercial paper,The term “commercial paper” refers to securities issued by corporations to meet their short-term cash needs. and money market funds.

For the past few years, FASB has been considering the elimination of the cash equivalents category. If a change is made, such assets (other than cash) will likely appear on the balance sheet as temporary investments. As with all such debates, both pros and cons exist for making such an official change. For simplicity purposes, cash will be used in the examples presented throughout this chapter. However, until new authoritative rules are passed, accounting for cash equivalents is the same as that for cash.

Test Yourself

Question:

Which of the following assets is least likely to be considered a cash equivalent?

- Treasury bills

- Commercial paper

- Money market funds

- Corporate bonds

Answer:

The correct answer is choice d: Corporate bonds.

Explanation:

Treasury bills, commercial paper, and money market funds are all considered to be cash equivalents as long as they can be converted into cash and had an original maturity of ninety days or fewer. Most corporate bonds have maturity dates much longer than ninety days, often many years.

Cash Flows from Operating Activities

Question: For reporting purposes all cash flows are classified within one of three categories: operating activities, investing activities, and financing activities. What transactions are specifically identified as operating activities?

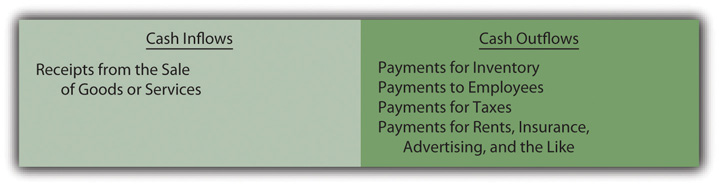

Answer: Operating activitiesA statement of cash flow category used to disclose cash receipts and disbursements arising from the primary activities of the reporting organization. generally involve producing and delivering goods and providing services to customers. These events are those that transpire on virtually a daily basis as a result of the organization’s primary function. For a business like Barnes & Noble, operating activities include the buying and selling of books (and other inventory items) as well as the multitude of other tasks required by that company’s retail function. As shown in Figure 17.1 "Typical Operating Activity Cash Inflows and Outflows", operating activities are those that are expected to take place regularly in the normal course of business.

Figure 17.1 Typical Operating Activity Cash Inflows and Outflows

The net number for the period (the inflows compared to the outflows) is presented as the cash flows generated from operating activities. This figure is viewed by many decision makers as a good measure of a company’s ability to prosper. Investors obviously prefer to see a positive number, one that increases from year to year. Some analysts believe that this figure is a better reflection of a company’s financial health than reported net income because the ultimate goal of a business is to generate cash.

For example, International Paper Company reported a net loss on its income statement for the year ended December 31, 2008, of $1.282 billion (considerably worse than any of the previous five years). However, its statement of cash flows for the same period reported a net cash inflow from operating activities of $2.669 million (considerably better than any of the previous five years). That is nearly a $4 billion difference. No one could blame a decision maker for being puzzled. Did the company do poorly that year or wonderfully well?

That is the problem with relying on only a few of the numbers in a set of financial statements without a closer and more complete inspection. What caused this company to lose over $1.2 billion dollars? How did the company manage to generate nearly $2.7 billion in cash from its operating activities? In-depth analysis of financial statements is never quick and easy. It requires patience and knowledge and the willingness to dig through all the available information.

Investing Activity Cash Flows

Question: On the statement of cash flows for the year ended August 31, 2011, Walgreen Co. reported that a net of over $1.5 billion in cash was spent in connection with a variety of investing activities. This company’s management obviously made decisions that required the use of considerable sums of money. Details about those expenditures should be of interest to virtually any party analyzing this company. What cash transactions are specifically identified as investing activities?

Answer: Investing activitiesA statement of cash flow category used to disclose cash receipts and disbursements arising from an asset transaction other than one relating to the primary activities of the reporting organization. encompass the acquisition and disposition of assets in transactions that are separate from the central activity of the reporting organization. In simple terms, these cash exchanges do not occur as part of daily operations.

- For a delicatessen, the purchase of bread, mustard, or onions is an operating activity, but the acquisition of a refrigerator or stove is an investing activity.

- For a pharmacy, the sale of aspirin or a decongestant is an operating activity, but the disposal of a delivery vehicle or cash register is an investing activity.

All of these cash transactions involve assets but, to be classified as an investing activity, they can only be tangentially related to the day-to-day operation of the business. For example, Figure 17.2 "The Three Biggest Investing Activity Cash Flows Identified on Walgreen’s Statement of Cash Flows for the Year Ended August 31, 2011" shows the three biggest investing activity cash flows reported by Walgreen.

Figure 17.2 The Three Biggest Investing Activity Cash Flows Identified on Walgreen’s Statement of Cash Flows for the Year Ended August 31, 2011

Healthy, growing companies normally expect cash flows from investing activities to be negative (a net outflow) as money is invested by management especially in new noncurrent assets. As can be seen in Figure 17.2 "The Three Biggest Investing Activity Cash Flows Identified on Walgreen’s Statement of Cash Flows for the Year Ended August 31, 2011", Walgreen Co. spent over $1.2 billion in cash during this one year to buy property and equipment. The company apparently had sufficient cash available to fund this significant expansion.

Financing Activity Cash Flows

Question: The third category of cash flows lists the amounts received and disbursed by a business through financing activities. For the year ended July 2, 2011, Sara Lee Corporation reported that its cash balance had been reduced by over $1.7 billion as a result of such financing activities. Again, that is a lot of money leaving the company. What transactions are specifically identified in a statement of cash flows as financing activities?

Answer: Financing activitiesA statement of cash flow category used to disclose cash receipts and disbursements arising from a liability or stockholders’ equity transaction other than one relating to the primary activities of the organization. are transactions separate from the central, day-to-day activities of an organization that involve either liabilities or shareholders’ equity accounts. Cash inflows from financing activities include issuing capital stock and incurring liabilities such as bonds or notes payable. Outflows are created by the distribution of dividends, the acquisition of treasury stock, the payment of noncurrent liabilities, and other similar cash transactions.

As can be seen in Figure 17.3 "The Three Biggest Financing Activity Cash Flows Identified on Sara Lee’s Statement of Cash Flows for the Year Ended July 2, 2011", Sara Lee’s three biggest changes in cash that resulted from financing activities were the repayments of other debt, purchases of common stock, and borrowing of other debt. Significant information about management’s decisions is readily apparent from an analysis of the cash flows from both investing and financing activities.

Figure 17.3 The Three Biggest Financing Activity Cash Flows Identified on Sara Lee’s Statement of Cash Flows for the Year Ended July 2, 2011

The net result reported for financing activities is frequently positive in some years and negative in others. When a company borrows money or sells capital stock, an overall positive inflow of cash is likely. In years when a large dividend is distributed or debt is settled, the net figure for financing activities is more likely to be negative.

Test Yourself

Question:

The Reardon Company paid salary to its employees totaling $527,000 during the current year. Into which category on a statement of cash flows will these payments be placed?

- Operating activities

- Investing activities

- Financing activities

- Capital activities

Answer:

The correct answer is choice a: Operating activities.

Explanation:

The payment of salary is a regular operating activity. The expenditure takes place as a direct result of the day-to-day operations of the business.

Test Yourself

Question:

The McGuire Company, located in Wilcox, Texas, issued 10,000 shares of its $3 par value common stock during this year for $9 in cash per share. Into which category on a statement of cash flows will this $90,000 capital contribution be placed?

- Operating activities

- Investing activities

- Financing activities

- Capital activities

Answer:

The correct answer is choice c: Financing activities.

Explanation:

This issuance of common (and preferred) stock is identified as a financing activity. It represents a change in a shareholders’ equity account. However, the cash inflow is not directly related to the daily operations of the business.

Test Yourself

Question:

The Staunton Corporation owns and operates several restaurants in eastern Iowa. Looking to expand operations, Staunton bought a piece of land recently for $500,000. The business paid $100,000 and a noncurrent note payable was signed for the remaining $400,000. How is this transaction reported on a statement of cash flows?

- Investing activity as an outflow of $100,000

- Investing activity as an outflow of $500,000

- Financing activity as an outflow of $100,000

- Financing activity as an outflow of $500,000

Answer:

The correct answer is choice a: Investing activity as an outflow of $100,000.

Explanation:

The purpose of the transaction is to acquire land. Land is an asset and this event did not take place as a normal part of Staunton’s daily operations. Thus, the transaction is an investing activity. Because $100,000 in cash was spent for this acquisition, the transaction is reported as an outflow of that amount. The $500,000 cost of the land and the $400,000 note payable will be recorded on the corporation’s balance sheet.

