This is “In a Set of Financial Statements, What Information Is Conveyed about Other Noncurrent Liabilities?”, chapter 15 from the book Business Accounting (v. 2.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

Chapter 15 In a Set of Financial Statements, What Information Is Conveyed about Other Noncurrent Liabilities?

Video Clip

(click to see video)In this video, Professor Joe Hoyle introduces the essential points covered in Chapter 15 "In a Set of Financial Statements, What Information Is Conveyed about Other Noncurrent Liabilities?".

15.1 Accounting for Leases

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Understand the theoretical difference between an operating lease and a capital lease.

- Recognize that a lessee will be required to account for a lease as either an operating lease or a capital lease based on the specific terms of the contract.

- Understand the concept of off-balance sheet financing.

- Explain the term “substance over form” and how it applies to the financial reporting of a capital lease.

Reporting a Liability for Leased Property

Question: Notes and bonds payable serve as the predominant source of long-term financing in the United States. Virtually all companies raise significant sums of money by incurring debts of this type. However, a quick perusal of the balance sheets of most well-known companies finds a broad array of other noncurrent liabilities, some of staggering size.

- Sears Holdings Corporation disclosed long-term capital lease obligations of $597 million as of January 29, 2011.

- Southwest Airlines Co. reported deferred income tax liabilities of approximately $2.5 billion on December 31, 2010.

- Alcoa Inc. at December 31, 2010, lists $2.6 billion in liabilities (slightly under 12 percent of the company’s total) labeled as accrued postretirement benefitsPromises such as pension payments, health care insurance coverage, and life insurance benefits made by employers to eligible employees to be received after the individuals reach a specified retirement age. (other than pensions).

These noncurrent liabilities represent large amounts of debts that are different from traditional notes and bonds. Some understanding of these balances is necessary to comprehend the information being conveyed in a set of financial statements. The reporting of liabilities such as those above is explored in depth in upper-level financial accounting courses. However, a basic level of knowledge is essential for every potential decision maker, not just those individuals who chose to major in accounting in college.

Lease liabilities will be explored first in this chapter. To illustrate, assume that the Abilene Company needs an airplane to use in its daily operations. Rather than buy this asset, Abilene leases one from a business that owns a variety of aircraft. The lease is for seven years at an annual cost of $100,000. A number of reasons might exist for choosing to lease rather than buy. Perhaps Abilene is able to negotiate especially good terms for the airplane because of the company’s willingness to commit to such a long period of time.

On the day that the lease is signed, should Abilene report a liability and, if so, is the amount just the first $100,000 installment, the $700,000 total of all payments, or some other figure? When a company leases an asset, how is the related liability reported?

Answer: The liability balance to be reported by the Abilene Company cannot be determined based purely on the information that is provided. When a lesseeA party that pays cash for the use of an asset in a lease contract. (the party that will make use of the asset) signs a lease agreement, the transaction is recorded in one of two ways based on the terms of the contract.

Possibility One—An Operating LeaseA rental agreement where the benefits and risks of ownership are not conveyed from the lessor to the lessee.. Abilene might have obtained the use of this airplane through an operating lease, a rental arrangement. If so, the liability recognized when the contract is signed is $100,000, only the amount due immediately. Upon payment, the reported debt is reduced to zero despite the requirement that six more installments have to be paid. In financial accounting, the future payments on an operating lease are viewed as a commitment rather than a liability. Thus, information about those payments is disclosed in the notes to the financial statements but not formally reported.

Possibility Two—A Capital LeaseA rental agreement where the benefits and risks of ownership are conveyed from the lessor to the lessee so that both the asset and liability are reported initially by the lessee at the present value of the cash payments; for accounting purposes, it exists when one of four established criteria are met.. This transaction could also have met specific criteria for classification as a capital lease. That type of lease is viewed as the equivalent of Abilene buying the airplane. The initial liability recognized by Abilene is the present value of the $700,000, the entire amount of cash to be paid over these seven years. The present value is determined by the mathematical removal of a reasonable rate of interest.

Test Yourself

Question:

A lessee signs a lease agreement so that a piece of property can be used for the specified period of time. From an accounting perspective, what are the two types of leases?

- Fixed leases and variable leases

- Operating leases and capital leases

- Income leases and expenditure-based leases

- Noncontractual leases and contractual leases

Answer:

The correct answer is choice b: Operating leases and capital leases.

Explanation:

For the lessee, all leases are classified for financial reporting purposes as either a rental (an operating lease) or the equivalent of a purchase (a capital lease).

Does a Lessee Prefer to Report an Operating or Capital Lease?

Question: The previous answer raises a number of immediate questions about lease accounting. Probably the first of these relates to the practical goal of officials who want to produce financial statements that make their company look as financially healthy as possible. A lease agreement can be reported as (a) an operating lease with only the initial payment recorded as a liability or (b) a capital lease where the present value of all payments (a much larger number) is shown as the liability.

Officials for the lessee must surely prefer to classify all leases as operating leases to reduce the reported debt total. In financial accounting, does a lessee not have a bias to report operating leases rather than capital leases?

Answer: The answer to this question is obviously “Yes.” If an option exists between reporting a larger liability (capital lease) or a smaller one (operating lease), officials for the lessee are inclined to take whatever measures necessary to classify each contract as an operating lease. This is not a choice such as applying FIFO or LIFO. The reporting classification is based on the nature of the agreement.

Thus, Abilene Company will likely attempt to structure the contract for this airplane to meet any designated criteria for an operating lease. Financial accounting is supposed to report events and not influence them. However, at times, authoritative reporting standards impact the method by which companies design the transactions in which they engage.

If the previous example is judged to be an operating lease, Abilene only reports an initial liability of $100,000 although legally bound by the agreement to pay a much larger amount. The term off-balance sheet financingDescription used for an obligation where an amount of money must be paid that is larger than the figure reported on the balance sheet; for a lessee, an operating lease provides an example of off-balance sheet financing. is commonly used when a company is obligated for more money than the reported debt. Operating leases are one of the primary examples of “off-balance sheet financing.”

As mentioned at the start of this chapter, Sears Holdings Corporation reports noncurrent liabilities of about $597 million on January 29, 2011, in connection with capital leases. However, that obligation seems small in comparison to the amount to be paid by the company on its operating leases. As the notes to those financial statements explain, Sears has numerous operating leases (for the use of stores, office facilities, warehouses, computers and transportation equipment) that will require payment of over $5.3 billion in the next few years. Most of the debt for this additional $5.3 billion is “off the balance sheet.” In other words, the obligation is not included in the liability section of the company’s balance sheet. For an operating lease, the reported liability balance does not reflect the total obligation, just the current amount that is due.

Test Yourself

Question:

A lessee is negotiating a new lease for a large piece of property. Which of the following is most likely to be true?

- The lessee will try to structure this contract as an operating lease to take advantage of off-balance sheet financing.

- The lessee will not care whether the contract is viewed as an operating lease or a capital lease.

- The lessee will try to structure this contract as a capital lease to avoid the implications of off-balance sheet financing.

- The lessee will structure the contract in whatever way is most convenient for the lessor (the actual owner of the property).

Answer:

The correct answer is choice a: The lessee will try to structure this contract as an operating lease to take advantage of off-balance sheet financing.

Explanation:

The liability balance reported for an operating lease is only the amount currently due. For most leases, that is a relatively small amount. A lessee will typically prefer to create this type of lease so that the reported liability total is lower. The remainder of the obligation will not be recognized until it comes due. The ability to use accounting rules to omit some amount of debt is commonly known as off-balance sheet financing.

