This is “Shifts in Supply and Demand for Bonds”, section 5.2 from the book Finance, Banking, and Money (v. 1.1). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

5.2 Shifts in Supply and Demand for Bonds

Learning Objective

- What causes the supply and demand for bonds to shift?

Shifting supply and demand curves around can be fun, but figuring out why the curves shift is the interesting part. (Determining the shape and slope of the curves is interesting too, but these details will not detain us here.) Movements along the curve, or why the supply curve slopes upward and the demand curve downward, were easy enough to grasp. Determining why the whole curve moves, why investors are willing to buy more (or fewer) bonds, or why borrowers are willing to sell more (or fewer) bonds at a given price is a bit more involved. Let’s tackle demand first, then we will move on to supply.

Wealth determines the overall demand for assets. An asset (something owned) is any store of value, including financial assets like money, loans (for the lender), bonds, equities (stocks), and a potpourri of derivativeshttp://www.margrabe.com/Dictionary/DictionaryAC.html#sectA and nonfinancial assets like real estate (land, buildings), precious metals (gold, silver, platinum), gems (diamonds, rubies, emeralds), hydrocarbons (oil, natural gas) and (to a greater or lesser extent, depending on their qualities) all other physical goods (as opposed to bads, like pollution, or freebies, like air). As wealth increases, so too does the quantity demanded of all types of assets, though to different degrees. The reasoning here is almost circular: if it is to be maintained, wealth must be invested in some asset, in some store of value. In which type of asset to invest new wealth is the difficult decision. When determining which assets to hold, most economic entities (people, firms, governments) care about many factors, but for most investors most of the time, three variables—expected relative return, risk, and liquidity—are paramount. (We briefly discussed these concepts, you may recall, in Chapter 2 "The Financial System".)

Expected relative return is the ex ante (before the fact) belief that the return on one asset will be higher than the returns of other comparable (in terms of risk and liquidity) assets. Return is a good thing, of course, so as expected relative return increases, the quantity demanded of an asset also increases. That can happen because the expected return on the asset itself increases, because the expected return on comparables decreases, or because of a combination thereof. Clearly, two major factors discussed in Chapter 4 "Interest Rates" will affect return expectations and hence the demand for certain financial assets, like bonds: expected interest rates and, via the Fisher Equation, expected inflation. If the interest rate is expected to increase for any reason (including, but not limited to, expected increases in inflation), bond prices are expected to fall, so the quantity demanded will decrease. Conversely, if the interest rate is thought to decrease for any reason (including, but not limited to, the expected taming of inflation), bond prices are expected to rise, so the quantity demanded will increase.

Overall, though, calculating relative expected returns is sticky business that is best addressed in more specialized financial books and courses. If you want an introduction, investigate the capital asset pricing model (CAPM)http://www.valuebasedmanagement.net/methods_capm.html;http://www.moneychimp.com/articles/valuation/capm.htm and the arbitrage pricing theory (APT).http://moneyterms.co.uk/apt/ As we learned in Chapter 4 "Interest Rates", calculating return is not terribly difficult and neither is comparing returns among a variety of assets. What’s tricky is forecasting future returns and making sure that assets are comparable by controlling for risk, among other things. Risk is the uncertainty of an asset’s returns. It comes in a variety of flavors, all of them unsavory, so as it increases, the quantity demanded of an asset decreases, ceteris paribus. In Chapter 4 "Interest Rates", we encountered two types of risk: default risk (aka credit risk), the chance that a financial contract will not be honored, and interest rate risk, the chance that the interest rate will rise and hence decrease a bond or loan’s price. An offsetting risk is called reinvestment risk, which bites when the interest rate decreases because coupon or other interest payments have to be reinvested at a lower yield to maturity. To be willing to take on more risk, whatever its flavor, rational investors must expect a higher relative return. Investors who require a much higher return for assuming a little bit of risk are called risk-averse. Those who will take on much risk for a little higher return are called risk-loving, risk-seekers, or risk-tolerant. (Investors who take on more risk without compensation are neither risk-averse nor risk-tolerant, but rather irrational in the sense discussed in Chapter 7 "Rational Expectations, Efficient Markets, and the Valuation of Corporate Equities".) Risks can be idiosyncratic; that is, they can be pertinent to a particular company, sectoral (pertinent to an entire industry, like trucking or restaurants), or systemic (economy-wide). Liquidity risk occurs when an asset cannot be sold as quickly or cheaply as expected, be it for idiosyncratic, sectoral, or systemic reasons. This, too, is a serious risk because liquidity, or (to be more precise) liquidity relative to other assets, is the third major determinant of asset demand. Because investors often need to change their investment portfolioThe set of financial and other investments or assets held by an economic entity. or dis-save (spend some of their wealth on consumption), liquidity, the ability to sell an asset quickly and cheaply, is a good thing. The more liquid an asset is, therefore, the higher the quantity demanded, all else being equal.