Disclosure of Noncash Transactions

Question: Significant investing and financing transactions can occur without any cash component. Land, for example, might be obtained by issuing common stock. Buildings are often bought through the signing of a long-term note payable with all cash payments deferred into the future. Is that information omitted entirely from the statement of cash flows? If no cash is received or expended, should a transaction be reported on a statement of cash flows?

Answer: All investing and financing transactions need to be reported in some manner because of the informational value. They represent choices made by the organization’s management. Even if no cash is involved, such events must still be disclosed in a separate schedule (often attached to the statement of cash flows) or explained in the notes to the financial statements. This information is valuable to the interested parties who want a complete picture of the investing and financing decisions that were made during the period.

For example, on the statement for Duke Energy Corporation for the year ended December 31, 2010, a significant noncash transaction was identified as “accrued capital expenditures” of $361 million. Although cash was not involved, inclusion of this information was still deemed to be important.

Stock dividends and stock splits, though, are omitted entirely in creating a statement of cash flows. As discussed previously, they are viewed as techniques to reduce the price of a corporation’s stock and are not decisions that impact the allocation of financial resources.

Key Takeaway

A statement of cash flows is required by U.S. GAAP whenever an income statement is presented. It explains all changes occurring in cash and cash equivalents during the reporting period. The various cash inflows and outflows are classified into one of three categories. Operating activities result from the primary or central function of the business. Investing activities are not part of normal operations and affect an asset (such as the cash acquisition of a truck or the sale of a patent). Financing activities are not part of normal operations and involve a liability or a stockholders’ equity account (borrowing money on a note, for example, or the reacquisition of treasury stock). Significant investing and financing activities that do not impact cash must still be disclosed because they reflect decisions made by management.

17.2 Cash Flows from Operating Activities: The Direct Method

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Identify the two methods available for reporting cash flows from operating activities.

- Indicate the method of reporting cash flows from operating activities that is preferred by FASB as well as the one that is most commonly used in practice.

- List the steps to be followed in determining cash flows from operating activities.

- List the income statement accounts that are removed entirely in computing cash flows from operating activities and explain this procedure when the direct method is applied.

- Identify common “connector accounts” that are used to convert accrual accounting figures to the change taking place in the cash balance as a result of these transactions.

- Compute the cash inflows and outflows resulting from common revenues and expenses such as sales, cost of goods sold, rent expense, salary expense, and the like.

The Handling of Noncash and Nonoperating Transactions by the Direct Method

Question: The net cash inflow or outflow generated by operating activities is especially significant information to any person looking at an organization’s financial health and future prospects. According to U.S. GAAP, that information can be presented within the statement of cash flows by either of two approaches: the direct methodA mechanical method of reporting the amount of cash flows that a company generates from its operating activities; it is preferred by FASB because the information is easier to understand but it is only rarely encountered in practice. or the indirect methodA mechanical method of reporting the amount of cash flows that a company generates from its operating activities; it is allowed by FASB (although the direct method is viewed as superior) but is used by a vast majority of businesses in the United States..

The numerical amount of the change in cash resulting from a company’s daily operations is not impacted by this reporting choice. The increase or decrease in cash is a fact that will not vary because of the manner of presentation. Both methods arrive at the same total. The informational value to decision makers, though, is potentially affected by the approach selected.

FASB has indicated a preference for the direct method. In contrast, reporting companies (by an extremely wide margin) continue to use the more traditional indirect method. Thus, both will be demonstrated here. The direct method is more logical and will be discussed first. How is information presented when the direct method is selected to disclose a company’s cash flows from operating activities?

Answer: The direct method starts with the entire income statement for the period. Then, each of the separately reported figures is converted into the amount of cash received or spent in carrying on this operating activity. “Sales,” for example, is turned into “cash collected from customers.” “Salary expense” and “rent expense” are recomputed as “cash paid to employees” and “cash paid to rent facilities.”

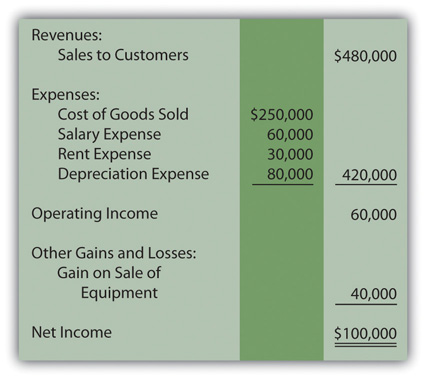

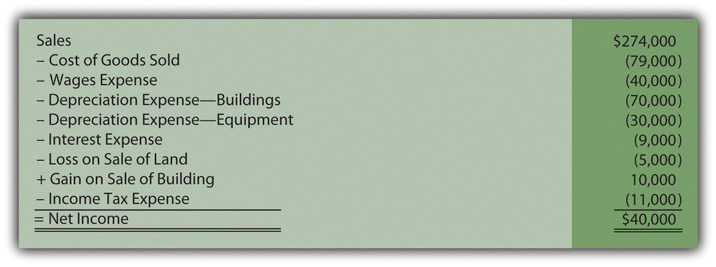

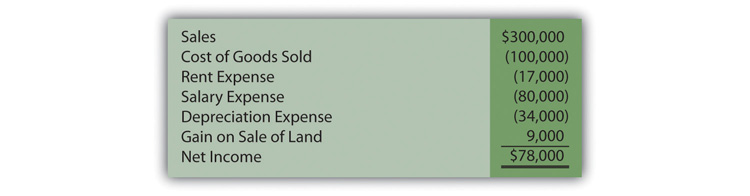

For illustration purposes, assume that Liberto Company prepared its income statement for the year ended December 31, Year One, as shown in Figure 17.4 "Liberto Company Income Statement Year Ended December 31, Year One". This statement has been kept rather simple so that the conversion to cash flows from operating activities is not unnecessarily complex. For example, income tax expense has been omitted.

Figure 17.4 Liberto Company Income Statement Year Ended December 31, Year One

The $100,000 net income figure reported here by Liberto is based on the application of U.S. GAAP. However, the amount of cash generated by the company’s operating activities might be considerably more or much less than that income figure. It is a different piece of information.

To transform a company’s income statement into its cash flows from operating activities, several distinct steps must be taken. These steps are basically the same regardless of whether the direct method or the indirect method is applied.

The first step is the complete elimination of any income statement account that does not involve cash. Although such balances are important in arriving at net income, they are not relevant to the cash generated and spent in connection with daily operations. By far the most obvious example is depreciation. This expense appears on virtually all income statements but has no direct impact on a company’s cash. In determining cash flows from operating activities, it is omitted because depreciation is neither a source nor use of cash. It is an allocation of a historical cost to expense over an asset’s useful life. To begin the calculation of the cash flows resulting from Liberto’s operating activities, the $80,000 depreciation expense must be removed.

The second step is the removal of any gains and losses that resulted from investing or financing activities. Although cash was likely involved in these transactions, this inflow or outflow is reported elsewhere in the statement of cash flows and not within the company’s operating activities. For example, Liberto’s $40,000 gain on the sale of equipment is germane to the reporting of investing activities, not operating activities. The cash received in this disposal is included on the statement of cash flows but as an investing activity.

Neither (a) noncash items such as depreciation nor (b) nonoperating gains and losses are included when an income statement is converted to the cash flows from operating activities.

Converting Accrual Accounts to Cash Flows—The Direct Method

Question: After all noncash and nonoperating balances are deleted, Liberto is left with four income statement accounts:

- Sales to customers—$480,000

- Cost of goods sold—$250,000

- Salary expense—$60,000

- Rent expense—$30,000

These balances all relate to operating activities. However, the numbers reflect the application of U.S. GAAP and accrual accounting rather than the amount of cash exchanged. The cash effects must be determined individually for these accounts. How are income statement figures such as sales or rent expense converted to the amount of cash received or expended?

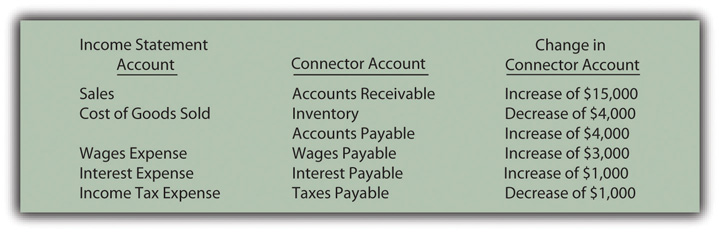

Answer: The third step in the process of determining cash flows from operating activities is the individual conversion to cash of all remaining income statement accounts. For these balances, a difference usually exists between the time of recognition as specified by accrual accounting and the exchange of cash. A sale is made on Monday (revenue is recognized), but the money is not collected until Friday. An employee performs work on Monday (expense is recognized) but payment is not made until Friday.