Differentiating an Operating Lease from a Capital Lease

Question: For a lessee, a radical difference in reporting exists between operating leases and capital leases. Company officials prefer to report operating leases so that the amount of liabilities appearing on the balance sheet is lower. What is the distinction between an operating lease and a capital lease?

Answer: In form, all lease agreements are rental arrangements. One party (the lessor) owns legal title to property while the other (the lessee) rents the use of that property for a specified period of time. However, in substance, a lease agreement may go beyond a pure rental agreement. Financial accounting has long held that a fairly presented portrait of an entity’s financial operations and economic health is only achieved by looking past the form of a transaction to report the actual substance of what is taking place. “Substance over form” is a mantra often heard in financial accounting.

Over thirty years ago, U.S. GAAP was created (by FASB) to provide authoritative guidance for the financial reporting of leases. An official pronouncement released at that time states that “a lease that transfers substantially all of the benefits and risks incident to the ownership of property should be accounted for as the acquisition of an asset and the incurrence of an obligation by the lessee.” In simple terms, this standard means that a lessee can obtain such a significant stake in leased property that the transaction more resembles a purchase than it does a rental. If the transaction looks like a purchase, the accounting should be that of a purchase.

When the transaction is more like a purchase, it is recorded as a capital lease. When the transaction is more like a rental, it is recorded as an operating lease.

- Capital lease. The lessee gains substantially all the benefits and risks of ownership. Although legal form is still that of a lease arrangement, the transaction is reported as a purchase at the present value of the future cash flows.

- Operating lease. The lessee does not obtain substantially all the benefits and risks of ownership. The transaction is reported as a rental arrangement.

Test Yourself

Question:

A lessee signs a contract with the word “LEASE” typed across the top. Which of the following statements is true?

- Rental expense will be recognized over the life of this contract.

- If this contract is accounted for as a capital lease, that is an example of reporting substance over form.

- If this contract is accounted for as an operating lease, that is an example of reporting form over substance.

- Because a formal legal document has been created, this lease must be reported as a capital lease.

Answer:

The correct answer is choice b: If this contract is accounted for as a capital lease, that is an example of reporting substance over form.

Explanation:

Although this contract is in the form of a rental arrangement, it must be accounted for as a capital lease if it has the substance of a purchase. Accountants always want to record the substance of a transaction rather than its mere form. Without knowing the information provided in the contract, the accountant cannot determine whether rent expense is appropriate here (an operating lease) or if the arrangement is the equivalent of a purchase (a capital lease).

Criteria for a Capital Lease

Question: A capital lease is accounted for as a purchase because it so closely resembles the acquisition of the asset. An operating lease is more like a rent. The lessee normally prefers to report all such transactions as operating leases to reduce the amount of debt shown on its balance sheet. How does an accountant determine whether a contract qualifies as a capital lease or an operating lease?

Answer: In establishing reporting guidelines in this area, FASB created four specific criteria to serve as the line of demarcation between the two types of leases. Such rules set a standard that all companies must follow. If any one of these criteria is met, the lease is automatically recorded by the lessee as a capital lease. In that case, both the asset and liability are reported as if an actual purchase took place.

Not surprisingly, accountants and other company officials study these four criteria carefully. They hope to determine how the rules can be avoided so that most of their new contracts are viewed as operating leases. Interestingly, in recent years, official groups here and abroad have been examining these rules to decide whether U.S. GAAP and IFRS will be revised so that virtually all leases are reported as capital leases. At this time, the final outcome of those deliberations remains uncertain. However, a serious limitation on the use of the operating lease category seems likely in the next few years.

Criteria to Qualify as a Capital Lease (only one must be met):

- If the lease contract specifies that title to the property will be conveyed to the lessee by the end of the lease term, it is a capital lease. If legal ownership is to be transferred from lessorA party that receives cash for granting the use of owned property to a lessee through a lease contract. to lessee, the entire series of payments is simply a method devised to purchase the asset. From the beginning, the property was being acquired.

- If the contract allows the lessee to buy the property at a specified time at an amount sufficiently below expected fair value (so that a purchase is reasonably assured), it is a capital lease. The availability of this bargain purchase option indicates, once again, that the true intention of the contract is the conveyance of ownership. The transaction is the equivalent of a purchase if the option price is so low that purchase by the lessee can be anticipated.

- If the lease contract is for a term that is equal to 75 percent or more of the estimated life of the property, it is a capital lease. This criterion is different from the first two where the transaction was just a disguised purchased. Here, the lessee will never gain ownership. However, the lease is for such an extensive portion of the asset’s life that the lessee obtains a vast majority of its utility. Although the 75 percent standard is an arbitrary benchmark, no doubt can exist that the lessee will be the primary beneficiary of the property.

- The fourth criterion is too complicated to cover in an introductory textbook. The general idea is that the lessee is paying approximately the same amount as would have been charged to buy the asset. Paying the equivalent of the purchase price (or close to it) indicates that no real difference exists between the nature of the lease transaction and an acquisition.

Test Yourself

Question:

A lessee signs a three-year lease for $79,000 per year to gain use of a machine. The machine has an expected useful life of five years. At the end of this three-year period, the machine is expected to be worth $60,000. The lessee has the right to buy it at that time for $50,000. The required payments are not the equivalent of the acquisition value of this asset. Which of the following is true for the lessee?

- The lease is a capital lease.

- The lease is an operating lease.

- The lease might be a capital lease but not enough information is available.

- The lease will be an operating lease if one of the four criteria is met.

Answer:

The correct answer is choice c: The lease might be a capital lease but not enough information is available.

Explanation:

If one of the four criteria established by FASB is met, this lease is reported as a capital lease. One of the criteria is still in question. Is a $50,000 purchase option viewed as a bargain if the expected fair value is $60,000? Is the $10,000 discount sufficient so that purchase is reasonably assured? Although the rules are clear, those judgments can be extremely difficult to make in practice. Not enough information is provided here to determine whether this purchase option is a bargain.

Key Takeaway

A lessee accounts for a lease contract as either an operating lease or a capital lease depending on the specific terms of the agreement. Officials working for the lessee will likely prefer the contract to qualify as an operating lease because a smaller liability is reported. Thus, the reporting of an operating lease is a common example of off-balance sheet financing because a significant portion of the contractual payments are not included as liabilities on the balance sheet. In contrast, for a capital lease, the present value of all future cash flows must be reported as a liability. To differentiate operating leases from capital leases, four criteria have been established within U.S. GAAP. If any one of these criteria is met, the lessee accounts for the transaction as a capital lease. Although still a lease in legal form, the contract is viewed as a purchase in substance and reported in that manner.

15.2 Operating Leases versus Capital Leases

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Account for an operating lease, realizing that the only liability to be reported is the amount that is currently due.

- Understand that the only asset reported in connection with an operating lease is prepaid rent if payments are made in advance.

- Record the initial entry for a capital lease with both the asset and the liability calculated at the present value of the future cash flows.

- Explain the interest rate to be used by the lessee in determining the present value of a capital lease and the amount of interest expense to be recognized each period.

- Determine and recognize the depreciation of an asset recorded as the result of a capital lease.

The Financial Reporting of an Operating Lease

Question: The Abilene Company has agreed to pay $100,000 per year for seven years to lease an airplane. Assume that legal title will not be received by Abilene and no purchase option is mentioned in the contract. Assume also that the life of the airplane is judged to be ten years and the payments do not approximate the fair value of the item.

