This is “Summary and Exercises”, section 22.5 from the book The Legal Environment and Business Law (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

22.5 Summary and Exercises

Summary

Commercial paper is the collective term for a variety of instruments—including checks, certificates of deposit, and notes—that are used to pay for goods; commercial paper is basically a contract to pay money. The key to the central role of commercial paper is negotiability, the means by which a person is empowered to transfer to another more than what the transferor himself possesses. The law regulating negotiability is Article 3 of the Universal Commercial Code.

Commercial paper can be divided into two basic types: the draft and the note. A draft is a document prepared by a drawer ordering the drawee to remit a stated sum of money to the payee. Drafts can be subdivided into two categories: sight drafts and time drafts. A note is a written promise to pay a specified sum of money on demand or at a definite time.

A special form of draft is the common bank check, a draft drawn on a bank and payable on demand. A special form of note is the certificate of deposit, a written acknowledgment by a bank that it has received money and agrees to repay it at a time specified in the certificate.

In addition to drawers, makers, drawees, and payees, one can deal with commercial paper in five other capacities: as indorsers, indorsees, holders, holders in due course, and accommodation parties.

A holder of a negotiable instrument must be able to ascertain all essential terms from its face. These terms are that the instrument (1) be in writing, (2) be signed by the maker or drawer, (3) contain an unconditional promise or order to pay (4) a sum certain in money, (5) be payable on demand or at a definite time, and (6) be payable to order or to bearer. If one of these terms is missing, the document is not negotiable, unless it is filled in before being negotiated according to authority given.

Exercises

- Golf Inc. manufactures golf balls. Jack orders 1,000 balls from Golf and promises to pay $4,000 two weeks after delivery. Golf Inc. delivers the balls and assigns its contract rights to First Bank for $3,500. Golf Inc. then declares bankruptcy. May First Bank collect $3,500 from Jack? Explain.

- Assume in problem 1 that Jack gives Golf Inc. a nonnegotiable note for $3,500 and Golf sells the note to the bank shortly after delivering the balls. May the bank collect the $3,500? Would the result be different if the note were negotiable? Explain.

- George decides to purchase a new stereo system on credit. He signs two documents—a contract and a note. The note states that it is given “in payment for the stereo” and “if stereo is not delivered by July 2, the note is cancelled.” Is the note negotiable? Explain.

