This is “What Do We Mean by Currency and Foreign Exchange?”, section 7.1 from the book Challenges and Opportunities in International Business (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

7.1 What Do We Mean by Currency and Foreign Exchange?

Learning Objectives

- Understand what is meant by currency and foreign exchange.

- Explore the purpose of the foreign exchange market.

- Understand how to determine exchange rates.

What Are Currency and Foreign Exchange?

In order to understand the global financial environment, how capital markets work, and their impact on global business, we need to first understand how currencies and foreign exchange rates work.

Briefly, currencyAny form of money in general circulation in a country. is any form of money in general circulation in a country. What exactly is a foreign exchange? In essence, foreign exchangeMoney denominated in the currency of another country. Money can also be denominated in the currency of a group of countries, such as the euro. is money denominated in the currency of another country or—now with the euro—a group of countries. Simply put, an exchange rateThe rate at which the market converts one currency into another. is defined as the rate at which the market converts one currency into another.

Any company operating globally must deal in foreign currencies. It has to pay suppliers in other countries with a currency different from its home country’s currency. The home country is where a company is headquartered. The firm is likely to be paid or have profits in a different currency and will want to exchange it for its home currency. Even if a company expects to be paid in its own currency, it must assess the risk that the buyer may not be able to pay the full amount due to currency fluctuations.

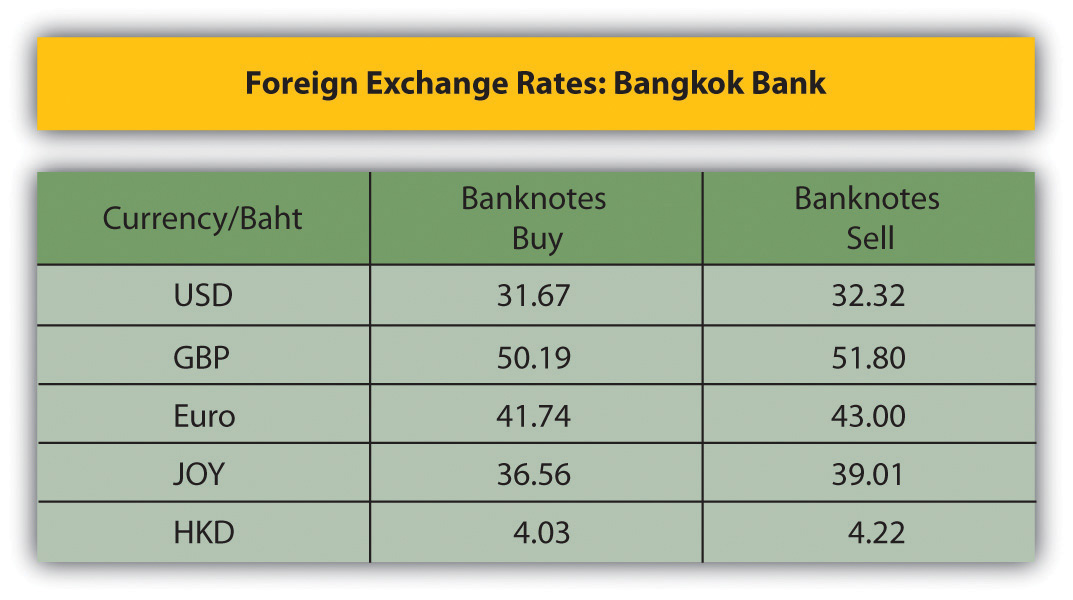

If you have traveled outside of your home country, you may have experienced the currency market—for example, when you tried to determine your hotel bill or tried to determine if an item was cheaper in one country versus another. In fact, when you land at an airport in another country, you’re likely to see boards indicating the foreign exchange rates for major currencies. These rates include two numbers: the bid and the offer. The bid (or buy)The price at which a bank or financial service firm is willing to buy a specific currency. is the price at which a bank or financial services firm is willing to buy a specific currency. The ask (or the offer or sell)Quote that refers to the price at which a bank or financial services firm is willing to sell that currency., refers to the price at which a bank or financial services firm is willing to sell that currency. Typically, the bid or the buy is always cheaper than the sell; banks make a profit on the transaction from that difference. For example, imagine you’re on vacation in Thailand and the exchange rate board indicates that the Bangkok Bank is willing to exchange currencies at the following rates (see the following figure). GBP refers to the British pound; JPY refers to the Japanese yen; and HKD refers to the Hong Kong dollar, as shown in the following figure. Because there are several countries that use the dollar as part or whole of their name, this chapter clearly states “US dollar” or uses US$ or USD when referring to American currency.