During the financial crisis that began in 2007, the prices of a certain type of bond collateralized by subprime mortgages, long-term loans collateralized with homes and made to relatively risky borrowers, collapsed. In other words, their yields had to increase markedly to induce investors to own them. They dropped in price after investors realized that the bonds, a type of asset-backed security (ABS), had much higher default rates and much lower levels of liquidity than they had previously believed. Figure 5.4 "Variables that influence demand for bonds" summarizes the chapter discussion so far.

Figure 5.4 Variables that influence demand for bonds

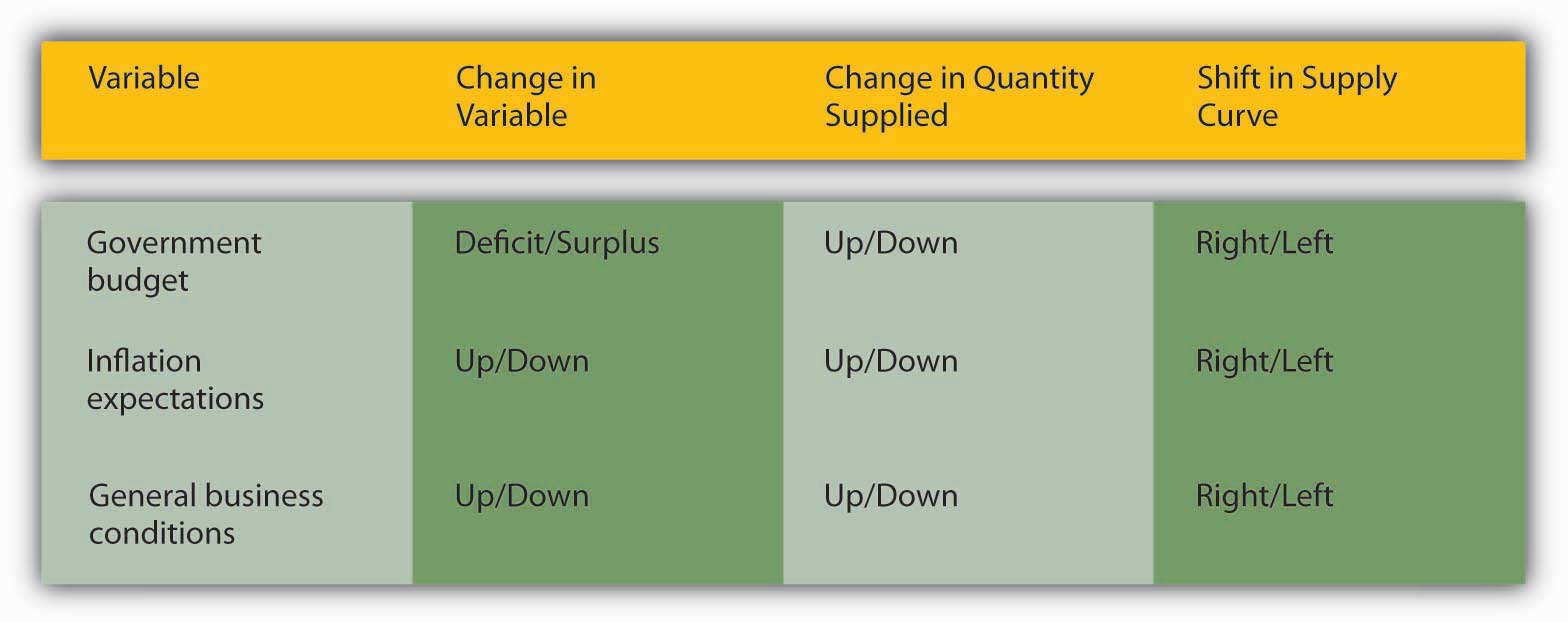

So much for demand. Why does the supply curve for bonds shift to and fro? There are many reasons, but the three main ones are government budgets, inflation expectations, and general business conditions. When governments run budget deficits, they often borrow by selling bonds, pushing the supply curve rightward and bond prices down (yields up), ceteris paribus. When governments run surpluses, and they occasionally do, believe it or not, they redeem and/or buy their bonds back on net, pushing the supply curve to the left and bond prices up (yields down), all else being equal. (For historical time series data on the U.S. national debt, which was usually composed mostly of bonds, browse http://www.economagic.com/em-cgi/data.exe/treas/pubdebt.)

Stop and Think Box

You are a copyeditor for Barron’s. What, if anything, appears wrong in the following sentence? How do you know?

“Recent increases in the profitability of investments, inflation expectations, and government surpluses will surely lead to increased bond supplies in the near future.”

Government deficits, not surpluses, lead to increased bond supplies.

The expectation of higher inflation, other factors held constant, will cause borrowers to issue more bonds, driving the supply curve rightward, and bond prices down (and yields up). The Fisher Equation, ir = i – πe, explains this nicely. If the inflation expectation term πe increases while nominal interest rate i stays the same, the real interest rate ir must decrease. From the perspective of borrowers, the real cost of borrowing falls, which means that borrowing becomes more attractive. So they sell bonds.