The contract is signed on December 31, Year One, with the first annual payment made immediately. Based on the description of the agreement, none of the four criteria for a capital lease have been met. Thus, Abilene has an operating lease. What financial accounting is appropriate for an operating lease?

Answer: None of the four criteria for a capital lease is met in this transaction:

- Legal ownership is not conveyed to the lessee.

- No bargain purchase option is included in the contract.

- The life of the lease is less than 75 percent of the life of asset (seven years out of ten years or 70 percent).

- Payments do not approximate the acquisition value of the asset.

Thus, Abilene is just renting the airplane and agrees on an operating lease. The first annual payment was made immediately to cover the subsequent year.

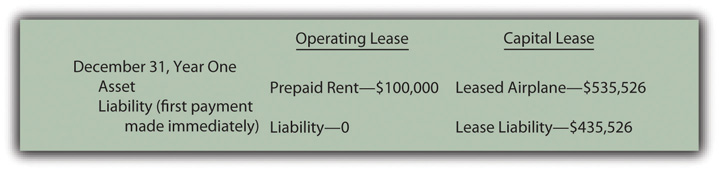

Figure 15.1 December 31, Year One—Payment of First Installment of Operating Lease

Because the first payment has been made, no liability is reported on Abilene’s balance sheet although the contract specifies that an additional $600,000 in payments will be required over the subsequent six years. In addition, the airplane itself is not shown as an asset by the lessee. The operating lease is viewed as the equivalent of a rent and not a purchase.

During Year Two, as time passes, the future value provided by the first prepayment gradually becomes a past value. The asset balance is reclassified as an expense. At the end of that period, the second payment will also be made.

Figure 15.2 December 31, Year Two—Adjustment to Record Rent Expense for Year Two

Figure 15.3 December 31, Year Two—Payment of Second Installment of Operating Lease

Initial Recording of a Capital Lease

Question: One slight change can move this contract from an operating lease to a capital lease. Assume all the information remains the same in the previous example except that the airplane has an expected life of only nine years rather than ten. With that minor alteration, the life of the lease is 77.8 percent of the life of the asset (seven years out of nine years). The contract is now 75 percent or more of the life of the asset. Because one of the criteria is now met, this contract must be viewed as a capital lease. The change in that one estimation creates a major impact on the reporting process. How is a capital lease reported initially by the lessee?

Answer: As a capital lease, the transaction is reported in the same manner as a purchase. Abilene has agreed to pay $100,000 per year for seven years, but no part of this amount is specifically identified as interest. According to U.S. GAAP, if a reasonable rate of interest is not explicitly paid each period, a present value computation is required to split the contractual payments between principal (the amount paid for the airplane) and interest (the amount paid to extend payment over this seven-year period). This accounting is not only appropriate for an actual purchase when payments are made over time but also for a capital lease.

Before the lessee computes the present value of the future cash flows, one issue must be resolved. A determination is needed of the appropriate rate of interest to be applied. In the previous discussion of bonds, a negotiated rate was established between the investor and the issuing company. No such bargained rate exists in connection with a lease. According to U.S. GAAP, the lessee should use its own incremental borrowing rate. That is the interest rate the lessee would be forced to pay to borrow this same amount of money from a bank or other lending institution.As explained in upper-level accounting textbooks, under certain circumstances, the lessee might use the implicit interest rate built into the lease contract by the lessor. Assume here that the incremental borrowing rate for Abilene is 10 percent per year. If the company had signed a loan to buy this airplane instead of lease it, the assumption is that the lender would have demanded an annual interest rate of 10 percent.

Abilene will pay $100,000 annually over these seven years. Because the first payment is made immediately, these payments form an annuity due. As always, the present value calculation computes the interest at the appropriate rate and then removes it to leave the principal: the amount of the debt incurred to obtain the airplane. Once again, present value can be found by table (in the following link or included at the end of this book), by formula, or by Excel spreadsheet.On an Excel spreadsheet, the present value of a $1 per period annuity due for seven periods at an assumed annual interest rate of 10 percent is computed by typing the following data into a cell: =PV(.10,7,1,,1).

Present Value of an Annuity Due of $1

http://www.principlesofaccounting.com/ART/fv.pv.tables/pvforannuitydue.htm

Present value of an annuity due of $1 per year for seven years at a 10 percent annual interest rate is $5.35526. The present value of seven payments of $100,000 is $535,526.

present value = $100,000 × 5.35526 present value = $535,526After the present value has been determined, the recording of the capital lease proceeds very much like a purchase made by signing a long-term liability.

Figure 15.4 December 31, Year One—Capital Lease Recorded at Present Value

Figure 15.5 December 31, Year One—Initial Payment on Capital Lease

A comparison at this point between the reporting of an operating lease and a capital lease is striking. The differences are not inconsequential. For the lessee, good reasons exist for seeking an operating lease rather than a capital lease.

Figure 15.6 Comparison of Initially Reported Amounts for an Operating Lease and for a Capital Lease

Test Yourself

Question:

A company signs a lease on January 1, Year One, to lease a machine for eight years. Payments are $10,000 per year with the first payment made immediately. The company has an incremental borrowing rate of 6 percent. This lease qualifies as a capital lease. The present value of an ordinary annuity of $1 for eight periods at an annual interest rate of 6 percent is $6.20979. The present value of an annuity due of $1 for eight periods at an annual interest rate of 6 percent is $6.58238. If financial statements are produced after this lease has been signed and settled, which of the following balances will be reported (rounded)?

- Leased asset of $62,098 and lease liability of $52,098

- Leased asset of $52,098 and lease liability of $62,098

- Leased asset of $65,824 and lease liability of $55,824

- Leased asset of $55,824 and lease liability of $65,824

Answer:

The correct answer is choice c: Leased asset of $65,824 and lease liability of $55,824.

Explanation:

Because the first payment is made immediately, this contract is classified as an annuity due. As a capital lease, both the asset and the liability are initially reported at the present value of these cash flows at the lessee’s incremental borrowing rate or $65,824 ($10,000 × $6.5824). However, the first $10,000 payment is also made at that time so the liability balance is reduced by that amount.

Accounting for a Capital Lease over Time

Question: In a capital lease, property is not bought but is accounted for as if it had been purchased. When the contract is signed in the previous example, Abilene records both the leased airplane and the liability at the present value of the required cash payments. What reporting takes place subsequent to the initial recording of a capital lease transaction?

Answer: As with any purchase of an asset having a finite life where payments extend into the future, the cost of the asset is depreciated, and interest is recognized in connection with the liability. This process remains the same whether the asset is bought or obtained by capital lease.

Depreciation. The airplane will be used by Abilene for the seven-year life of the lease. The recorded cost of the asset is depreciated over this period to match the expense recognition with the revenue that the airplane helps generate. Assuming the straight-line method is applied, annual depreciation is $76,504 (rounded) or $535,526/seven years.

Interest. The principal of the lease liability during Year Two is $435,526. That balance is the initial $535,526 present value less the first payment of $100,000. The annual interest rate used in determining present value was 10 percent so interest expense of $43,553 (rounded) is recognized for this period of time—the liability principal of $435,526 times this 10 percent annual rate. As in the chapter on bonds and notes, the effective rate method is applied here.

Figure 15.7 December 31, Year Two—Depreciation of Airplane Obtained in Capital Lease

Figure 15.8 December 31, Year Two—Interest on Lease Liability from Capital Lease

Figure 15.9 December 31, Year Two—Second Payment on Capital Lease

Test Yourself

Question:

A company leases a truck for its operations. The accountant is attempting to determine if this lease is a capital lease or an operating lease. Which of the following statements is true?