This chart tells us that when you land in Thailand, you can use 1 US dollar to buy 31.67 Thai baht. However, when you leave Thailand and decide that you do not need to take all your baht back to the United States, you then convert baht back to US dollars. We then have to use more baht—32.32 according to the preceding figure—to buy 1 US dollar. The spreadThe difference between the bid and the ask. This is the profit made for each unit of currency bought and sold. between these numbers, 0.65 baht, is the profit that the bank makes for each US dollar bought and sold. The bank charges a fee because it performed a service—facilitating the currency exchange. When you walk through the airport, you’ll see more boards for different banks with different buy and sell rates. While the difference may be very small, around 0.1 baht, these numbers add up if you are a global company engaged in large foreign exchange transactions. Accordingly, global firms are likely to shop around for the best rates before they exchange any currencies.

What Is the Purpose of the Foreign Exchange Market?

The foreign exchange market (or FX market) is the mechanism in which currencies can be bought and sold. A key component of this mechanism is pricing or, more specifically, the rate at which a currency is bought or sold. We’ll cover the determination of exchange rates more closely in this section, but first let’s understand the purpose of the FX market. International businesses have four main uses of the foreign exchange markets.

Currency Conversion

Companies, investors, and governments want to be able to convert one currency into another. A company’s primary purposes for wanting or needing to convert currencies is to pay or receive money for goods or services. Imagine you have a business in the United States that imports wines from around the world. You’ll need to pay the French winemakers in euros, your Australian wine suppliers in Australian dollars, and your Chilean vineyards in pesos. Obviously, you are not going to access these currencies physically. Rather, you’ll instruct your bank to pay each of these suppliers in their local currencies. Your bank will convert the currencies for you and debit your account for the US dollar equivalent based on the exact exchange rate at the time of the exchange.

Currency Hedging

One of the biggest challenges in foreign exchange is the risk of rates increasing or decreasing in greater amounts or directions than anticipated. Currency hedgingRefers to the technique of protecting against the potential losses that result from adverse changes in exchange rates. refers to the technique of protecting against the potential losses that result from adverse changes in exchange rates. Companies use hedging as a way to protect themselves if there is a time lag between when they bill and receive payment from a customer. Conversely, a company may owe payment to an overseas vendor and want to protect against changes in the exchange rate that would increase the amount of the payment. For example, a retail store in Japan imports or buys shoes from Italy. The Japanese firm has ninety days to pay the Italian firm. To protect itself, the Japanese firm enters into a contract with its bank to exchange the payment in ninety days at the agreed-on exchange rate. This way, the Japanese firm is clear about the amount to pay and protects itself from a sudden depreciation of the yen. If the yen depreciates, more yen will be required to purchase the same euros, making the deal more expensive. By hedging, the company locks in the rate.

Currency Arbitrage

Arbitrage is the simultaneous and instantaneous purchase and sale of a currency for a profit. Advances in technology have enabled trading systems to capture slight differences in price and execute a transaction, all within seconds. Previously, arbitrage was conducted by a trader sitting in one city, such as New York, monitoring currency prices on the Bloomberg terminal. Noticing that the value of a euro is cheaper in Hong Kong than in New York, the trader could then buy euros in Hong Kong and sell them in New York for a profit. Today, such transactions are almost all handled by sophisticated computer programs. The programs constantly search different exchanges, identify potential differences, and execute transactions, all within seconds.

Currency Speculation

Speculation refers to the practice of buying and selling a currency with the expectation that the value will change and result in a profit. Such changes could happen instantly or over a period of time.

High-risk, speculative investments by nonfinance companies are less common these days than the current news would indicate. While companies can engage in all four uses discussed in this section, many companies have determined over the years that arbitrage and speculation are too risky and not in alignment with their core strategies. In essence, these companies have determined that a loss due to high-risk or speculative investments would be embarrassing and inappropriate for their companies.