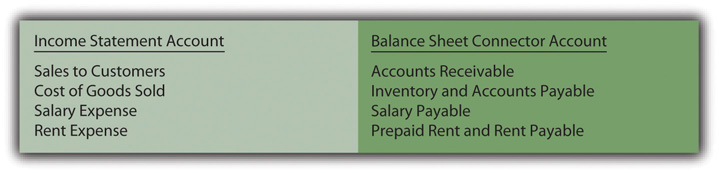

These timing differences occur because accrual accounting is required by U.S. GAAP. Thus, many revenues and expenses are not recorded at the same time as the related cash transactions. In the interim, recognition of an asset or liability balance is necessary. Between the sale on Monday and the collection on Friday, the business reports an account receivable. This asset goes up when the sale is made and down when the cash is collected. Between the employee’s work on Monday and the payment on Friday, the business reports a salary payable. This liability goes up when the money is earned and down when the cash payment is made. In this textbook, these interim accounts (such as accounts receivable and salary payable) will be referred to as “connector accounts” because they connect the recording mandated by accrual accounting with the cash transaction.

Each income statement account (other than the noncash and nonoperating numbers that have already been eliminated) has at least one asset or liability that is recorded between the time of accounting recognition and the exchange of cash. The changes in these connector accounts can be used to convert the individual income statement figures to their cash equivalents. Basically, the increase or decrease is removed to revert the reported number back to the amount of cash involved. As can be seen in Figure 17.5 "Common Connector Accounts for Liberto’s Four Income Statement Balances", connector accounts are mostly receivables, payables, and prepaid expenses.

Figure 17.5 Common Connector Accounts for Liberto’s Four Income Statement BalancesFor convenience, the allowance for doubtful accounts will not be included with accounts receivable. The possibility of bad debts makes the conversion to cash more complicated and is covered in upper-level accounting textbooks.

If a connector account is an asset and the balance goes up, the business has less cash (the receivable was not collected, for example). If a connector account is an asset and goes down, the business has more cash (such as when receivables from previous years are collected in the current period). Therefore, for a connector account that is an asset, an inverse relationship exists between the change in the balance during the year and the reporting entity’s cash balance.

- Increase in connector account that is an asset → Lower cash balance

- Decrease in connector account that is an asset → Higher cash balance

If a connector account is a liability and the balance goes up, the business has saved its cash and holds more (an expense has been incurred but not yet paid, for example). If a connector account is a liability and this balance falls, the business must have used its cash to reduce the debt and has less remaining. Consequently, a direct relationship exists between the change in a connector account that is a liability and the cash balance.

- Increase in connector account that is a liability → Higher cash balance

- Decrease in connector account that is a liability → Lower cash balance

Applying the Direct Method to Determine Cash Revenues and Expenses

Question: Liberto has one revenue and three expenses left on its income statement after removal of noncash and nonoperating items. To arrive at the net cash flows from operating activities, the cash inflow or outflow relating to each must be determined. Assume that the following changes took place during this year in the related balance sheet connector accounts:

- Accounts receivable: up $19,000

- Inventory: down $12,000

- Prepaid rent: up $4,000

- Accounts payable: up $9,000

- Salary payable: down $5,000

In applying the direct method to determine operating activity cash flows, how are the individual figures to be disclosed computed?

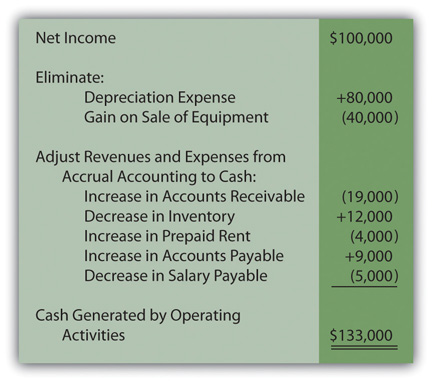

Answer:

- Sales to customers were reported on the income statement as $480,000. During that same period, accounts receivable increased by $19,000. Thus, less money was collected than the amount of the company’s credit sales. That is the cause for a rise in receivables. To reflect the collection of less cash, a reduction is needed. Consequently, the cash received from customers was only $461,000 ($480,000 less $19,000).

- Salary expense was reported as $60,000. During that time period, salary payable went down by $5,000. More cash must have been paid to cause this drop in the liability. The amount actually paid to employees was $65,000 ($60,000 plus $5,000).

- Rent expense was reported as $30,000. Prepaid rent increased by $4,000 from the first of the year to the end. This connector account is an asset. Because this asset increased, Liberto must have paid an extra amount for rent. Cash paid for rent was $34,000 ($30,000 plus $4,000).

-

Cost of goods sold has been left to last because it requires an extra step. The company first determines the quantity of inventory bought during this period. Only then can the cash payment made for those acquisitions be determined.

- Cost of goods sold is reported as $250,000. However, the balance held in inventory fell by $12,000. Thus, the company bought $12,000 less inventory than it sold. Fewer purchases cause a drop in inventory. The amount of inventory acquired during the period was only $238,000 ($250,000 less $12,000).

- Next, the cash paid for those purchases is calculated. As indicated, accounts payable went up $9,000. Liabilities increase because less money is paid. Although $238,000 of merchandise was acquired, only $229,000 in cash payments were made ($238,000 less $9,000).

After each of these four income statement accounts is converted to the amount of cash received or paid this period, the operating activity section of the statement of cash flows can be created by the direct method as shown in Figure 17.6 "Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Direct Method".

Figure 17.6 Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Direct Method

Liberto’s income statement reported net income of $100,000. However, the cash generated by operating activities during this same period was $133,000. The conversion from accrual accounting to operating cash inflows and outflows required three steps.

- All noncash revenues and expenses (depreciation, in this example) were removed. These accounts do not represent cash transactions.

- All nonoperating gains and losses (the gain on sale of equipment, in this example) were removed. These accounts reflect investing and financing activities and the resulting cash flows are reported in those sections of the statement of cash flows rather than within the operating activities.

- All remaining income statement accounts are adjusted to the amount of cash physically exchanged this period by applying the change in each related connector account. By this process, accrual accounting figures are converted to cash balances.

Test Yourself

Question:

The Giotto Company reported sales in its latest year of $800,000. Giotto held $170,000 in accounts receivable at the beginning of the period but only $144,000 at the end. Assume that all of these receivables are viewed as collectible so that no allowance is needed. What amount of cash did the company collect this period from its customers?

- $774,000

- $776,000

- $824,000

- $826,000

Answer:

The correct answer is choice d: $826,000.

Explanation:

During this year, the accounts receivable balance dropped by $26,000 ($170,000 to $144,000). Thus, more cash was collected than the amount of sales. Receivables decrease because cash is received. These additional receipts indicate that a total of $826,000 was collected from the Giotto’s customers ($800,000 plus $26,000).

Test Yourself

Question:

The Lessain Company reported salary expense of $345,000 on its income statement for the year ended December 31, Year One. At the beginning of that year, salary payable was shown as $31,000 but rose to $40,000 by December 31. In reporting the Lessain’s cash flows generated from operating activities, what amount should be shown as the cash paid to employees?

- $336,000

- $345,000

- $354,000

- $376,000

Answer:

The correct answer is choice a: $336,000.

Explanation:

Lessain’s salary payable went up by $9,000. Accrued liabilities rise because fewer payments are made than the expenses incurred. Although employees earned $345,000 during this year, only $336,000 was paid to them as salary ($345,000 less $9,000). It is this reduction in the cash payment that caused the salary payable account to increase by $9,000 during Year One.

Test Yourself

Question:

The TJ Corporation reported cost of goods sold for Year One of $564,000. During that same period, this company’s inventory balance rose by $22,000 while its accounts payable fell by $7,000. In creating a statement of cash flows using the direct method, what amount should be reported by the TJ Corporation as the cash spent to acquire inventory?

- $535,000

- $549,000

- $579,000

- $593,000

Answer:

The correct answer is choice d: $593,000.