- The reported liability balance is likely to be higher in an operating lease.

- A prepaid rental account is likely to be reported in a capital lease.

- The leased asset will appear in the financial statements if this is an operating lease.

- Both depreciation expense and interest expense are recognized for a capital lease.

Answer:

The correct answer is choice d: Both depreciation expense and interest expense are recognized for a capital lease.

Explanation:

In an operating lease, a prepaid rent account is established by the cash payments with that amount then reclassified to rent expense as time passes. Little or no liability is reported. In a capital lease, both the asset and the liability are reported at the present value of the future cash payments. The cost attributed to the asset is depreciated while interest expense must be recognized on the liability balance each period.

Talking with an Independent Auditor about International Financial Reporting Standards

Following is a continuation of our interview with Robert A. Vallejo, partner with the accounting firm PricewaterhouseCoopers.

Question: In U.S. GAAP, if a lease arrangement meets any one of four criteria, the transaction is reported as a capital lease. Companies often design transactions to either avoid or meet these criteria based on the desired method of accounting. Do IFRS requirements utilize the same set of criteria to determine whether a capital lease or an operating lease has been created?

Rob Vallejo: This is difficult to answer based on the current status of the FASB and IASB’s joint project on “Leases” that began with a discussion paper in 2009. After receiving a large number of comments on a draft version of a new standard, the FASB and IASB are currently making revisions and will release a new draft version in the first half of 2012. Regardless of the outcome, after the new standard is issued (effective date could be as early as 2014), the distinction between operating and capital leases will be eliminated, as all leases will be treated as finance leases and included on the balance sheet at inception. For organizations that have structured leases to meet the definition of an operating lease, the new standard will have a significant impact. Officials should already be considering the implications to their financial statements and ongoing financial reporting. To check the latest status of the FASB and IASB’s joint project on leases, check the FASB’s web-site, http://www.FASB.org. Currently, a leasing arrangement may well be classified differently under IFRS than under U.S. GAAP. This is an example of where existing U.S. GAAP has rules and IFRS has principles. Under today’s U.S. GAAP, guidance is very specific based on the four rigid criteria established by FASB. However, under IFRS, the guidance focuses on the substance of the transaction and there are no quantitative breakpoints or bright lines to apply. For example, there is no definitive rule such as the “75 percent of the asset’s life” criterion found in U.S. GAAP. IFRS simply asks the question: have all the risks and rewards of ownership been substantially transferred?

Key Takeaway

Operating leases record payment amounts as they come due and are paid. Therefore, the only reported asset is a prepaid rent, and the liability is the current amount due. For a capital lease, the present value of all future cash payments is determined using the incremental borrowing rate of the lessee. The resulting amount is recorded as both the leased asset and the lease liability. The asset is then depreciated over the time that the lessee will make use of it. Interest expense is recorded (along with periodic payments) in connection with the liability as time passes using the effective rate method.

15.3 Recognition of Deferred Income Taxes

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Understand that the recognition of revenues and expenses under U.S. GAAP differs at many critical points from the taxation rules established by the Internal Revenue Code.

- Explain the desire by corporate officials to defer the payment of income taxes.

- Determine the timing for the reporting of a deferred income tax liability and explain the connection of this process to the matching principle.

- Calculate taxable income as well as the related deferred income tax liability when the installment sales method is used.

The Reporting of Deferred Tax Liabilities

Question: At the beginning of this chapter, mention was made that Southwest Airlines reported deferred income taxes at the end of 2010 as a noncurrent liability of $2.5 billion. Such an account balance is not unusual. The Dow Chemical Company listed a similar debt of almost $1.3 billion on its December 31, 2010, balance sheet while Marathon Oil Corporation showed approximately $3.6 billion. What information is conveyed by these huge account balances? How is a deferred income tax liability created?

Answer: The reporting of deferred income tax liabilitiesA balance sheet account indicating that the current payment of an income tax amount has been delayed until a future date; companies often seek to create this deferral so that tax dollars can be used in the interim to increase net income. is, indeed, quite prevalent. One recent survey found that approximately 70 percent of businesses included a deferred tax balance within their noncurrent liabilities.Matthew Calderisi, senior editor, Accounting Trends & Techniques, 63rd edition (New York: American Institute of Certified Public Accountants, 2009), 279. Decision makers need to have a basic understanding of any account that is so commonly encountered in a set of financial statements.

In the earlier discussion of LIFO, the disparity between financial accounting principles and income tax rules was described. In the United States, financial information is presented based on the requirements of U.S. GAAP (created by FASB) whereas income tax reporting is determined according to the Internal Revenue Code (written by Congress). At many places, these two sets of guidelines converge. If a grocery store sells a can of tuna fish for $6 in cash, the revenue is $6 on both the reported financial statements and the income tax return. However, at a number of critical junctures, the recognized amounts can be quite different.

Where legal, companies frequently exploit these differences for their own benefit by delaying tax payments. The deferral of income taxes is usually considered a wise business strategy because the organization is able to use its cash for a longer period of time and, hence, generate additional revenues. When paid, the money is gone, but until then, it can be used to raise net income. For example, if an entity earns a 10 percent return on assets and manages to defer a tax payment of $700 million for one year, the increased profit is $70 million ($700 million × 10 percent).

Businesses commonly attempt to reduce their current taxable income by moving reported gains and revenue into the future. That is one prevalent method for deferring tax payments. Southwest, Dow Chemical, and Marathon likely used this approach to create a portion of the deferred tax liabilities they are reporting. Revenue or a gain might be recognized this year for financial reporting purposes although deferred until an upcoming time period for tax purposes. Consequently, the payment of tax on this income is pushed into that future year. As long as the tax laws are obeyed, such deferral is legal.

Taxable income is reduced in the current period (revenue is moved out) but increased at a later time (the revenue is moved back into taxable income). Because a larger tax will have to be paid in the subsequent period, a deferred income tax liability is created. To illustrate, assume that a business reports revenue of $10,000 on its Year One income statement. Because of tax rules and regulations, assume that this amount will not be subject to income taxation until Year Six. The $10,000 is referred to as a temporary tax differenceA revenue or expense reported for both financial accounting and income tax purposes but in two different time periods; leads to the recognition of deferred income taxes.. It is reported for both financial accounting and tax purposes but in two different time periods.

If the effective tax rate for this business is 40 percent, it reports a $4,000 ($10,000 × 40 percent) deferred income tax liability on its December 31, Year One, balance sheet. The revenue was earned in Year One, so the related expense and liability are also recorded in Year One. This amount will be paid to the government but not until Year Six when the revenue becomes taxable. The revenue is recognized now according to U.S. GAAP but in a later year for income tax purposes. Although, net income is higher in the current year than taxable income, taxable income will be higher in the future by $10,000. Most important, payment of the $4,000 income tax is delayed until Year Six.

Simply put, a deferred income tax liabilityMany companies also report deferred income tax assets that arise because of other differences in U.S. GAAP and the Internal Revenue Code. For example, Southwest Airlines included a deferred income tax asset of $214 million on its December 31, 2010, balance sheet. Accounting for such assets is especially complex and will not be covered in this textbook. Some portion of this asset balance, although certainly not all, is likely to be the equivalent of a prepaid income tax where Southwest was required to make payments by the tax laws in advance of recognition according to U.S. GAAP. is created when an event occurs now that will lead to a higher amount of income tax payment in the future.