Understand How to Determine Exchange Rates

How to Quote a Currency

There are several ways to quote currency, but let’s keep it simple. In general, when we quote currencies, we are indicating how much of one currency it takes to buy another currency. This quote requires two components: the base currencyThe currency that is to be purchased with another currency and is noted in the denominator. and the quoted currencyThe currency with which another currency is to be purchased.. The quoted currency is the currency with which another currency is to be purchased. In an exchange rate quote, the quoted currency is typically the numerator. The base currency is the currency that is to be purchased with another currency, and it is noted in the denominator. For example, if we are quoting the number of Hong Kong dollars required to purchase 1 US dollar, then we note HKD 8 / USD 1. (Note that 8 reflects the general exchange rate average in this example.) In this case, the Hong Kong dollar is the quoted currency and is noted in the numerator. The US dollar is the base currency and is noted in the denominator. We read this quote as “8 Hong Kong dollars are required to purchase 1 US dollar.” If you get confused while reviewing exchanging rates, remember the currency that you want to buy or sell. If you want to sell 1 US dollar, you can buy 8 Hong Kong dollars, using the example in this paragraph.

Direct Currency Quote and Indirect Currency Quote

Additionally, there are two methods—the American termsAlso known as US terms, American terms are from the point of view of someone in the United States. In this approach, foreign exchange rates are expressed in terms of how many US dollars can be exchanged for one unit of another currency (the non-US currency is the base currency). and the European termsForeign exchange rates are expressed in terms of how many currency units can be exchanged for one US dollar (the US dollar is the base currency). For example, the pound-dollar quote in European terms is £0.64/US$1 (£/US$1).—for noting the base and quoted currency. These two methods, which are also known as direct and indirect quotes, are opposite based on each reference point. Let’s understand what this means exactly.

The American terms, also known as US terms, are from the point of view of someone in the United States. In this approach, foreign exchange rates are expressed in terms of how many US dollars can be exchanged for one unit of another currency (the non-US currency is the base currency). For example, a dollar-pound quote in American terms is USD/GP (US$/£) equals 1.56. This is read as “1.56 US dollars are required to buy 1 pound sterling.” This is also called a direct quoteStates the domestic currency price of one unit of foreign currency. For example, €0.78/US$1. We read this as “it takes 0.78 of a euro to buy 1 US dollar.” In a direct quote, the domestic currency is a variable amount and the foreign currency is fixed at one unit., which states the domestic currency price of one unit of foreign currency. If you think about this logically, a business that needs to buy a foreign currency needs to know how many US dollars must be sold in order to buy one unit of the foreign currency. In a direct quote, the domestic currency is a variable amount and the foreign currency is fixed at one unit.

Conversely, the European terms are the other approach for quoting rates. In this approach, foreign exchange rates are expressed in terms of how many currency units can be exchanged for a US dollar (the US dollar is the base currency). For example, the pound-dollar quote in European terms is £0.64/US$1 (£/US$1). While this is a direct quote for someone in Europe, it is an indirect quoteStates the price of the domestic currency in foreign currency terms. For example, US$1.28/€1. We read this as “it takes 1.28 US dollars to buy 1 euro.” In an indirect quote, the foreign currency is a variable amount and the domestic currency is fixed at one unit. in the United States. An indirect quote states the price of the domestic currency in foreign currency terms. In an indirect quote, the foreign currency is a variable amount and the domestic currency is fixed at one unit.

A direct and an indirect quote are simply reverse quotes of each other. If you have either one, you can easily calculate the other using this simple formula:

direct quote = 1 / indirect quote.To illustrate, let’s use our dollar-pound example. The direct quote is US$1.56 = 1/£0.64 (the indirect quote). This can be read as

1 divided by 0.64 equals 1.56.In this example, the direct currency quote is written as US$/£ = 1.56.

While you are performing the calculations, it is important to keep track of which currency is in the numerator and which is in the denominator, or you might end up stating the quote backward. The direct quote is the rate at which you buy a currency. In this example, you need US$1.56 to buy a British pound.