Explanation:

Although cost of goods sold was reported as $564,000, the inventory on hand increased $22,000. More inventory was bought that year than sold. TJ acquired $586,000 in inventory during Year One ($564,000 sold plus the $22,000 increase). At the same time, accounts payable dropped. This decrease indicates that more in cash was paid than the amount bought. Spending an extra $7,000 caused the reduction. Thus, cash paid out this year to acquire inventory was $593,000 ($586,000 plus $7,000).

Test Yourself

Question:

Sales reported by a local shoe store are $470,000. Accounts receivable decreased by $27,000 this year while unearned revenues rose by $14,000. If the direct method is used to report cash flows from operating activities, how much should be shown as the store’s cash collected from its customers?

- $429,000

- $467,000

- $483,000

- $511,000

Answer:

The correct answer is choice d: $511,000.

Explanation:

A new connector account (unearned revenues) is included here. This balance represents cash received where revenue has not yet been earned. This increase indicates that $14,000 more in cash was collected from customers than the amount reported as revenue. Also, accounts receivable fell by $27,000. Receivables are reduced through collection. The shoe store must have received that much more cash than it earned. Cash received during this period is $511,000 ($470,000 plus $14,000 and $27,000).

Key Takeaway

An entity’s cash flows from operating activities can be derived and reported by either the direct method or the indirect method. FASB has expressed preference for the direct method but the indirect method has been adopted by virtually all businesses in the United States. The process always begins with the income for the period (the entire income statement is used when the direct method is applied). First noncash items (such as depreciation) and then nonoperating gains and losses are eliminated entirely because they are not related to operating activity cash flows. In the direct method, the remaining revenue and expense accounts are individually converted into cash figures. For each, the change in one or more related balance sheet connector accounts is used to adjust these accrual accounting numbers to their corresponding cash balances. Thus, income statement balances are returned to their underlying cash inflows and outflows for reporting purposes.

17.3 Cash Flows from Operating Activities: The Indirect Method

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Explain the difference in the start of the operating activities section of the statement of cash flows when the indirect method is used rather than the direct method.

- Demonstrate the removal of both noncash items and nonoperating gains and losses in the application of the indirect method.

- Determine the effect caused by the change in the various connector accounts when the indirect method is used to present cash flows from operating activities.

- Identify the reporting classification for interest revenues, dividend revenues, and interest expense in creating a statement of cash flows and explain the controversy that resulted from this handling.

The Steps Followed in Applying the Indirect Method

Question: As mentioned, most organizations do not choose to present their operating activity cash flows using the direct method despite the preference of FASB. Instead, this information is almost universally shown within a statement of cash flows by means of the indirect method. How does the indirect method of reporting operating activity cash flows differ from the direct method?

Answer: The indirect method actually follows the same set of procedures as the direct method except that it begins with net income rather than the business’s entire income statement. After that, the same three steps demonstrated previously to determine the net cash flows from operating activities are followed although the mechanical application here is different.

- Noncash items are removed.

- Nonoperational gains and losses are removed.

- Adjustments are made, based on the monetary change occurring during the period in the various balance sheet connector accounts, to switch all remaining revenues and expenses from accrual accounting to cash accounting.

Removing Noncash and Nonoperating Items—The Indirect Method

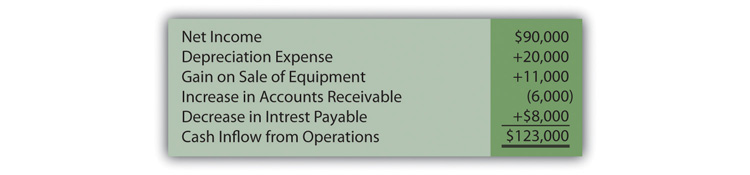

Question: In the income statement presented in Figure 17.4 "Liberto Company Income Statement Year Ended December 31, Year One" for the Liberto Company, net income was reported as $100,000. This figure included depreciation expense (a noncash item) of $80,000 and a gain on the sale of equipment (an investing activity rather than an operating activity) of $40,000. In applying the indirect method, how are noncash items and nonoperating gains and losses removed from net income?

Answer: First, all noncash items within net income are eliminated. Depreciation is the example included here. As an expense, it is a negative component found within net income. To remove a negative, it is offset by a positive. Thus, adding back $80,000 serves to remove the impact of depreciation from the reporting company’s net income.

Second, all nonoperating items within net income are eliminated. Liberto’s gain on sale of equipment is reported within reported income. As a gain, it is a positive figure; it helped increase profits this period. To eliminate this gain, $40,000 must be subtracted from net income. The cash flows resulting from this transaction came from an investing activity and not an operating activity.

In applying the indirect method, as shown in Figure 17.7 "Operating Activity Cash Flows, Indirect Method—Elimination of Noncash and Nonoperating Balances", a negative is removed by addition; a positive is removed by subtraction.

Figure 17.7 Operating Activity Cash Flows, Indirect Method—Elimination of Noncash and Nonoperating Balances

- In the direct method, these two income statement amounts were simply omitted in arriving at the individual cash flows from operating activities.

- In the indirect method, they are both physically removed from income by reversing their effect.

The impact is the same in the indirect method as in the direct method; the balances are removed.

Converting Accrual Accounting Figures to Cash Balances—The Indirect Method

Question: After all noncash and nonoperating items are removed from net income, only the changes in the balance sheet connector accounts must be utilized to complete the conversion to cash. For Liberto, those balances were shown previously.

- Accounts receivable: up $19,000

- Inventory: down $12,000

- Prepaid rent: up $4,000

- Accounts payable: up $9,000

- Salary payable: down $5,000

Each of these increases and decreases was used in the direct method to turn accrual accounting figures into cash balances. That same process is followed in the indirect method. In determining cash flows from operating activities, how are changes in an entity’s connector accounts reflected in the application of the indirect method?

Answer: Although the procedures appear to be different, the same logic is applied in the indirect method as in the direct method. The change in each of the previous connector accounts discloses the difference in the accrual accounting amounts recognized in the income statement and the actual changes in cash. Here, though, the effect is measured on net income as a whole rather than on the individual revenue and expense accounts.

Accounts receivable increased by $19,000. This rise in the receivable balance shows that less money was collected than the sales made by Liberto during the period. Receivables go up because customers are slow to pay. This change results in a lower cash balance. Thus, the $19,000 is subtracted in arriving at the cash flow amount generated by operating activities. The cash received was actually less than the figure reported for sales that appears within the company’s net income. Subtract $19,000.

Inventory decreased by $12,000. A drop in the amount of inventory on hand indicates that less merchandise was purchased during the period. Buying less requires a smaller amount of cash to be paid. That leaves the cash balance higher. The $12,000 is added in arriving at the operating activity change in cash. Add $12,000.

Prepaid rent increased by $4,000. An increase in any prepaid expense shows that more of the asset was acquired during the year than was consumed. This additional purchase requires the use of cash; thus, the resulting cash balance is lower. The increase in prepaid rent necessitates a $4,000 subtraction in the operating activity cash flow computation. Subtract $4,000.

Accounts payable increased by $9,000. Any jump in a liability means that Liberto paid less cash during the period than the debts that were incurred. Postponing liability payments is a common method for saving cash to keep the reported balance high. In determining cash flows from operating activities, the $9,000 liability increase is added. Add $9,000.

Salary payable decreased by $5,000. Liability balances fall when additional payments are made. Such cash transactions are reflected in applying the indirect method by a $5,000 subtraction from net income. Subtract $5,000.

Therefore, if Liberto Company uses the indirect method to report its cash flows from operating activities, the information will be presented to decision makers as shown in Figure 17.8 "Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Indirect Method".

Figure 17.8 Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Indirect Method

As with the direct method (Figure 17.6 "Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Direct Method"), the total here reflects a net cash inflow of $133,000 from the operating activities of this company. In both cases, the starting spot was net income (either as the entire income statement or as the single number). Then, all noncash items were removed as well as nonoperating gains and losses. Finally, the effect of changes in the various connector accounts that bridge the time period between accrual accounting recognition and the cash exchange are included so that only the cash flows from operating activities remain.

In reporting operating activity cash flows by means of the indirect method (Figure 17.8 "Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Indirect Method"), the following pattern can be seen.

- A change in a connector account that is an asset is reflected on the statement in the opposite fashion. As shown previously, increases in both accounts receivable and prepaid rent are subtracted while a decrease in inventory is added.

- A change in a connector account that is a liability is included on the statement in an identical change. An increase in accounts payable is added whereas a decrease in salary payable is subtracted.