Test Yourself

Question:

A company earns $60,000 late in Year One. The tax rate is 25 percent so the tax payment on this income will be $15,000. Because of a specific rule in the Internal Revenue Code, this $60,000 is not taxable until Year Two. Thus, the $15,000 will be paid on March 15, Year Three when the company files its Year Two income tax return. Which of the following statements is true?

- The liability is first recognized in Year One even though payment is not made until Year Three.

- The liability is first recognized in Year Two even though payment is not made until Year Three.

- The liability is not recognized until Year Three when the tax return is filed.

- There is not enough information presented here to determine when the liability should first be recognized.

Answer:

The correct answer is choice a: The liability is first recognized in Year One even though payment is not made until Year Three.

Explanation:

The income is recognized in Year One so the related income tax expense should be recognized in that same period to conform to the matching principle. Because recognition of the income has been delayed for tax purposes, a deferred income tax liability is also reported in Year One to disclose the future payment. The income was earned in Year One according to U.S. GAAP so the related liability must be reported then as well.

The Installment Sales Method and Deferred Income Taxes

Question: Assume that the Hill Company buys an asset (land, for example) for $150,000. Later, this asset is sold for $250,000 during Year One. The earning process is substantially complete at that point. Hill reports a gain on its Year One income statement of $100,000 ($250,000 less $150,000). Because of the terms of the sales contract, this money will not be collected from the buyer until Year Five. The buyer is financially strong and should be able to pay at the required times. Hill’s effective tax rate for this transaction is 30 percent.

Officials for Hill are pleased to recognize the $100,000 gain on this sale in Year One because it makes the company looks better. However, they prefer to wait as long as possible to pay the income tax especially since no cash has yet been collected. How can the recognition of income for tax purposes be delayed, thereby creating the need to report a deferred income tax liability?

Answer: According to U.S. GAAP, this $100,000 gain is recognized on Hill Company’s income statement in Year One based on accrual accounting. The earning process is substantially complete and the amount to be collected can be reasonably estimated. However, if certain conditions are met, income tax laws permit taxpayers to report such gains using the installment sales method.The installment sales method can also be used for financial reporting purposes but only under very limited circumstances. In simple terms, the installment sales method allows a seller to delay reporting a gain for tax purposes until cash is collected. In this illustration, no cash is received in Year One, so no taxable income is reported. The tax will be paid in Year Five when Hill collects the cash. Thus, as shown in Figure 15.10 "Year One—Comparison of Financial Reporting and Tax Reporting", the income is reported now on the financial statements but not until Year Five for tax purposes.

Figure 15.10 Year One—Comparison of Financial Reporting and Tax Reporting

The eventual tax to be paid on the gain will be $30,000 ($100,000 × 30 percent). How is this $30,000 reported in Year One if payment to the government is not required until Year Five?

- First, because of the matching principle, the income tax expense of $30,000 must be recorded in Year One. The $100,000 gain is reported on the income statement in that year; therefore, any related expense is recognized in the same period. That is the basic premise of the matching principle.

- Second, the $100,000 gain creates a temporary difference. The amount will become taxable when the cash is collected in Year Five. At that time, a tax payment of $30,000 is required. Accountants have long debated whether this liability is created when the income is earned (Year One) or when the payment is to be made (Year Five). Legally, the company does not owe any money to the government until the Year Five income tax return is filed. However, reporting guidance provided by U.S. GAAP holds that recognition of the gain in Year One is the event that creates the probable future sacrifice. Thus, the liability is recognized immediately; a deferred income tax liability must be reported.

Consequently, the adjusting entry shown in Figure 15.11 "December 31, Year One—Recognition of Deferred Income Tax on Gain" is prepared at the end of Year One so that both the expense and the liability are properly reported.

Figure 15.11 December 31, Year One—Recognition of Deferred Income Tax on Gain

In Year Five, when the cash is received from the sale, Hill will report the $100,000 gain on its income tax return. The resulting $30,000 payment to the government eliminates the deferred income tax liability. However, as shown in Figure 15.11 "December 31, Year One—Recognition of Deferred Income Tax on Gain", the income tax expense was reported back in Year One when the original sale was recognized for financial reporting purposes.

Test Yourself

Question:

A local business buys property for $80,000 and later sells it for $200,000. Payments will be collected equally over this year and the following three. The profit is recognized immediately for financial reporting purposes. For tax purposes, assume that this transaction qualified for use of the installment sales method. The business’s effective tax rate is 20 percent. What amount of deferred income tax liability should this entity recognize as of December 31, Year One?

- Zero

- $18,000

- $24,000

- $30,000

Answer:

The correct answer is choice b: $18,000.

Explanation:

The company makes a profit of $120,000 ($200,000-$80,000). Using the installment sales method, the gain is taxed when cash is collected. Because 25 percent of the cash is collected in the first year, $30,000 of that profit (25 percent × $120,000) is recognized immediately for tax purposes. Only the remaining $90,000 ($120,000 less $30,000) is deferred until later years for tax purposes. At a rate of 20 percent, the deferred tax liability is $18,000 ($90,000 × 20 percent).

Key Takeaway

U.S. GAAP and the Internal Revenue Code are created by separate groups with different goals in mind. Consequently, many differences exist as to amounts and timing of income recognition. The management of a business will try to use these differences to postpone payment of income taxes so that the money can remain in use and generate additional profits. Although payment is not made immediately, the matching principle requires the income tax expense to be reported in the same time period as the related revenue. If payment is delayed, a deferred income tax liability is created that remains in the financial records until the income becomes taxable. One of the most common methods for deferring income tax payments is application of the installment sales method. For financial reporting purposes, any gain is recorded immediately as is the related income tax expense. However, according to tax laws, recognition of the profit can be delayed until cash is collected. In the interim, a deferred tax liability is reported to alert decision makers to the eventual payment that will be required.

15.4 Reporting Postretirement Benefits

Learning Objectives

At the end of this section, students should be able to meet the following objectives:

- Define the term “postretirement benefits.”

- Explain the accounting problems associated with the recognition of accrued postretirement benefits.

- List the steps that are followed to determine a company’s reported obligation for postretirement benefits.

- Identify the role of the actuary in accounting for postretirement benefits.

- Calculate a company’s debt-to-equity ratio and explain its meaning.

- Calculate the times interest earned ratio and explain its meaning.

Liability for Postretirement Benefits

Question: According to the information provided at the beginning of this chapter, Alcoa reported a $2.6 billion liability at the end of 2010 for accrued postretirement benefits. What constitutes a postretirement benefit?

Answer: In a note to the 2010 financial statements, Alcoa explains part of this liability as follows:

“Alcoa also maintains health care and life insurance benefit plans covering eligible U.S. retired employees and certain retirees from foreign locations. Generally, the medical plans pay a percentage of medical expenses, reduced by deductibles and other coverages. These plans are generally unfunded, except for certain benefits funded through a trust. Life benefits are generally provided by insurance contracts. Alcoa retains the right, subject to existing agreements, to change or eliminate these benefits.”

Postretirement benefits cover a broad array of promises that companies make to their employees to boost morale and keep them from seeking other jobs. According to this note disclosure, Alcoa provides two of the most common: health care insurance and life insurance. Based on stipulations as to eligibility, Alcoa helps its employees by paying a portion of these insurance costs even after they have retired. Alcoa apparently continues to provide these payments as a reward for years of employee service.