Borrowing also becomes more attractive when general business conditions become more favorable, as when taxes and regulatory costs decrease or the economy expands. Although individuals sometimes try to borrow out of financial weakness or desperation, relatively few such loans are made because they are high risk. Most economic entities borrow out of strength, to finance expansion and engage in new projects they believe will be profitable. So when economic prospects are good, taxes are low, and regulations are not too costly, businesses are eager to borrow, often by selling bonds, shifting the supply curve to the right and bond prices down (yields up). Figure 5.5 "Variables that determine the supply of bonds" summarizes the chapter discussion so far.

Figure 5.5 Variables that determine the supply of bonds

As Yoda might say, “Pause here, we must” to make sure we’re on track.http://www.yodaspeak.co.uk/index.php Try out these questions until you are comfortable. Remember that the ceteris paribus condition holds in each.

Exercises

- What will happen to bond prices if stock trading commissions decrease? Why?

- What will happen to bond prices if bond trading commissions increase? Why?

- What will happen to bond prices if the government implements tax increases? Why?

- If government revenues drop significantly (and remember all else stays the same, including government expenditures), what will likely happen to bond prices? Why?

- If the government guaranteed the payment of bonds, what would happen to their prices? Why?

- What will happen to bond prices if the government implements regulatory reforms that reduce regulatory costs for businesses? Why?

- If government revenues increase significantly, what will likely happen to bond prices? Why?

- What will happen to bond prices if terrorism ended and the world’s nations unilaterally disarmed and adopted free trade policies? Why?

- What will happen to bond prices if world peace brought substantially lower government budget deficits?