Tip: Many international business professionals become experienced over their careers and are able to correct themselves in the event of a mix-up between currencies. To illustrate using the example mentioned previously, the seasoned global professional knows that the British pound is historically higher in value than the US dollar. This means that it takes more US dollars to buy a pound than the other way around. When we say “higher in value,” we mean that the value of the British pound buys you more US dollars. Using this logic, we can then deduce that 1.56 US dollars are required to buy 1 British pound. As an international businessperson, we would know instinctively that it cannot be less—that is, only 0.64 US dollars to buy a British pound. This would imply that the dollar value was higher in value. While major currencies have changed significantly in value vis-à-vis each other, it tends to happen over long periods of time. As a result, this self-test is a good way to use logic to keep track of tricky exchange rates. It works best with major currencies that do not fluctuate greatly vis-à-vis others.

A useful side note: traders always list the base currency as the first currency in a currency pair. Let’s assume, for example, that it takes 85 Japanese yen to purchase 1 US dollar. A currency trader would note this as follows: USD 1 / JPY 85. This quote indicates that the base currency is the US dollar and 85 yen are required to purchase a dollar. This is also called a direct quote, although FX traders are more likely to call it an American rate rather than a direct rate. It can be confusing, but try to keep the logic of which currency you are selling and which you are buying clearly in your mind, and say the quote as full sentences in order to keep track of the currencies.

These days, you can easily use the Internet to access up-to-date quotes on all currencies, although the most reliable sites remain the Wall Street Journal, the Financial Times, or any website of a trustworthy financial institution.

Spot Rates

The exchange rates discussed in this chapter are spot rates—exchange rates that require immediate settlement with delivery of the traded currency. “Immediate” usually means within two business days, but it implies an “on the spot” exchange of the currencies, hence the term spot rate. The spot exchange rateThe exchange rate transacted at a particular moment by a buyer and seller of a currency. When we buy and sell our foreign currency at a bank or at American Express, it’s quoted as the rate for the day. For currency traders, the spot can change throughout the trading day, even by tiny fractions. is the exchange rate transacted at a particular moment by the buyer and seller of a currency. When we buy and sell our foreign currency at a bank or at American Express, it’s quoted at the rate for the day. For currency traders though, the spot can change throughout the trading day even by tiny fractions.

To illustrate, assume that you work for a clothing company in the United States and you want to buy shirts from either Malaysia or Indonesia. The shirts are exactly the same; only the price is different. (For now, ignore shipping and any taxes.) Assume that you are using the spot rate and are making an immediate payment. There is no risk of the currency increasing or decreasing in value. (We’ll cover forward rates in the next section.)

The currency in Malaysia is the Malaysian ringgit, which is abbreviated MYR. The supplier in Kuala Lumpur e-mails you the quote—you can buy each shirt for MYR 35. Let’s use a spot exchange rate of MYR 3.13 / USD 1.

The Indonesian currency is the rupiah, which is abbreviated as Rp. The supplier in Jakarta e-mails you a quote indicating that you can buy each shirt for Rp 70,000. Use a spot exchange rate of Rp 8,960 / USD 1.

It would be easy to instinctively assume that the Indonesian firm is more expensive, but look more closely. You can calculate the price of one shirt into US dollars so that a comparison can be made:

For Malaysia: MYR 35 / MYR 3.13 = USD 11.18 For Indonesia: Rp 70,000 / Rp 8,960 = USD 7.81Indonesia is the cheaper supplier for our shirts on the basis of the spot exchange rate.

Cross Rates

There’s one more term that applies to the spot market—the cross rateThe exchange rate between two currencies, neither of which is the official currency in the country in which the quote is provided. This is the exchange rate between two currencies, neither of which is the official currency in the country in which the quote is provided. For example, if an exchange rate between the euro and the yen were quoted by an American bank on US soil, the rate would be a cross rate.