A quick visual comparison of the direct method (Figure 17.6 "Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Direct Method") and the indirect method (Figure 17.8 "Liberto Company Statement of Cash Flows for Year One, Operating Activities Reported by Indirect Method") makes the two appear almost completely unrelated. However, when analyzed more closely, the same series of steps can be seen in each. They both begin with the income for the period. Noncash items and nonoperating gains and losses are removed. Changes in the connector accounts for the period are factored in so that only the cash from operating activities remains.

Test Yourself

Question:

The Hemingway Company reported net income last year of $354,000. Within that figure, depreciation expense of $37,000 was included. In addition, accounts receivable increased by $11,000 during the period. What amount of cash did this company generate from its operating activities?

- $306,000

- $328,000

- $380,000

- $402,000

Answer:

The correct answer is choice c: $380,000.

Explanation:

Depreciation is a noncash expense that appears within net income as a negative. To remove it, the $37,000 figure is added. Addition counterbalances the original negative effect. The increase in accounts receivable means that customers were slow to pay this year. Credit sales were greater than the amount of cash received. The $11,000 is subtracted from net income to arrive at the lower cash figure. Thus, cash inflow from operating activities is $380,000 ($354,000 + $37,000 − $11,000).

Test Yourself

Question:

The Faulkner Corporation reported net income in Year One of $437,000. Accounts receivable at the start of the period totaled $26,000 but grew to $41,000 by the end of Year One. Beginning insurance payable was $7,000 but fell to an ending balance of $4,000. What amount of cash did Faulkner collect as a result of its operating activities?

- $419,000

- $425,000

- $449,000

- $455,000

Answer:

The correct answer is choice a: $419,000.

Explanation:

Accounts receivable went from $26,000 to $41,000. The $15,000 increase indicates that credit sales were greater than cash collected. The $15,000 is subtracted from net income. Insurance payable fell by $3,000 ($7,000 to $4,000); thus, the amount paid was greater than the expense recognized. Cash was spent to reduce the liability. The $3,000 is also subtracted in arriving at the cash change. The cash inflow from operating activities is $419,000 ($437,000 net income − $15,000 and $3,000).

The Reporting of Dividends and Interest on the Statement of Cash Flows

Question: When listing cash flows from operating activities for the year ended December 31, 2010, EMC Corporation (a technology company) included an inflow of nearly $103 million labeled as “dividends and interest received” as well as an outflow of over $76 million shown as “interest paid.”

Unless a company is a bank or financing institution, dividend and interest revenues do not appear to relate to its central operating function. For most businesses, these cash inflows are fundamentally different from the normal sale of goods and services. Monetary amounts collected as dividends and interest resemble investing activity cash inflows because they are often generated from noncurrent assets. Similarly, interest expense payments are normally associated with noncurrent liabilities rather than resulting from daily operations. Interest expenditures could certainly be viewed as a financing activity cash outflow.

Dividend distributions are not in question here. They are labeled as financing activity cash outflows because they are made directly to stockholders. The issue is the classification of dividend and interest revenue collections and interest expense payments. Why is cash received as dividends and interest and cash paid as interest expense reported within operating activities on a statement of cash flows rather than as investing activities and financing activities?

Answer: Authoritative pronouncements that create U.S. GAAP are the subject of years of intense study, discussion, and debate. In this process, controversies often arise. When FASB issued its official standard on cash flows in 1987, three of the seven board members voted against passage. Their opposition, at least in part, came from the handling of interest and dividends. On page ten of Statement 95, Statement of Cash Flows, these three argue “that interest and dividends received are returns on investments in debt and equity securities that should be classified as cash inflows from investing activities. They believe that interest paid is a cost of obtaining financial resources that should be classified as a cash outflow for financing activities.”

The other board members were not convinced. Thus, inclusion of dividends collected, interest collected, and interest paid within an entity’s operating activity cash flows became a requirement of U.S. GAAP. Such disagreements arise frequently in the creation of official accounting rules.

The majority of the board apparently felt that—because these transactions occur on a regular ongoing basis—a better portrait of the organization’s cash flows is provided by inclusion within operating activities. At every juncture of financial accounting, multiple possibilities for reporting exist. Rarely is complete consensus ever achieved as to the most appropriate method of presenting financial information.

Talking With an Independent Auditor about International Financial Reporting Standards

Following is the conclusion of our interview with Robert A. Vallejo, partner with the accounting firm PricewaterhouseCoopers.

Question: Any company that follows U.S. GAAP and issues an income statement must also present a statement of cash flows. Cash flows are classified as resulting from operating activities, investing activities, or financing activities. Are IFRS rules the same for the statement of cash flows as those found in U.S. GAAP?

Rob Vallejo: Differences do exist between the two frameworks for the presentation of the statement of cash flows, but they are relatively minor. Probably the most obvious issue involves the reporting of interest and dividends that are received and paid. Under IFRS, interest and dividend collections may be classified as either operating or investing cash flows whereas, in U.S. GAAP, they are both required to be shown within operating activities. A similar difference exists for interest and dividend payments. These cash outflows can be classified as either operating or financing activities according to IFRS. For U.S. GAAP, interest payments are viewed as operating activities whereas dividend payments are considered financing activities.

Key Takeaway

Most reporting entities use the indirect method to report net cash flows from operating activities. This presentation begins with net income and then eliminates any noncash items (such as depreciation expense) as well as nonoperating gains and losses. Their impact on net income is reversed to create this removal. In addition, changes in each balance sheet connector account (such as accounts receivables, inventory, accounts payable, and salary payable) must also be utilized in converting from accrual accounting to cash. Changes in asset connectors are reversed in arriving at cash flows from operating activities whereas changes in liability connectors have the same impact (increases are added and decreases are subtracted). Cash transactions that result from interest revenue, dividend revenue, and interest expense are all reported within operating activities because they happen on a regular ongoing basis. However, some argue that interest and dividend collections are really derived from investing activities and interest payments relate to financing activities.

17.4 Cash Flows from Investing and Financing Activities

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Analyze the changes in assets that are not operating assets to determine cash inflows and outflows from investing activities.

- Analyze the changes in liabilities (that are not operating liabilities) and stockholders’ equity accounts to determine cash inflows and outflows from financing activities.

- Recreate journal entries to determine the individual effects on ledger accounts where several cash transactions have occurred.

Determining Cash Flows from Investing Activities

Question: As shown in Figure 17.9 "The Walt Disney Company Investing Activity Cash Flows for Year Ended October 2, 2010", The Walt Disney Company reported a net cash outflow of over $4.5 billion as a result of investing activities undertaken during the year ended October 2, 2010.

Figure 17.9 The Walt Disney Company Investing Activity Cash Flows for Year Ended October 2, 2010

This section of Disney’s statement of cash flows shows that a number of transactions involving assets (other than operating assets such as inventory and accounts receivable) created this $4.5 billion reduction in cash. Information about management decisions is readily available. For example, a potential investor can see that officials chose to spend over $2.1 billion in cash during this year in connection with Disney’s parks, resorts and other property. Interestingly, this expenditure level is approximately 20 percent higher than the monetary amount invested in those assets the previous year. With a strong knowledge of financial accounting, a portrait of a business and its activities begins to become clear.

After the various cash amounts are determined, conveyance of this information does not appear particularly complicated. How does a company arrive at the investing activity figures that are disclosed within the statement of cash flows?

Answer: Here, the accountant is not interested in assets such as inventory, accounts receivable, and prepaid rent because they are included within operating activities. Instead, each of the other asset accounts (land, buildings, equipment, patents, trademarks, and the like) is investigated to determine the individual transactions that took place during the year. The amount of every cash change is identified and reported. A sale of land can create a cash inflow whereas the acquisition of a building may well require the payment of some amount of cash.

