This is “Accountability for Sustainability”, chapter 4 from the book Sustainable Business Cases (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

Chapter 4 Accountability for Sustainability

Overview

Learning Objectives

- Discuss business and organizational accountability.

- List the factors that are influencing an increase in interest and activity in business accountability.

AccountabilityThe obligation that an organization takes on to ensure that it meets its responsibilities. is a concept in corporate governanceThe set of processes, rules, policies, laws, and institutions by which businesses are directed, administered, or controlled. that is the acknowledgement of responsibility by an organization for actions, decisions, products, and policies that it undertakes.

A customer of a business expects that a product manufactured and sold by a business has been designed, tested, and produced so that it is safe to use. An investor in a business expects that the managers of the company are working to maximize shareholder return and to not be wasteful of corporate resources. The federal government expects that a business pays its taxes properly and promptly. These are all examples of the expectations that stakeholdersAny person, group, or organization affected by an organization’s actions. For businesses, it can include owners and investors, employees, customers, suppliers, and all members of society affected by the organization. have of businesses to act in a responsible manner.

Rising stakeholder expectations are motivating organizations to consider the impacts of their actions in a broad, transparent, and systematic manner. Businesses are a major actor in modern society, and stakeholders expect that businesses be a positive contributor to societal well-being. Stakeholders want companies to be more than purveyors of a product or a service; they expect them to fulfill a more positive societal role.

Consumers are showing increasing concern for the environmental and societal impacts of the products and services they purchase.BBMG, Conscious Consumers Are Changing the Rules of Marketing. Are You Ready?, http://www.bbmg.com/pdfs/BBMG_Conscious_Consumer_White_Paper.pdf. Many investors are starting to use a company’s performance in sustainability as an indicator of business value and of management strength. A recent example of increased investor sustainability accountability expectations is when twenty-four institutional investors wrote to thirty of the world’s largest stock exchanges asking that they address inadequate sustainability reportingThe collection, analysis, and reporting of social, economic, and ecological performance indicators by an organization. by companies.United Nations Global Compact, “Investors Representing US$1.6 Trillion Call for Sustainability Disclosure from Listed Companies,” news release, February 2011, http://www.unglobalcompact.org/news/103-02-22-2011.

“Shooting the Elephant”

There are numerous examples of companies’ social or environmental actions affecting consumer purchasing behavior both positively and negatively. In March 2011, Bob Parsons, the CEO of GoDaddy, the world’s largest provider of web hosting and domain name registrations, posted a video of him shooting an elephant in Zimbabwe, Africa, on the Internet. The video showed the elephant being killed and local villagers stripping flesh from the carcass of the dead elephant to a score of rock band AC/DC’s “Hells Bells.” While Parsons claimed the elephant was destroying the villagers’ crops and that he was actually providing a service to the local African community, his actions—and specifically the callous way that he documented his actions—spurred outrage from customers with many cancelling their accounts as a result. This is an example of how the social conduct of the CEO of a company carried over to the brand image of the company and resulted in a loss in revenue.

Video 1

Elephant Hunt Video

Follow the link to view the video:

Sidebar

“Ethical Jewelry”

In June 2011, Jewelers’ Circular Keystone (JCK), the jewelry industry’s leading trade publication, reported on the results of a survey that found 78 percent of consumers said they cared about sustainability and 60 percent of consumers said they were willing to pay a premium for “ethical jewelry.” Rebecca Foerster, the US vice president at Rio Tinto Diamonds, stated, “This generation that is up and coming is more concerned about where the products they are buying come from, and they are becoming activists about it.”Rob Bates, “JCK Las Vegas: Consumers Want Sustainable Products,” JCK Magazine, June 4, 2011, http://www.jckonline.com/2011/06/04/jck-las-vegas-consumers-want-sustainable-products. Consumer demand for ethical jewelry is increasing sales for products, such as recycled gold and conflict-free-certified diamonds.