The most common cross-currency pairs are EUR/GBP, EUR/CHF, and EUR/JPY. These currency pairs expand the trading possibilities in the foreign exchange market but are less actively traded than pairs that include the US dollar, which are called the “majors” because of their high degree of liquidity. The majors are EUR/USD, GBP/ USD, USD/JPY, USD/CAD (Canadian dollar), USD/CHF (Swiss franc), and USD/AUD (Australian dollar). Despite the changes in the international monetary system and the expansion of the capital markets, the currency market is really a market of dollars and nondollars. The dollar is still the reserve currency for the world’s central banks. Table 7.1 "Currency Cross Rates" contains some currency cross rates between the major currencies. We can see, for example, that the rate for the cross-currency pair of EUR/GBP is 1.1956. This is read as “it takes 1.1956 euros to buy one British pound.” Another example is the EUR/JPY rate, which is 0.00901. However, a seasoned trader would not say that it takes 0.00901 euros to buy 1 Japanese yen. He or she would instinctively know to quote the currency pair as the JPY/EUR rate or—more specifically—that it takes 111.088 yen to purchase 1 euro.

Table 7.1 Currency Cross Rates

| Currency codes / names | United Kingdom Pound | Canadian Dollar | Euro | Hong Kong Dollar | Japanese Yen | Swiss Franc | US Dollar | Chinese Yuan Renminbi |

|---|---|---|---|---|---|---|---|---|

| GBP | 1 | 0.6177 | 0.8374 | 0.08145 | 0.007544 | 0.6455 | 0.633 | 0.09512 |

| CAD | 1.597 | 1 | 1.3358 | 0.1299 | 0.012032 | 1.0296 | 1.0095 | 0.1517 |

| EUR | 1.1956 | 0.7499 | 1 | 0.09748 | 0.00901 | 0.771 | 0.7563 | 0.1136 |

| HKD | 12.2896 | 7.7092 | 10.2622 | 1 | 0.09267 | 7.9294 | 7.7749 | 1.1682 |

| JPY | 132.754 | 83.2905 | 111.088 | 10.8083 | 1 | 85.65 | 84.001 | 12.6213 |

| CHF | 1.5512 | 0.9732 | 1.2981 | 0.1263 | 0.011696 | 1 | 0.9815 | 0.1475 |

| USD | 1.5807 | 0.9915 | 1.3232 | 0.1287 | 0.011919 | 1.0199 | 1 | 0.1503 |

| CNY | 10.5218 | 6.6002 | 8.8075 | 0.8565 | 0.07934 | 6.7887 | 6.6565 | 1 |

| Note: The official name for the Chinese currency is renminbi and the main unit of the currency is the yuan. | ||||||||

| Source: “Currency Cross Rates: Results,” Oanda, accessed May 25, 2011, http://www.oanda.com/currency/cross- rate/result?quotes=GBP"es=CAD"es=EUR"es=HKD"es=JPY"es= CHF"es=USD"es=CNY&go=Get+my+Table+++. | ||||||||

Forward Rates

The forward exchange rateThe rate at which two parties agree to exchange currency and execute a deal at some specific point in the future, usually 30 days, 60 days, 90 days, or 180 days in the future. is the exchange rate at which a buyer and a seller agree to transact a currency at some date in the future. Forward rates are really a reflection of the market’s expectation of the future spot rate for a currency. The forward marketThe currency market for transactions at forward rates. is the currency market for transactions at forward rates. In the forward markets, foreign exchange is always quoted against the US dollar. This means that pricing is done in terms of how many US dollars are needed to buy one unit of the other currency. Not all currencies are traded in the forward market, as it depends on the demand in the international financial markets. The majors are routinely traded in the forward market.

For example, if a US company opted to buy cell phones from China with payment due in ninety days, it would be able to access the forward market to enter into a forward contract to lock in a future price for its payment. This would enable the US firm to protect itself against a depreciation of the US dollar, which would require more dollars to buy one Chinese yuan. A forward contractA contract that requires the exchange of an agreed-on amount of a currency on an agreed-on date and a specific exchange rate. is a contract that requires the exchange of an agreed-on amount of a currency on an agreed-on date and a specific exchange rate. Most forward contracts have fixed dates at 30, 90, or 180 days. Custom forward contracts can be purchased from most financial firms. Forward contracts, currency swaps, options, and futures all belong to a group of financial instruments called derivatives. In the term’s broadest definition, derivativesFinancial instruments whose underlying value comes from (derives from) other financial instruments or commodities. are financial instruments whose underlying value comes from (derives from) other financial instruments or commodities—in this case, another currency.