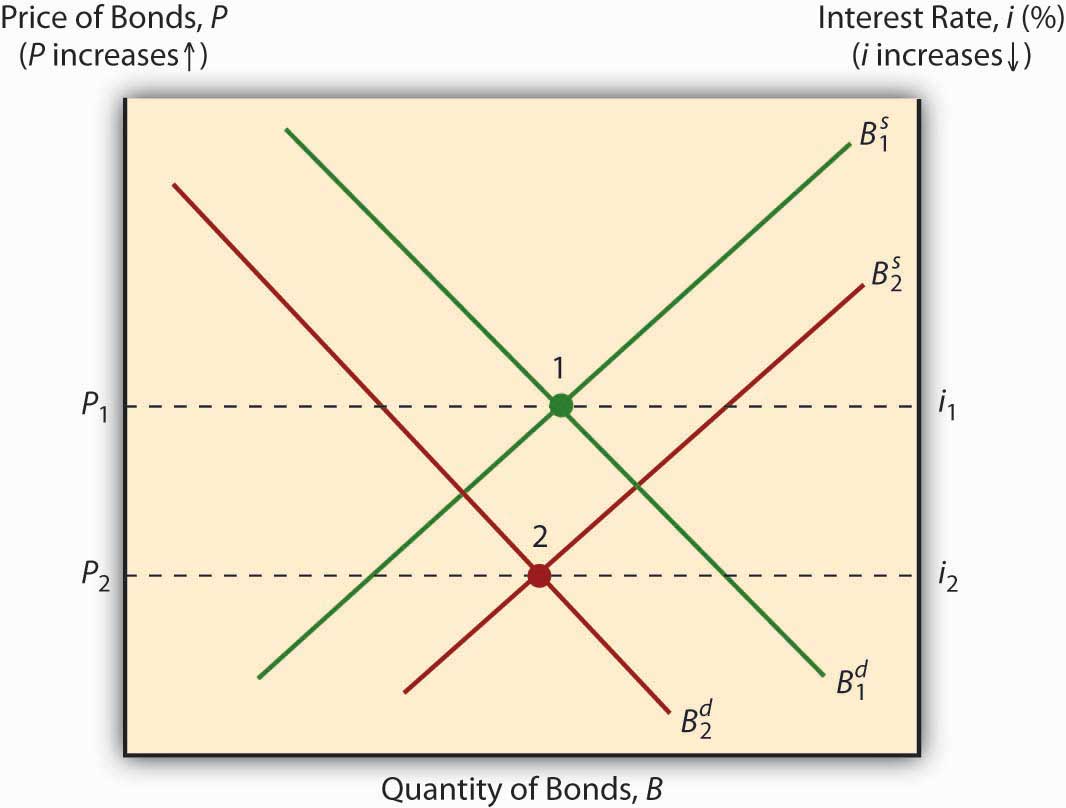

If you’ve already figured out that expected inflation will decrease bond prices, and increase bond yields, by both shifting the supply curve to the right and the demand curve to the left, as in Figure 5.6 "Expected inflation and bond prices" below, kudos to you!