Determining a Liability for Postretirement Benefits

Question: Assume that one of the employees for the Michigan Company is currently thirty-four years old and is entitled to certain postretirement benefits starting at the age of sixty-five. The company has promised to continue paying health care and life insurance premiums for all retirees as long as they live.Health care and life insurance benefits paid by an employer while an employee is still working do not pose an accounting issue. The costs are known and can be expensed as incurred. These expenses are matched with the revenues being generated by the employees at the current time. For this employee, no postretirement benefits will be paid for the next thirty-one years (65 less 34). After that, an unknown payment amount will begin and continue for an unknown period of time. In one of the opening chapters of this book, the challenge presented to accountants as a result of future uncertainty was discussed. Probably no better example of uncertainty can be found than postretirement benefits. Payments may continue for decades and neither their amount nor their duration is more than a guess.

The employee is helping the company generate revenues currently so that, as always, the related expense should be recognized now according to the matching principle. Although this obligation might not be paid for many years, both the expense and related liability are recorded when the person is actually working for the company and earning these benefits.

How is the amount of this liability possibly determined? An employee might retire at sixty-five and then die at sixty-six or live to be ninety-nine. Plus, estimating the cost of insurance (especially medical insurance) over several decades into the future seems to be a virtually impossible challenge. The skyrocketing cost of health care is difficult to anticipate months in advance, let alone decades. The dollar amount of the company’s obligation for these future costs appears to be a nebulous figure at best. In this textbook, previous liabilities have been contractual or at least subject to a reasonable estimation prior to recognition. How is the liability calculated that will be reported by a company for the postretirement benefits promised to its employees?

Answer: As shown by the Alcoa example, postretirement benefits are estimated and reported according to U.S. GAAP while employees work. Because of the length of time involved and the large number of variables (some of which, such as future health care costs, are quite volatile), a precise determination of this liability is impossible. In fact, this liability might be the most uncertain number found on any set of financial statements. Apparently, reporting a dollar amount for postretirement benefits, despite its inexactness, is more helpful than omitting the expense and liability entirely. However, decision makers need to understand that these reported balances are no more than approximations.

The actual computation and reporting of postretirement benefits is more complicated than can be covered adequately in an introductory financial accounting textbook. An overview of the basic steps, though, is useful in helping decision makers understand the information that is provided.

To arrive at the liability to be reported for postretirement benefits that are earned now but only paid after retirement, the Michigan Company takes two primary steps. First, an actuaryAn individual who mathematically computes the likelihood of future events. calculates an estimation of the cash amounts that will eventually have to be paid as a result of the terms promised to employees. “An actuary is a business professional who analyzes the financial consequences of risk. Actuaries use mathematics, statistics, and financial theory to study uncertain future events, especially those of concern to insurance and pension programs.”http://www.math.purdue.edu/academic/actuary/what.php?p=what. In simpler terms, an actuary is a mathematical expert who computes the likelihood of future events.

To make a reasonable guess at the amount of postretirement benefits, the actuary has to make a number of difficult estimations such as the average length of time employees will live and the future costs of health care and life insurance (and any other benefits provided to retirees). For example, an actuary’s calculations might indicate that these costs will average $10,000 per year for the twenty years that an employee is expected to live following retirement.

The future payments to be made by the company are estimated by an actuary, but they are projected decades into the future. Thus, as the second step in this process, the present value of these amounts is calculated to derive the figure to be reported currently on the balance sheet. Once again, as in previous chapters, interest for this period of time is determined mathematically and removed to leave just the principal of the obligation as of the balance sheet date. That is the amount reported by the employer within noncurrent liabilities.

| Determining Accrued Postretirement Benefits |

|---|

| Step One: Estimate Future Payments |

| Step Two: Calculate Present Value of Estimated Future Payments |

Test Yourself

Question:

The Johnson Corporation hires 100 employees in Year One. At that time, the organization makes a promise to each of its employees. If they will work for Johnson for twenty years, the company will pay for the college education of all their children. At that time, none of the employees has a child who will start college until after the next six years. Which of the following statements is true?

- The company should report an expense and a liability at the end of Year One.

- The company should start reporting an expense and a liability after six years.

- The company should start reporting an expense in Year One but no liability.

- The company will never report this promise as an expense and a liability.

Answer:

The correct answer is choice a: The company should report an expense and a liability at the end of Year One.

Explanation:

Johnson Corporation has begun to incur an expected cost in connection with future benefits for its employees. The related expense should be recognized beginning in Year One because these employees are working to generate revenues. An actuary can estimate the eventual cost of this promise based on the amount of work performed to date. A present value computation will then be made to determine the amount of this expense and liability that are applicable to the first year.

The Consequences of Having to Report a Liability

Question: Alcoa recognizes an accrued postretirement benefit liability on its balance sheet of $2.6 billion. This number is the present value of the estimated amounts that the company will have to pay starting when each employee retires. Except for the inherent level of uncertainty, this accounting seems reasonable. At one time decades ago, companies were not required to recognize this obligation. The liability was ignored and costs were simply expensed as paid. Only after advanced computer technology and sophisticated mathematical formulas became available was the reporting of this liability mandated. What is the impact of reporting postretirement benefits if the numbers can only be approximated?

Answer: Organizations typically prefer not to report balances that appear to weaken the portrait of their economic health and vitality. However, better decisions are made by all parties when relevant information is readily available. Transparency is a primary goal of financial accounting. Arguments can be made that some part of the problems that many businesses currently face are the result of promises that were made over past decades where the eventual costs were not properly understood.

As the result of the evolution of U.S. GAAP, decision makers (both inside and outside the company) can now better see the costs associated with postretirement benefits. Not surprisingly, once disclosed, some companies opted to cut back on the amounts promised to retirees. The note disclosure quoted previously for Alcoa goes on further to say, “All U.S. salaried and certain hourly employees hired after January 1, 2002 are not eligible for postretirement health care benefits. All U.S. salaried and certain hourly employees that retire on or after April 1, 2008 are not eligible for postretirement life insurance benefits” (emphasis added).

For the employees directly impacted, these decisions may have been understandably alarming. However, by forcing the company to recognize this liability, U.S. GAAP has helped draw attention to the costs of making such promises.

Test Yourself

Question:

On its most recent balance sheet, the Randle Company reports a noncurrent liability of $30 million as an accrued postretirement benefit obligation. Which of the following statements is least likely to be true?

- The amount to be paid will be more than $30 million.

- The company will have the $30 million in cash payments scheduled out at set times.

- The $30 million figure is a culmination of a number of difficult estimations.

- This liability could extend into the future for several decades.

Answer:

The correct answer is choice b: The company will have the $30 million in cash payments scheduled out at set times.

Explanation:

Postretirement benefits are amounts that a company will pay years into the future, often based on the life expectancy of retirees. After amounts are determined based on several estimates, cash payments are reduced to present value for reporting purposes. Because of the length of time involved, present value is often much less than the anticipated cash payments. Determination of the exact amount and timing of payments is subject to many variables that are not yet known such as life expectancy.

Vital Signs Studied in Connection with Liabilities

Question: In previous chapters, various vital signs have been examined—numbers, ratios, and the like—that assist decision makers in evaluating an entity’s financial condition and future prospects. In connection with liabilities, do specific vital signs exist that are frequently relied on to help assess the economic health of a business or other organization?

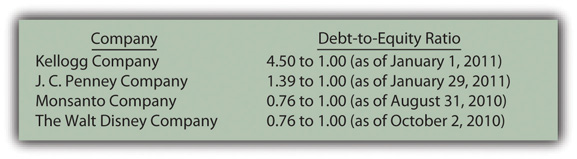

Answer: One vital sign that is often studied by decision makers is the debt-to-equity ratioA measure of a company’s use of debt for financing purposes; it is computed by dividing total liabilities by total stockholders’ equity.. This figure is simply the total liabilities reported by a company divided by total stockholders’ equity. The resulting number indicates whether most of a company’s assets have come from borrowing and other debt or from its own operations and owners. A high debt-to-equity ratio indicates that a company is highly leveraged. As discussed previously, that raises the level of risk but also increases the possible profits earned by stockholders. Relying on debt financing makes a company more vulnerable to bankruptcy and other financial problems but also provides owners with the chance for higher financial rewards.