Swaps, Options, and Futures

Swaps, options, and futures are three additional currency instruments used in the forward market.

A currency swapA simultaneous buy and sell of a currency for two different dates. is a simultaneous buy and sell of a currency for two different dates. For example, an American computer firm buys (imports) components from China. The firm needs to pay its supplier in renminbi today. At the same time, the American computer is expecting to receive RMB in ninety days for its netbooks sold in China. The American firm enters into two transactions. First, it exchanges US dollars and buys yuan renminbi today so that it can pay its supplier. Second, it simultaneously enters into a forward contract to sell yuan and buy dollars at the ninety-day forward rate. By entering into both transactions, the firm is able to reduce its foreign exchange rate risk by locking into the price for both.

Currency optionsThe option or the right, but not the obligation, to exchange a specific amount of currency on a specific future date and at a specific agreed-on rate. Because a currency option is a right but not a requirement, the parties in an option do not have to actually exchange the currencies if they choose not to. are the option or the right—but not the obligation—to exchange a specific amount of currency on a specific future date and at a specific agreed-on rate. Since a currency option is a right but not a requirement, the parties in an option do not have to actually exchange the currencies if they choose not to. This is referred to as not exercising an option.

Currency futures contractsContracts that require the exchange of a specific amount of currency at a specific future date and at a specific exchange rate. are contracts that require the exchange of a specific amount of currency at a specific future date and at a specific exchange rate. Futures contracts are similar to but not identical to forward contracts.

Exchange-Traded and Standardized Terms

Futures contracts are actively traded on exchanges, and the terms are standardized. As a result, futures contracts have clearinghouses that guarantee the transactions, substantially reducing any risk of default by either party. Forward contracts are private contracts between two parties and are not standardized. As a result, the parties have a higher risk of defaulting on a contract.

Settlement and Delivery

The settlement of a forward contract occurs at the end of the contract. Futures contracts are marked-to-market daily, which means that daily changes are settled day by day until the end of the contract. Furthermore, the settlement of a futures contract can occur over a range of dates. Forward contracts, on the other hand, only have one settlement date at the end of the contract.

Maturity

Futures contracts are frequently employed by speculators, who bet on the direction in which a currency’s price will move; as a result, futures contracts are usually closed out prior to maturity and delivery usually never happens. On the other hand, forward contracts are mostly used by companies, institutions, or hedgers that want to eliminate the volatility of a currency’s price in the future, and delivery of the currency will usually take place.

Companies routinely use these tools to manage their exposure to currency risk. One of the complicating factors for companies occurs when they operate in countries that limit or control the convertibility of currency. Some countries limit the profits (currency) a company can take out of a country. As a result, many companies resort to countertrade, where companies trade goods and services for other goods and services and actual monies are less involved.

The challenge for companies is to operate in a world system that is not efficient. Currency markets are influenced not only by market factors, inflation, interest rates, and market psychology but also—more importantly—by government policy and intervention. Many companies move their production and operations to overseas locations to manage against unforeseen currency risks and to circumvent trade barriers. It’s important for companies to actively monitor the markets in which they operate around the world.

Key Takeaways

In this section you learned about the following:

- An exchange rate is the rate at which the market converts one currency into another. An exchange rate can be quoted as direct or indirect.

- The spot rate is an exchange rate that requires immediate settlement with delivery of the traded currency. The forward exchange rate is the exchange rate at which a buyer and seller agree to transact a currency at some date in the future. Swaps, options, and futures are additional types of currency instruments used in the forward market.

- Companies routinely use these tools to manage their exposure to currency risk. Well-functioning currency markets are a component of the global financial markets and an essential mechanism for global firms that need to exchange currencies.

Exercises

(AACSB: Reflective Thinking, Analytical Skills)

- What is currency and foreign exchange? Why are they so important to international business?

- What is the difference between American and European terms for quoting currencies? Give an example. If you have traveled outside your home country, discuss how you exchanged currency while abroad. What process did you follow?

- Describe a spot rate and a forward rate.

- What are the main differences between a forward contract and a futures contract?