Figure 5.6 Expected inflation and bond prices

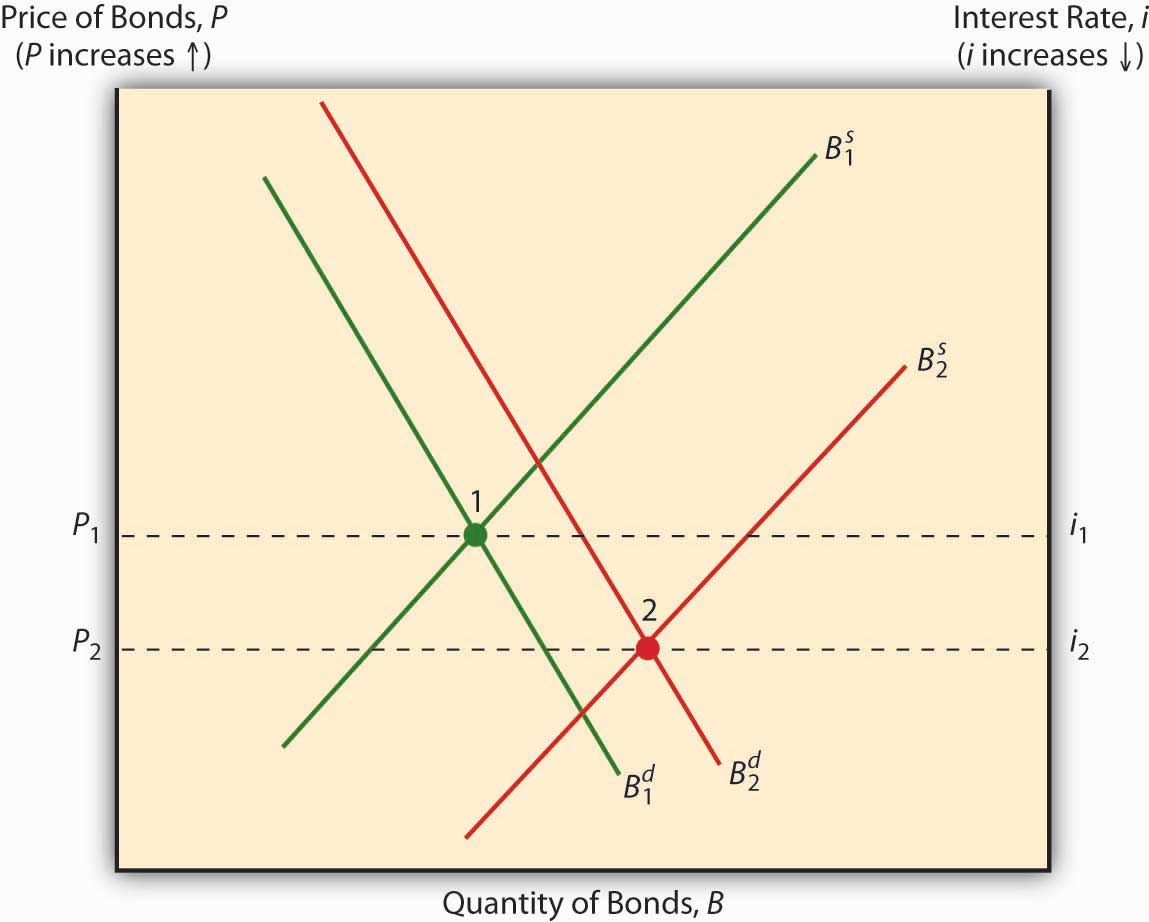

If you noticed that the response of bond prices and yields to a business cycle expansion is indeterminate, booya! As noted above, a boom shifts the bond supply curve to the right by inducing businesses to borrow and thus take advantage of the bonanza. Holding demand constant, that action reduces bond prices (raises the interest rate). But demand does not stay constant because economic expansion increases wealth, which increases demand for bonds (shifts the curve to the right), which in turn increases bond prices (reduces the interest rate). The net effect on the interest rate, therefore, depends on how much each curve shifts, as in Figure 5.7 "Business cycle expansion and bond prices".

Figure 5.7 Business cycle expansion and bond prices

In reality, the first scenario is the one that usually wins out: during expansions, the interest rate usually rises, and during recessions, it always falls. For example, the interest rate fell to very low levels during the Great DepressionAn almost worldwide decrease in per capita income during the 1930s. and during Japan’s extended economic funkFunk is not a technical term, but it is used widely because it encapsulates the economic situation in Japan in a single interesting word. After World War II, Japan experienced rapid economic growth. That growth slowed considerably in the 1990s, following a major financial crisis. in the 1990s.http://www.bloomberg.com/apps/news?pid=10000101&refer=japan&sid=a28sELjm9W04

Key Takeaways

- The demand curve for bonds shifts due to changes in wealth, expected relative returns, risk, and liquidity.

- Wealth, returns, and liquidity are positively related to demand; risk is inversely related to demand.

- Wealth sets the general level of demand. Investors then trade off risk for returns and liquidity.

- The supply curve for bonds shifts due to changes in government budgets, inflation expectations, and general business conditions.

- Deficits cause governments to issue bonds and hence shift the bond supply curve right; surpluses have the opposite effect.

- Expected inflation leads businesses to issue bonds because inflation reduces real borrowing costs, ceteris paribus; decreases in expected inflation or deflation expectations have the opposite effect.

- Expectations of future general business conditions, including tax reductions, regulatory cost reduction, and increased economic growth (economic expansion or boom), induce businesses to borrow (issue bonds), while higher taxes, more costly regulations, and recessions shift the bond supply curve left.

- Theoretically, whether a business expansion leads to higher interest rates or not depends on the degree of the shift in the bond supply and demand curves.

- An expansion will cause the bond supply curve to shift right, which alone will decrease bond prices (increase the interest rate).

- But expansions also cause the demand for bonds to increase (the bond demand curve to shift right), which has the effect of increasing bond prices (and hence lowering bond yields).

- Empirically, the bond supply curve typically shifts much further than the bond demand curve, so the interest rate usually rises during expansions and always falls during recessions.