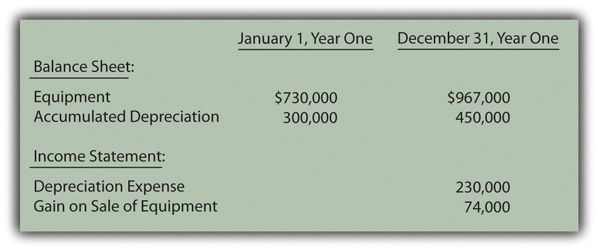

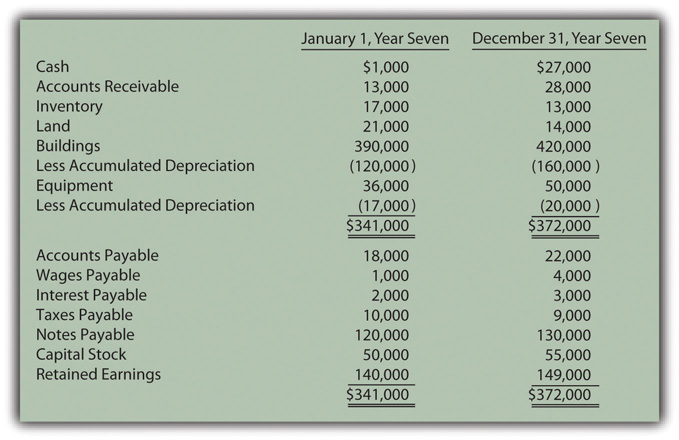

The difficulty in this process frequently comes from having to sort through multiple purchases and sales to compute the exact amount of cash involved in each transaction. At times, determining the individual cash effects can resemble the work needed to solve a puzzle with many connecting pieces. Often, the journal entries that were made originally must be replicated. Even then, the cash portion of these transactions may have to be determined by mathematical logic. To illustrate, assume that the Hastings Company reports the account balances that appear in Figure 17.10 "Account Balances to Illustrate Cash Flows from Investing Activities".

Figure 17.10 Account Balances to Illustrate Cash Flows from Investing Activities

In looking through the financial records maintained by this business, assume the accountant finds two additional pieces of information about the accounts in Figure 17.10 "Account Balances to Illustrate Cash Flows from Investing Activities":

- Equipment costing $600,000 was sold this year for cash.

- Other equipment was acquired, also for cash.

Sale of equipment. This transaction is analyzed first because the cost of the equipment is already provided. However, the accumulated depreciation relating to the disposed asset is not known. The accountant must study the available data to determine that missing number because that balance is also removed when the asset is sold.

Accumulated depreciation at the start of the year was $300,000 but depreciation expense of $230,000 was then reported as shown in Figure 17.10 "Account Balances to Illustrate Cash Flows from Investing Activities". This expense was apparently recognized through the year-end adjustment recreated in Figure 17.11 "Assumed Adjusting Entry for Depreciation".

Figure 17.11 Assumed Adjusting Entry for Depreciation

The depreciation entry increases the accumulated depreciation account to $530,000 ($300,000 plus $230,000). However, the end-of-year balance is not $530,000 but only $450,000. What caused the $80,000 drop in this contra asset account?

Accumulated depreciation represents the cost of a long-lived asset that has already been expensed. Virtually the only situation in which accumulated depreciation is reduced is the disposal of the related asset. Here, the accountant knows equipment was sold. Although the amount of accumulated depreciation relating to that asset is unknown, the assumption can be made that the sale caused this reduction of $80,000. No other possible decrease in accumulated depreciation is mentioned.

Thus, the accountant believes equipment costing $600,000 but with accumulated depreciation of $80,000 (and, hence, a net book value of $520,000) was sold. The amount received must have created the $74,000 gain that is shown in the reported balances in Figure 17.10 "Account Balances to Illustrate Cash Flows from Investing Activities".

A hypothetical journal entry can be constructed in Figure 17.12 "Assumed Journal Entry for Sale of Equipment" from this information.

Figure 17.12 Assumed Journal Entry for Sale of Equipment

This journal entry only balances if the cash received is $594,000. Equipment with a book value of $520,000 was sold during the year at a reported gain of $74,000. Apparently, $594,000 was the cash received. How does all of this information affect the statement of cash flows?

- A cash inflow of $594,000 is reported within investing activities. It is labeled something like “cash received from sale of equipment.”

- Depreciation of $230,000 is eliminated from net income in computing the cash flows from operating activities because this expense had no impact on cash flows.

- In determining the cash flows from operating activities, the $74,000 gain is also eliminated from net income. The $594,000 cash collection comes from an investing activity rather than an operating activity.

Purchase of equipment. According to the information provided, another asset was acquired this year but its cost is not provided. Once again, the accountant must puzzle out the amount of cash involved in the transaction.

The equipment account began the year with a $730,000 balance. The sale of equipment costing $600,000 was just discussed. This transaction should have dropped the ledger account to $130,000 ($730,000 less $600,000). However, at the end of the period, the amount reported for this asset is actually $967,000. How did the cost of equipment rise from $130,000 to $967,000? If no other transaction is mentioned, the most reasonable explanation is that additional equipment was acquired at a cost of $837,000 ($967,000 less $130,000). Unless information is available indicating that part of this purchase was made on credit, the journal entry that was recorded originally must have been made as shown in Figure 17.13 "Assumed Journal Entry for Purchase of Equipment".

Figure 17.13 Assumed Journal Entry for Purchase of Equipment

At this point, the changes in all related accounts (equipment, accumulated depreciation, depreciation expense, and the gain on sale of equipment) have been used to determine the two transactions for the period and their related cash inflows and outflows. In the statement of cash flows for this company, the investing activities are listed as shown in Figure 17.14 "Statement of Cash Flows—Investing Activities".

Figure 17.14 Statement of Cash Flows—Investing Activities

Test Yourself

Question:

The following accounts appear on Red Company’s balance sheets at the beginning and end of Year One:

Figure 17.15

During Year One, equipment with an original cost of $30,000 and accumulated depreciation of $18,000 was sold at a loss of $3,000. What is the cash received on the sale of that equipment?

- $9,000

- $12,000

- $15,000

- $16,000

Answer:

The correct answer is choice a: $9,000.

Explanation:

The book value of this equipment is $12,000 ($30,000 cost less $18,000 accumulated depreciation). Because the equipment was sold at a loss of $3,000, cash received must have been only $9,000 ($12,000 less $3,000). The transaction can also be recreated through the following entry.

Figure 17.16

The loss is eliminated from income in determining the cash flows from operating activities. If the direct method is used, the loss is simply omitted. If the indirect method is used, the loss (because it is a negative within net income) is added back to net income. The $9,000 cash inflow appears in the investing activity section of the statement of cash flows.

Test Yourself

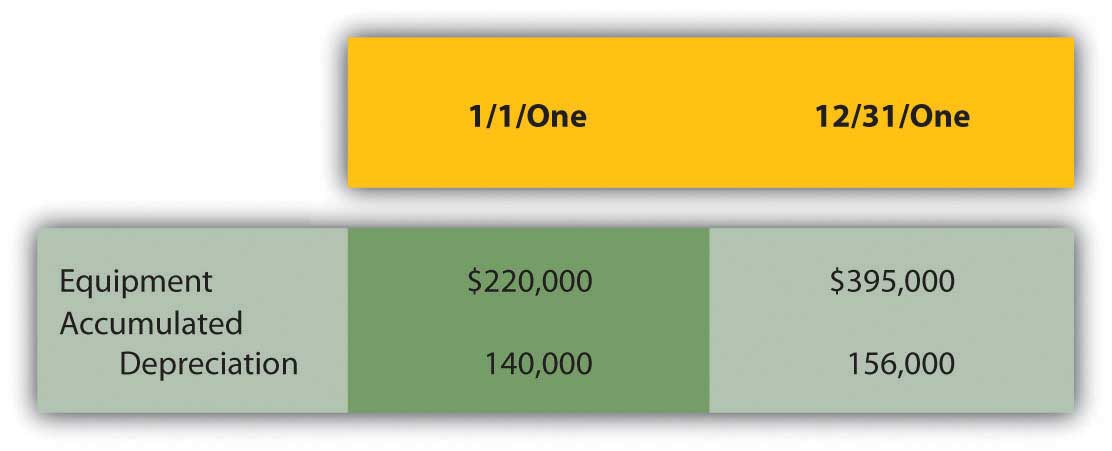

Question:

The following accounts appear on White Company’s balance sheets at the beginning and end of Year One.

Figure 17.17

One piece of equipment—with an original cost of $30,000 and accumulated depreciation of $18,000—was sold at a loss of $3,000. On a statement of cash flows, what amount should be reported as cash paid for additional equipment bought during the period?

- $145,000

- $175,000

- $205,000

- $235,000

Answer:

The correct answer is choice c: $205,000.

Explanation:

Based on the information provided, the equipment account decreased by the $30,000 cost of the asset that was sold. The reported balance would have fallen from $220,000 to $190,000. At year’s end, equipment was not reported as $190,000 but rather as $395,000. With no other transactions mentioned, the $205,000 increase from $190,000 to $395,000 must have been created by purchase of additional equipment. This $205,000 acquisition appears in the investing activities section as a cash outflow.