Recent debt-to-equity ratios presented in Figure 15.12 "Recent Debt-to-Equity Ratios for Several Prominent Companies" for several prominent companies show a wide range of results. No single financing strategy is evident here. The debt-to-equity ratio indicates a company’s policy toward debt, but other factors are involved. For example, in some industries, debt levels tend to be higher than in others. Also, individual responses to the recent economic recession might have impacted some companies more than others.

Figure 15.12 Recent Debt-to-Equity Ratios for Several Prominent Companies

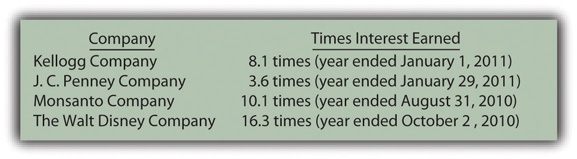

Another method to evaluate the potential problem posed by a company’s debts is to compute the times interest earned (TIE)A measure of a company’s ability to meet obligations as they come due; it is computed by taking EBIT (earnings before interest and taxes) and dividing that number by interest expense for the period. ratio. Normally, debt only becomes a risk if interest cannot be paid when due. This calculation helps measure how easily a company has been able to meet its interest obligations through current operations.

Times interest earned begins with the company’s net income before both interest expense and income taxes are removed (a number commonly referred to as “EBIT” or “earnings before interest and taxes”). Interest expense for the period is then divided into this income figure. For example, if EBIT is $500,000 and interest expense is $100,000, the reporting company earned enough during the year to cover the required interest obligations five times.

Figure 15.13 Recent Times Interest Earned for Several Prominent Companies

Test Yourself

Question:

The owners of a company contribute $100,000 to acquire its capital stock. Another $200,000 is borrowed from a bank. In its first year, the company earns a reported net income of $50,000. If the company then pays a cash dividend of $10,000, what is the impact of this distribution on the debt-to-equity ratio?

- There is no effect on the debt-to-equity ratio.

- It goes up. It was 1.33 to 1.00 and now is 1.43 to 1.00.

- It goes down. It was 1.33 to 1.00 and now is 1.25 to 1.00.

- It goes down. It was 1.43 to 1.00 and now is 1.33 to 1.00.

Answer:

The correct answer is choice b: It goes up. It was 1.33 to 1.00 and now is 1.43 to 1.00.

Explanation:

The company has one debt of $200,000. Before the dividend, stockholders’ equity is $150,000 ($100,000 in contributed capital and $50,000 in retained earnings). The debt-to-equity ratio is $200,000/$150,000 or 1.33 to 1.00. The dividend reduces retained earnings (this portion of net income is distributed to stockholders rather than leaving the assets in the business) to $40,000. Stockholders’ equity has dropped to $140,000. The debt-to-equity ratio is $200,000/$140,000 or 1.43 to 1.00.

Key Takeaway

Businesses and other organizations often promise benefits (such as health care and life insurance) to eligible employees to cover the years after they reach retirement age. Determining the liability balance to be reported at the current time poses a significant challenge for accountants because eventual payment amounts are so uncertain. An actuary uses historical data, computer programs, and statistical models to estimate these amounts. The present value of the projected cash payments is then calculated and recognized by the company as a noncurrent liability. The size of this debt can be quite large but the numbers are no more than approximations. Decision makers often analyze the level of a company’s debt by computing the debt-to-equity ratio and the times interest earned ratio. Both of these calculations help decision makers evaluate the risk and possible advantage of the current degree of debt financing.

Talking with a Real Investing Pro (Continued)

Following is a continuation of our interview with Kevin G. Burns.

Question: Lease arrangements are quite common in today’s business environment. For a capital lease, the present value of the future payments is reported by the lessee as a liability. In contrast, for an operating lease, only the amount currently due is included on the balance sheet as a liability. The reporting of such off-balance sheet financing has been criticized because businesses often go out of their way to create operating leases to minimize the total shown for their debts. However, information about these operating leases must be clearly disclosed in the notes to the financial statements. Are you concerned when you see a company with a lot of off-balance sheet financing? Would you prefer a system where companies had to report more of their debts from leasing arrangements? Do you believe off-balance sheet financing is a problem for the users of financial accounting information?

Kevin Burns: I hate off balance sheet financing. It is trickery in my opinion. As usual, I prefer full or even too much disclosure. A lease is a liability. It should be categorized as such. It is really quite simple—show the liability. Having information in the notes helps but liabilities should be reported on the balance sheet for all to see easily. Anything that reduces transparency is bad for the accounting industry and the people relying on reported financial information.

Obviously, I prefer for companies to have less debt. But, there are exceptions. I own a stake in a company that has a large building that has had a significant appreciation in value. Because they use that building, they cannot take advantage of that increase in value. I suggested to the management that they sell the building to get all of that money and then lease the building back so they could still use it. They would have to report the liability for the lease, but they get their money in a usable form right now, and they can remain in the building.

Video Clip

(click to see video)Professor Joe Hoyle talks about the five most important points in Chapter 15 "In a Set of Financial Statements, What Information Is Conveyed about Other Noncurrent Liabilities?".

15.5 End-of-Chapter Exercises

Questions

- The Ace Company buys a large piece of equipment, which it immediately leases to Zebra Corporation for five years. Which company is the lessor and which company is the lessee?

- In simplest terms, what is an operating lease? In simplest terms, what is a capital lease?

- On December 31, Year One, a company agrees to pay $100,000 per year for the next nine years to lease a large piece of machinery. The first payment is made when the contract is signed. If the contract qualifies as an operating lease, what appears on this company’s balance sheet at December 31, Year One?

- Use the information in question 3 to explain the term “off-balance sheet financing.”

- On December 31, Year One, a company agrees to pay a set amount each year for six years to lease a large truck for hauling purposes. The first payment is made when the contract is signed. If this contract qualifies as a capital lease, what appears on this company’s balance sheet at December 31, Year One?

- A five-year lease is signed. At the end of that time, the lessee can buy the leased asset for an amount of money that is viewed as a bargain. Why does this option make the contract a capital lease?

- A lease is signed for property that has an expected life of ten years. The lease is for only eight years. Why does the length of this lease require the parties to record it as a capital lease?

- How many of the four official criteria must be met to require capital lease accounting?

- A company believes that its incremental borrowing rate is 7 percent. What is meant by the term “incremental borrowing rate?”

- A company is negotiating to lease an asset for use in its business operations. Why will company officials attempt to structure the agreement as an operating lease rather than as a capital lease?

- On January 1, Year One, the Atkins Corporation signs a four-year lease with the first payment made immediately. If this contract is an operating lease, what type of expense or expenses will be recognized at the end of Year One?

- On January 1, Year One, the Carleton Company signs a five-year lease with the first payment made immediately. If this contract is a capital lease, what type of expense or expenses will be recognized at the end of Year One?

- A company leases a building for eighteen years and records it as a capital lease. Why does the handling of this lease illustrate the desire of accountants to report substance over form?

- The Marlento Company reports net income in Year One for financial reporting purposes of $983,000. However, when the company prepares its income tax return for Year One, taxable income is shown as only $536,000. In general, why are these two income totals different?