“Conflict” diamonds, also known as “blood” diamonds, are defined by the United Nations as those that originate from areas controlled by forces opposed to legitimate and internationally recognized governments. Angola and Sierra Leone in Africa are examples of two countries that are sources of conflict diamonds. Diamonds have often been used by rebel forces in these countries to finance arms purchases and other illegal activities. Conflict-free diamonds do not look any different from conflict diamonds but have proof of origination showing that were produced in more peaceful regions of the world.

Ethical jewelry is an example of how consumer concern for sustainable products is transforming the offerings from the jewelry industry. By customers “voting” with their purchases they are supporting conflict-free diamonds, which helps reduce a source of funding available to rebel forces with the expectation that this will either shorten wars or prevent their occurrence.

Blood diamond impact.

Organizations also need to prepare for anticipated regulation and new government measures related to environmental and social impact. Governments continue to pass legislation to change or end business practices that are harmful to the environment, consumers, or employees. Governments also provide programs and incentives to support voluntary efforts by business to improve their impacts on the community and the environment. The role of government in driving sustainability in businesses is discussed in detail in Chapter 3 "Government, Public Policy, and Sustainable Business".

The response by many businesses has been an increase in transparencyRefers to openness, communication, and accountability. For sustainable businesses, it involves ready access to important information about an organization’s economic, ecological, and social impacts. on the reporting of the economic, ecological, and social impacts of their activities. This allows for credibility and operational integrity in a company’s business activities. Businesses need to clearly communicate the positive and measurable impact that they have on all the stakeholders impacted by their operations.

Triple bottom line (TBL) reporting, also known as sustainability reporting, has emerged as the primary vehicle to communicate this information from businesses to stakeholders. This type of reporting goes beyond profit (financial) information and discloses the planet (environmental) and people (social) impact of a business. Sustainability reporting is a tool to communicate to society the actions a company is undertaking to fulfill its broad responsibilities to society.

A goal of sustainability reporting at the society level is to identify uneconomic growth. Uneconomic growthA concept from human welfare economics and is economic growth that results in a decline in the quality of life. is a concept from human welfare economics and is economic growth that results in a decline in the quality of life. Only measuring financial activity would not identify uneconomic growth, but with the inclusion of social and environmental performance, stakeholders have a better indication of the quality of economic activity.

Quite often sustainability reporting is driven not only by external stakeholder forces but by the internal core values of the companies. Some companies are founded by social entrepreneurs who want to incorporate aspects of social change or environmental stewardship into their business operations. Sustainability reporting provides a way of documenting efforts by these organizations and communicating that to customers and other stakeholders. Some companies hope that by publicly disclosing successes and failures related to their sustainability initiatives that they can provide lessons learned to help other companies become more sustainable.

Businesses are facing new risks that need to be managed and this is leading them to actively manage their sustainability profile. Resource depletion, increased toxicity, and climate change are all examples of risks that can decrease profitability through either increased cost or decreased revenue. Sustainability reporting can help a company measure and quantify its economic risk associated with different environmental or social threats that may be overlooked in traditional financial reporting. At the same time, all of these factors provide for new business opportunities, and the companies that can successfully manage their businesses from a sustainability perspective can build competitive advantage, mitigate risk, and capitalize on innovation.

Currently, larger-size companies, such as Ford, are leading efforts in sustainability reporting as they have greater financial resources available to cover the additional costs of sustainability reporting. It can be challenging for smaller companies to replicate the efforts of the largest and most resourceful companies. These larger company efforts in sustainability reporting, which are the focus of this chapter, provide examples of the types of information that could be useful for businesses of all sizes to report on and provide details about processes that business of all sizes can establish in sustainability reporting.