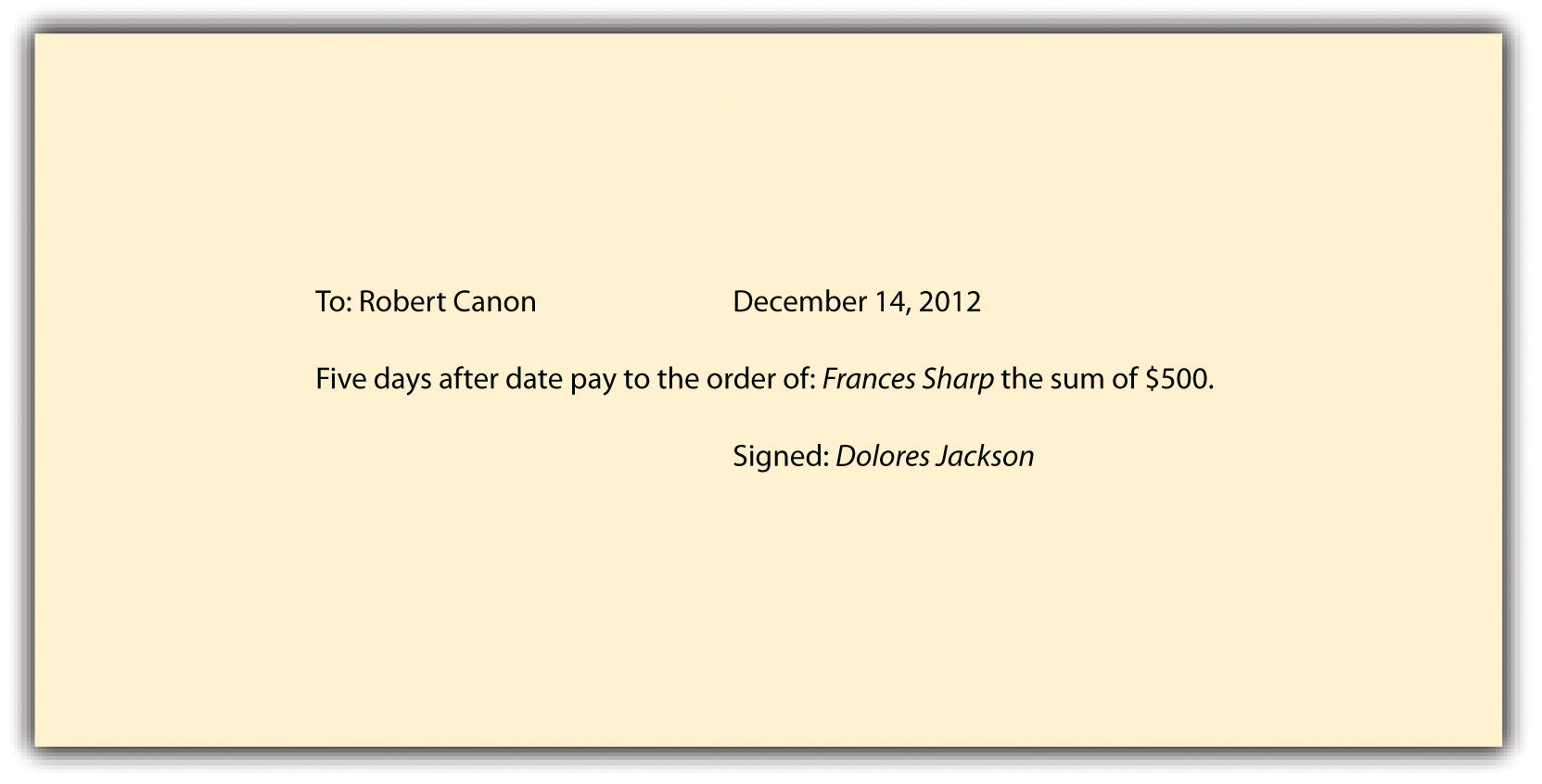

-

Is the following instrument a note, check, or draft? Explain.

Figure 22.7

-

State whether the following provisions in an instrument otherwise in the proper form make the instrument nonnegotiable and explain why:

- A note stating, “This note is secured by a mortgage of the same date on property located at 1436 Dayton Street, Jameson, New York”

- A note for $25,000 payable in twenty installments of $1,250 each that provides, “In the event the maker dies all unpaid installments are cancelled”

- An instrument reading, “I.O.U., Rachel Donaldson, $3,000”

- A note reading, “I promise to pay Rachel Donaldson $3,000”

- A note stating, “In accordance with our telephone conversation of January 7th, I promise to pay Sally Wilkenson or order $1,500”

- An undated note for $1,500 “payable one year after date”

- A note for $1,500 “payable to the order of Marty Dooley, six months after Nick Solster’s death”

- A note for $18,000 payable in regular installments also stating, “In the event any installment is not made as provided here, the entire amount remaining unpaid may become due immediately”

- Lou enters into a contract to buy Alan’s car and gives Alan an instrument that states, “This acknowledges my debt to Alan in the amount of $10,000 that I owe on my purchase of the 2008 Saturn automobile I bought from him today.” Alan assigns the note to Judy for $8,000. Alan had represented to Lou that the car had 20,000 miles on it, but when Lou discovered the car had 120,000 miles he refused to make further payments on the note. Can Judy successfully collect from Lou? Explain.

- The same facts as above are true, but the instrument Lou delivered to Alan reads, “I promise to pay to Alan or order $10,000 that I owe on my purchase of the 2008 automobile I bought from him today.” Can Judy successfully collect from Lou? Explain.

- Joe Mallen, of Sequim, Washington, was angry after being cited by a US Fish and Wildlife Service for walking his dog without a leash in a federal bird refuge. He was also aggravated with his local bank because it held an out-of-state check made out to Mallen for ten days before honoring it. To vent his anger at both, Mallen spray painted a twenty-five-pound rock from his front yard with three coats of white paint, and with red paint, spelled out his account number, the bank’s name, the payee, his leash law citation number, and his signature. Should the US District Court in Seattle—the payee—attempt to cash the rock, would it be good? Explain.Joel Schwarz, “Taking Things for Granite,” Student Lawyer, December 1981.

- Raul Castana purchased a new stereo system from Eddington Electronics Store. He wrote a check on his account at Silver Bank in the amount of $1,200 and gave it to Electronics’ clerk. David Eddington, the store owner, stamped the back of the check with his rubber indorsement stamp, and then wrote, “Pay to the order of City Water,” and he mailed it to City Water to pay the utility bill. Designate the parties to this instrument using the vocabulary discussed in this chapter.

- Would Castana’s signed note made out to Eddington Electronics Store be negotiable if it read, “I promise to pay Eddington’s or order $1,200 on or before May 1, 2012, but only if the stereo I bought from them works to my satisfaction”? Explain. And—disregarding negotiability for a moment—designate the parties to this instrument using the vocabulary discussed in this chapter.

Self-Test Questions

-

A negotiable instrument must

- be signed by the payee

- contain a promise to pay, which may be conditional

- include a sum certain

- be written on paper or electronically

-

The law governing negotiability is found in

- Article 3 of the UCC

- Article 9 of the UCC

- the Uniform Negotiability Act

- state common law

-

A sight draft

- calls for payment on a certain date

- calls for payment when presented

- is not negotiable

- is the same as a certificate of deposit

-

A note reads, “Interest hereon is 2% above the prime rate as determined by First National Bank in New York City.” Under the UCC,

- the interest rate provision is not a “sum certain” so negotiability is destroyed

- the note is not negotiable because the holder must look to some extrinsic source to determine the interest rate

- the note isn’t negotiable because the prime rate can vary before the note comes due

- variable interest rates are OK

-

A “maker” in negotiable instrument law does what?

- writes a check

- becomes obligated to pay on a draft

- is the primary obligor on a note

- buys commercial paper of dubious value for collection

Self-Test Answers

- c

- a

- b

- d

- c