Test Yourself

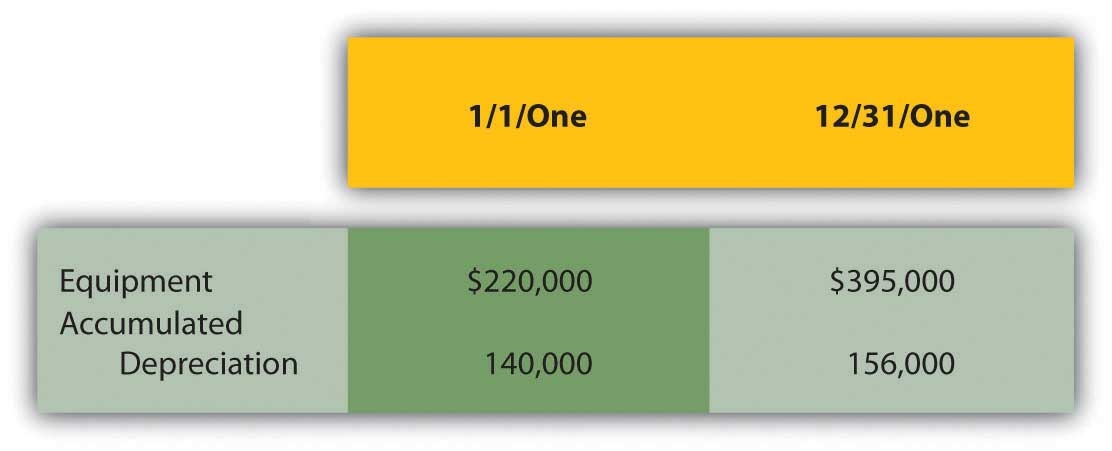

Question:

The following accounts appear on Blue Company’s balance sheets at the beginning and end of Year One.

Figure 17.18

Equipment with an original cost of $30,000 and accumulated depreciation of $18,000 was sold at a loss of $3,000. What is the depreciation expense recognized during the year and, if the indirect method is used, how is this reported in the statement of cash flows?

- $19,000 is subtracted from net income

- $28,000 is added to net income

- $34,000 is added to net income

- $46,000 is subtracted from net income

Answer:

The correct answer is choice c: $34,000 is added to net income.

Explanation:

Because of the sale of equipment, accumulated depreciation drops by $18,000 from $140,000 to $122,000. By the end of Year One, the account is $156,000. Accumulated depreciation only increases as a result of recording depreciation expense. The increase from $122,000 to $156,000 points to an expense of $34,000. Depreciation is a negative noncash item in net income and is removed in presenting cash flows from operating activities. With the indirect method is used, depreciation is added back.

Determining Cash Flows from Financing Activities

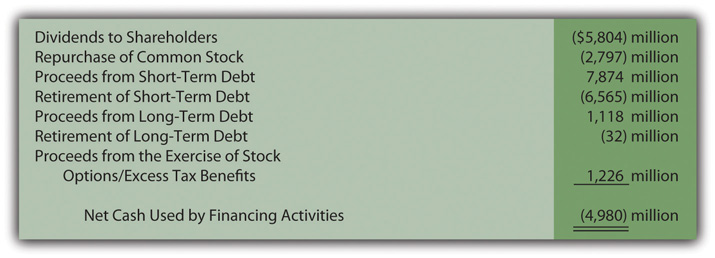

Question: For the year ended January 2, 2011, Johnson & Johnson reported a net cash outflow from financing activities of over $4.9 billion. Within the statement of cash flows, this total was broken down into seven specific categories as replicated in Figure 17.19 "Financing Activity Cash Flows Reported by Johnson & Johnson for Year Ended January 2, 2011".

Figure 17.19 Financing Activity Cash Flows Reported by Johnson & Johnson for Year Ended January 2, 2011

In preparing a statement of cash flows, how does a company such as Johnson & Johnson determine the amounts that were paid and received as a result of its various financing activities?

Answer: As has been indicated, financing activities reflect transactions that are not part of a company’s central operations and involve either a liability or a stockholders’ equity account. Johnson & Johnson paid over $5.8 billion in cash dividends in this year and nearly $2.8 billion to repurchase common stock (treasury shares). During the same period, approximately $7.9 billion in cash was received from borrowing money on short-term debt and another $1.1 billion from long-term debt. None of these amounts are directly associated with the company’s operating activities. However, they do involve either liabilities or stockholders’ equity accounts and are appropriately reported as financing activities.

The procedures used in determining the cash amounts to be reported as financing activities are the same as demonstrated above for investing activities. The change in each relevant balance sheet account is analyzed to determine cash payments and receipts. In starting this process, many liabilities such as accounts payable, rent payable, and salaries payable are ignored because they relate only to operating activities. However, the remaining liabilities and all stockholders’ equity accounts must be studied. The recording of individual transactions can be replicated so that the cash effect is isolated.

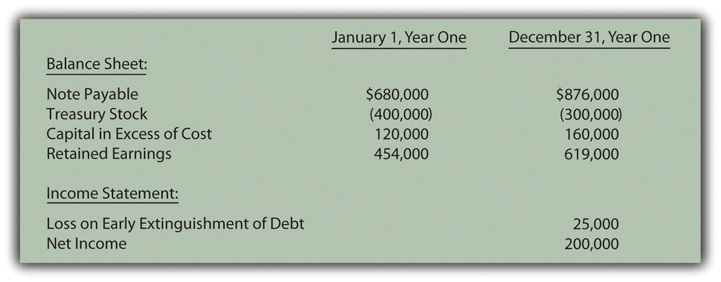

To illustrate, various account balances for the Hastings Corporation are presented in the schedule included in Figure 17.20 "Account Balances to Illustrate Cash Flows from Financing Activities".

Figure 17.20 Account Balances to Illustrate Cash Flows from Financing Activities

In examining the financial records for the Hastings Corporation for this year, the accountant finds several additional pieces of information:

- Cash of $400,000 was borrowed by signing a note payable with a local bank.

- Another note payable was paid off prior to its maturity date because of a drop in interest rates.

- Treasury stock was reissued to the public for cash.

- A cash dividend was declared and distributed.

Once again, the various changes in each account balance can be analyzed to determine the cash flows, this time to be reported as financing activities.

Borrowing on note payable. Complete information about this transaction is available. Hastings Corporation received $400,000 in cash from a bank by signing a note payable. Figure 17.21 "Assumed Journal Entry for Signing of Note Payable" provides the journal entry to record the incurrence of this liability.

Figure 17.21 Assumed Journal Entry for Signing of Note Payable

On a statement of cash flows, this transaction is listed within the financing activities as a $400,000 cash inflow.

Paying note payable. Incurring the $400,000 debt raises the note payable balance from $680,000 to $1,080,000. By the end of the year, this account only shows a total of $876,000. The company’s notes payable have decreased in some way by $204,000 ($1,080,000 less $876,000). According to the information gathered by the accountant, a debt was paid off this year prior to maturity. In addition, the general ledger reports a $25,000 loss on the early extinguishment of a debt. When a bond or note is settled before its maturity, a penalty payment is often required. Once again, the journal entry for this transaction can be recreated by logical reasoning as shown in Figure 17.22 "Assumed Journal Entry for Extinguishment of Debt".

Figure 17.22 Assumed Journal Entry for Extinguishment of Debt

To balance this entry, cash of $229,000 must have been paid. Spending this amount of money to extinguish a $204,000 liability creates the $25,000 reported loss. The cash outflow of $229,000 relates to a liability and is, thus, listed on the statement of cash flows as a financing activity.

Issuance of treasury stock. This equity balance reflects the cost of all repurchased shares. During the year, the total in the T-account fell by $100,000 from $400,000 to $300,000. Apparently, $100,000 was the cost of the company’s shares reissued to the public. At the same time, the capital in excess of cost balance rose from $120,000 to $160,000. That $40,000 increase in contributed capital must have been created by this issuance since no other stock transaction is mentioned. The shares were sold for more than their purchase price. The journal entry must have looked like the one presented in Figure 17.23 "Assumed Journal Entry for Sale of Treasury Stock".

Figure 17.23 Assumed Journal Entry for Sale of Treasury Stock

If the original cost of the treasury stock was $100,000 and $40,000 was added to the capital in excess of cost, the cash inflow from this transaction had to be $140,000. Cash received from the issuance of treasury stock is reported as a financing activity of $140,000 because it relates to a stockholders’ equity account.