Sidebar

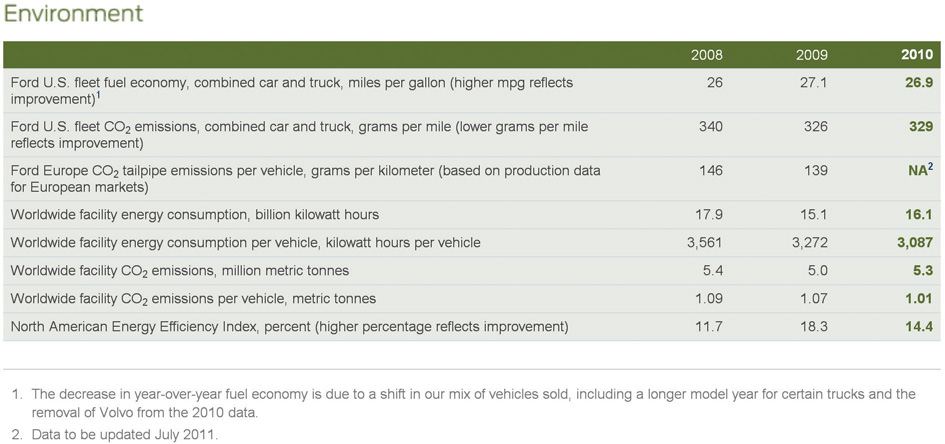

Sustainability Reporting at Ford

Ford’s “12th Annual Sustainability Report” provides a performance summary with measures that are important to Ford in its pursuit of sustainability. Ford chose to publish their report as an interactive website that allowed stakeholders to quickly jump to the areas of sustainability that were of interest to them.

Source: “Sustainability Report 2010–2011,” Ford Company, http://corporate.ford.com/microsites/sustainability-report-2010-11/overview-performance.

Highlights from the Twelfth Annual Sustainability Report

- Reduced CO2 emissions from Ford’s global operations by 5.6 percent on a per-vehicle basis, compared to 2009.

- Set a goal to reduce global facility CO2 emissions by 30 percent by 2025 on a per-vehicle basis.

- Listed water as one of the top sustainability concerns; Ford aims to reduce 2011 global water use by 5 percent per vehicle compared to 2010. This is in addition to the 49 percent per vehicle reduction since 2000.

To read Ford’s complete sustainability report, go to http://corporate.ford.com/microsites/sustainability-report-2010-11/default.

Sidebar

Rocky Mountain Flatbread

Rocky Mountain Flatbread is owned by Dominic and Suzanne Fielden, who “care deeply about…community, food and celebration.” The Canadian-based business operates two carbon neutral restaurants and a pizza wholesale business, which distributes to over two hundred health and grocery stores throughout western Canada. Their company exists to generate a profit but also to create positive societal change. They engage in a wide variety of sustainability activities, including partnering with local schools on healthy cooking classes, using Canadian-grown ingredients, and fueling their clay oven with salvage wood or fallen timber. They have taken a simplified approach to sustainability reporting and have calculated a carbon footprint and keep track of some key metrics. For example, 90 percent of their food ingredients are produced locally, and they compost 100 percent of their food.American Institute of CPAs, SMEs Set their Sights on Sustainability: Case Studies of Small and Medium-Sized Enterprises (SMEs) from the UK, US and Canada, http://www.aicpa.org/interestareas/businessindustryandgovernment/resources/sustainability/downloadabledocuments/sustainability_case_studies_final%20pdf.pdf. They have found the right balance of tracking information to help inform progress on sustainability goals without hindering business operations. Public reporting of their sustainability efforts includes videos on YouTube (http://www.youtube.com/watch?v=8PSIPWavu0o) and sustainabilitytv.com, Facebook, and a page on their website called “Going Green.”

Key Takeaways

- Accountability is the acknowledgement of responsibility by an organization for actions, decisions, products, and policies that it undertakes.

- Stakeholders expect that businesses will act in a responsible manner.

- Sustainability is a business philosophy in which a company considers its accountability for its social and ecological impacts.

- Triple bottom line, also called sustainability reporting, is a mechanism to communicate accountability activities to stakeholders.

- Larger-size companies are leading efforts in sustainability reporting as they have greater financial resources available to cover the costs of sustainability reporting.

Exercise

- Visit Rocky Mountain’s website at http://www.rockymountainflatbread.ca/goinggreen/carbonneutral.html. What activities are they undertaking to be carbon neutral? Do you think the web page is an effective tool to communicate with their customers? What other stakeholders might benefit from this web page?