- What is meant by the term “temporary tax difference?”

- The Wyndsoki Corporation reports a gain of $3 million in Year One. For income tax purposes, the gain is not taxable until Year Four. Will company officials be happy with this delay? Why or why not?

- The Lendmor Corporation earns income of $1.2 million in Year One before income taxes. However, by careful planning, all of this income has been deferred for tax purposes until Year Four. Assume that the tax rate is 30 percent. What adjusting entry, if any, is made for income taxes at the end of Year One?

- The Astomori Corporation buys land for $300,000 in Year One and sells it for $400,000 in Year Two. The company collects half of this money in Year Three and the other half in Year Four. Assume that the tax rate is 30 percent. In what year is the income tax expense recognized on this gain? What journal entry or adjusting entry is used to record the income tax expense at the end of Year Two?

- Jane Buenti-Jones is hired by the Cleveland Corporation. She is thirty years old. The company promises to pay her medical insurance while she works for the company and also after she retires. What is the accounting problem that the company faces here?

- The Abraham Company informs all employees that their life insurance will be paid by the company each year after they retire. What must be done to determine the amounts to be reported on the company’s financial statements in the current year?

- What role does an actuary play in accounting for postretirement benefits?

- What impact can the reporting of postretirement benefits have on company employees?

- A financial analyst mentions that a certain company reports EBIT of $1.4 million. What does EBIT represent?

- The James Company reports liabilities of $3.5 million and stockholders’ equity of $2.0 million. Then, just before the end of the current year, the company pays off a long-term liability with $500,000 in cash. What was the impact of that payment on James Company’s debt-to-equity ratio?

- A company reports a number of figures on its income statement including rent expense of $600,000, interest expense of $500,000, and income tax expense of $400,000. The company’s net income was shown as $1.8 million. Compute the times interest earned ratio for this company.

True or False

- ____ A lessee that is reporting the effects of a capital lease will record depreciation expense on the leased property.

- ____ A capital lease is a common example of off-balance sheet financing.

- ____ A lessee negotiates the lease of a piece of equipment. The lessee will likely attempt to structure the lease as an operating lease.

- ____ A lease has been signed that meets only two of the four criteria for a capital lease. Thus, this transaction will be recorded as an operating lease.

- ____ Lessees usually prefer to record leases as operating leases rather than capital leases.

- ____ Depreciation and interest are both recorded by a lessee in connection with a capital lease, but not an operating lease.

- ____ A lease is signed on December 31, Year One, that calls for annual payments of $20,000. The present value of these payments is $73,000. The lease is an operating lease. On its December 31, Year One, balance sheet, the company will record a liability of $53,000.

- ____ A lease contract is for six years although the asset has an expected life of twelve years. The lessee can buy the asset at the end of six years for $14,000. The lease has to be recorded as a capital asset.

- ____ On January 1, Year One, a lease is signed that is a capital lease. The cash payments are $10,000 per year starting on January 1, Year One. The present value of the cash flows before the first payment is $65,860. If the incremental borrowing rate is 10 percent, the lessee recognizes interest of $6,586 for the first year.

- ____ A company’s Year One income statement reports net income of $348,000. The company’s taxable income for that same year will also be $348,000.

- ____ If a gain is earned in Year One but taxed in Year Three, the related expense is reported in Year One.

- ____ If a gain is earned in Year One but taxed in Year Three, a deferred tax liability is reported at the end of Year One.

- ____ The deferral of income tax payments is viewed as a strategy for increasing reported net income.

- ____ When using the installment sales method for tax purposes, gains are generally taxed when the sale is made.

- ____ Postretirement benefits are not expensed until they are paid.

- ____ The liability recorded for postretirement benefits reflects a factual number that is known by company officials.

- ____ Because Melody Stuart works for a company this year, an expense will be recorded in connection with benefits that she will receive after her retirement in 2020.

- ____ Companies work to reduce their debt-to-equity ratio because of the risk that this figure reflects.

- ____ The computation of times interest earned is found by dividing interest expense for the period by the total amount of noncurrent liabilities.

Multiple Choice

-

Wichita Corporation leases a large machine with a life of twenty years. Which of the following does not necessitate reporting this contract as a capital lease?

- The lease is only for sixteen years.

- At the end of the lease, Wichita can (but doesn’t have to) buy the machine at an amount significantly below expected fair value.

- At the end of twelve years, title to the machine goes to Wichita.

- Wichita will pay a smaller amount each year over a lease life of fourteen years.

-

Sizemore Corporation leases a building to use for the next twenty years. Which of the following is true about Sizemore’s reporting?

- If this contract is a capital lease, rent expense is recognized each period.

- If this contract is an operating lease, depreciation expense is recognized each period.

- If this contract is an operating lease, interest expense and rent expense are recognized each period.

- If this contract is a capital lease, depreciation expense and interest expense are recognized each period.

-

Albemarle Corporation leases a truck for six years and is trying to determine whether the contract qualifies as an operating lease or a capital lease. Which of the following is true?

- Albemarle will want the lease to be a capital lease because less interest is reported.

- Albemarle will want the lease to be a capital lease because less depreciation is reported.

- Albemarle will want the lease to be an operating lease because the reported liability will be lower.

- Albemarle will want the lease to be an operating lease because the reported asset balance will be larger.

-

Myers Company leases a boat on January 1, Year One. The lease does qualify as a capital lease. The lease covers four years, with payments of $20,000 annually, beginning on January 1, Year One. The expected life of the boat is six years. Myers annual incremental borrowing rate is 5 percent. The present value of an ordinary annuity for four years at a 5 percent rate is $3.54595. The present value of an annuity due for four years at a 5 percent rate is $3.72325. What amount of depreciation (rounded) should Myers recognize on the boat for Year One if Myers chooses to use the straight-line method?

- $12,411

- $13,616

- $17,730

- $18,616

-

Charlotte Company leases a piece of equipment on February 1. The lease covers two years although the life of the equipment is four years. The contract contains no bargain purchase option, the equipment does not transfer to Charlotte at the end of the lease, and the payments do not approximate the fair value of the equipment. The annual payments are $4,000 due each February 1, starting with the current one. Charlotte’s incremental borrow rate is 5 percent. The present value of an annuity due of $1 at a 5 percent interest rate for two years is $1.95238. What journal entry or entries should Charlotte make on February 1?

-

Figure 15.14

-

Figure 15.15

-

Figure 15.16

-

Figure 15.17

-

-

On December 31, Year One, the Brangdon Corporation leases a truck to use in its operations. The truck has a life of ten years, although the lease is only for six years. Payments are $10,000 per year with the first payment made immediately. No interest payments are made but Brangsdon has an incremental borrowing rate of 9 percent. The present value of an annuity due at a 9 percent rate for six periods is $4.88965. The present value of an ordinary annuity at a 9 percent rate for six periods is $4.48592. If this is an operating lease, what figure is recorded initially as the capitalized cost of the truck?

- Zero

- $38,897

- $44,859

- $48,897

-

On December 31, Year One, the Sliyvoid Corporation leases a large machine for five years, its entire expected life. Depreciation is recorded using the straight-line method. Payments are $12,000 per year starting on December 31, Year One, and every December 31 thereafter. The incremental borrowing rate is 10 percent per year. The present value of an annuity due at a 10 percent rate for five periods is $4.16987. The present value of an ordinary annuity at a 10 percent rate for five periods is $3.79079. What is the net book value of the leased asset on December 31, Year Two?

- $30,431

- $36,392

- $37,875

- $40,030