Distribution of dividend. A dividend has been paid to the company’s stockholders, but the amount is not shown in the information provided. However, other information is available. Net income for the period was reported as $200,000. Those profits increase retained earnings. As a result, the beginning balance of $454,000 increases to $654,000. Instead, retained earnings only rose to $619,000 by the end of the year. The unexplained drop of $35,000 ($654,000 less $619,000) must have resulted from the payment of the dividend. No other possible reason is given for this reduction. The appropriate journal entry is found in Figure 17.24 "Assumed Journal Entry for Payment of Dividend". Hence, a cash dividend distribution of $35,000 is shown within the statement of cash flows as a financing activity.

Figure 17.24 Assumed Journal Entry for Payment of Dividend

In this example, four specific financing activity transactions have been identified as created changes in cash. This section of Hasting’s statement of cash flows can be created in Figure 17.25 "Statement of Cash Flows—Financing Activities". All the sources and uses of this company’s cash (as related to financing activities) are apparent from this schedule. Determining the cash amounts can take some computational logic, but the information is then clear and useful.

Figure 17.25 Statement of Cash Flows—Financing Activities

Test Yourself

Question:

The Abraham Company begins the year with bonds payable having a reported balance of $600,000. The ending balance is $700,000. This company’s income statement for the year reports a gain on extinguishment of bond of $9,000. During the year, new bonds were issued at their face value of $300,000. How much cash was paid for the bonds that were extinguished?

- $191,000

- $209,000

- $291,000

- $309,000

Answer:

The correct answer is choice a: $191,000.

Explanation:

The issuance of $300,000 in new debt would increase the liability balance from $600,000 to $900,000. However, the account ended the year at only $700,000. The unexplained reduction of $200,000 must have been the face value of the debt paid off ($900,000 less $700,000). Because a gain of $9,000 was recognized on this transaction, the company managed to eliminate the debt by paying only $191,000.

Test Yourself

Question:

The Oregon Company’s total stockholders’ equity on January 1 was $870,000. By the end of the year, stockholders’ equity had risen to $990,000. This company bought treasury stock this year. The shares had originally been issued for $120,000 but were reacquired for $150,000. In addition, Oregon reported net income for the year of $340,000. No other stock transactions occurred but a cash dividend was paid. How much should Oregon report on the statement of cash flows for the dividend distribution?

- $50,000

- $60,000

- $70,000

- $80,000

Answer:

The correct answer is choice c: $70,000.

Explanation:

Acquisition of the treasury stock reduces stockholders’ equity by $150,000 while net income increases it by $340,000. If nothing else took place, stockholders’ equity at the end of the period would be $1,060,000 ($870,000 less $150,000 but plus $340,000). Instead, the ending total is actually $990,000. Because only the dividend distribution is left to include, it must have been the amount needed to reduce stockholders’ equity to its final reported total ($70,000 or $1,060,000 less $990,000).

Key Takeaway

In determining cash flows from investing activities, current assets such as inventory, accounts receivable, and prepaid rent are ignored because they relate to operating activities. The accountant then analyzes all changes that have taken place in each remaining asset such as buildings and equipment. Hypothetical journal entries can be recreated to replicate the impact of each transaction and lead to the amount of cash involved. For financing activities, a similar process is applied. Liabilities such as accounts payable, interest payable, and salaries payable are not excluded; they only impact operating activities. Monetary changes in the remaining liabilities (notes and bonds payable, for example) and all stockholders’ equity accounts are analyzed. Again, the journal entries that were recorded to report individual events can be recreated so that the cash amounts are known. Once all changes in these accounts have been determined, the various sections of the statement of cash flows can be produced.

Talking with a Real Investing Pro (Continued)

Following is the conclusion of our interview with Kevin G. Burns.

Question: Many investors watch the movement of a company’s reported net income and earnings per share and make investment decisions based on increases or decreases. Other investors argue that the amount of cash flows generated by operating activities is really a more useful figure. When you make investing decisions are you more inclined to look at net income or the cash flows generated by operating activities?

Kevin Burns: As I have said previously, net income and earnings per share have a lot of subjectivity to them. Unfortunately, cash flow information can be badly misused also. A lot of investors seem fascinated by the calculation of EBITDA which is the company’s earnings before interest, taxes, depreciation, and amortization. I guess you could say that determining EBITDA is like blending net income and cash flows. But, to me, interest and taxes are real cash expenses so why exclude them? The biggest mistake I ever made as an investor or financial advisor was putting too much credence in EBITDA as a technique for valuing a business. Earnings are earnings and that is important information. A lot of analysts now believe that different cash flow models should be constructed for different industries. If you look around, you can find cable industry cash flow models, theater cash flow models, entertainment industry cash flow models, and the like. I think that is a lot of nonsense. You have to obtain a whole picture to know if an investment is worthwhile. While cash generation is important in creating that picture so are actual earnings and a whole lot of other financial information found in a company’s annual report.

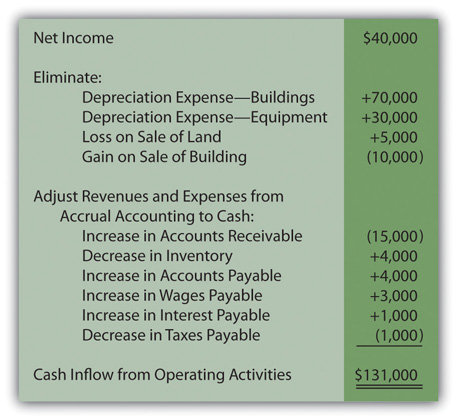

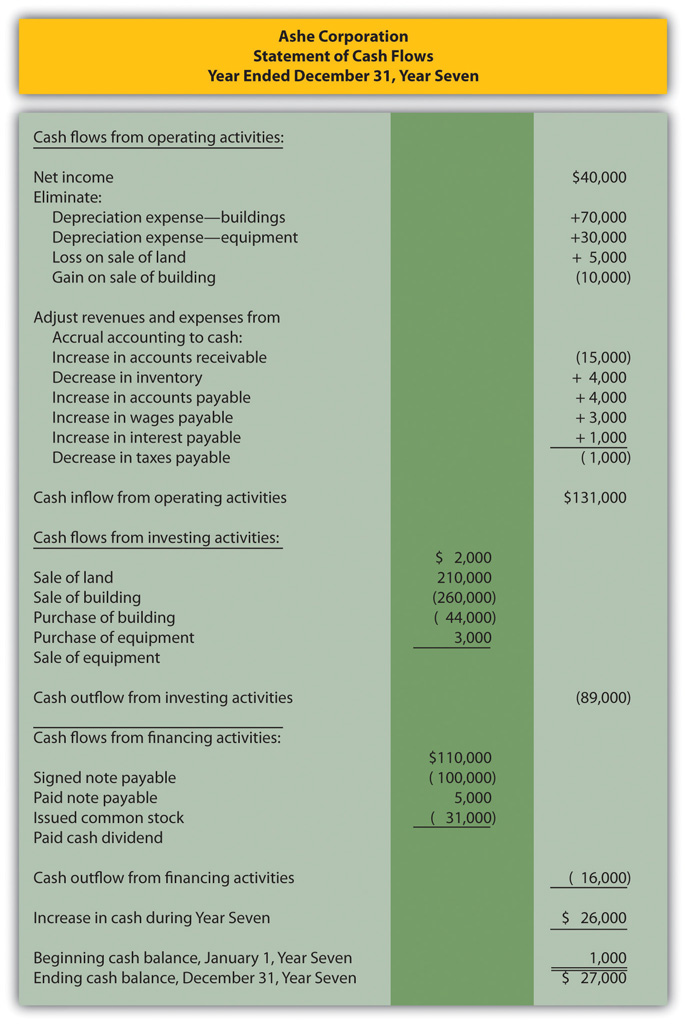

17.5 Appendix: Comprehensive Illustration—Statement of Cash Flows

The Creation of a Complete Statement of Cash Flows

Question: All three sections of the statement of cash flows are presented in this chapter but in separate coverage. Now, through a comprehensive illustration, these categories will be combined into a formal and complete statement.

The following information has been uncovered within the internal records maintained by the Ashe Corporation for Year Seven. The company is a small organization that was incorporated several years ago in the western part of North Carolina.

A few of the significant financial events that occurred during the current year are as follows:

- Land that had cost Ashe $7,000 several years ago was sold to an outside buyer.

- A building was also sold but for $210,000 in cash. This property had an original cost of $230,000. Accumulated depreciation to date on this building was $30,000. This building was replaced with a new purchase made for cash during the year.

- Equipment was purchased for $44,000 in cash to replace other equipment that was sold at the beginning of the year.