This is “Appendix: Transfer Prices between Divisions”, section 11.8 from the book Accounting for Managers (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

11.8 Appendix: Transfer Prices between Divisions

Learning Objective

- Explain how transfer pricing can affect performance evaluation measures.

Question: Many companies have independent divisions that transfer goods or services from one division to another. If division managers are evaluated based only on division results using measures, such as segmented net income, profit margin ratio, or return on investment (ROI), conflicts can arise causing managers to take a course of action that benefits the division but hurts the company as a whole. For example, a division manager may decide to purchase raw materials from an outside supplier even though the same materials can be produced at a lower cost by another division within the company (the other division’s manager refuses to sell the materials at a reduced price because she is evaluated based on her division’s profits!). How should a company establish transfer pricing to avoid this kind of conflict?

Answer: The price used to value the transfer of goods or services between divisions within the same company is called a transfer priceThe value assigned to the transfer of goods or services between divisions within the same company.. Several different approaches can be used to establish transfer prices between divisions. The goal is to establish a transfer pricing policy that encourages managers to do what is in the best interest of the company while also doing what is in the best interest of the division manager (this is called goal congruence). Several common approaches are presented next.

Using the General Economic Transfer Pricing Rule

Question: How does the general economic transfer pricing rule help organizations to establish an appropriate transfer price?

Answer: The general economic transfer pricing rule attempts to establish guidelines for divisions to maximize overall company profit. This rule states the transfer price should be set at differential cost to the selling division (normally variable cost), plus the opportunity cost of making the sale internally (none if the seller has idle capacity or selling price minus differential cost if the seller is at capacity). This rule is summarized in “Key Equation: Economic Transfer Pricing Rule.”

Key Equation

Economic Transfer Pricing Rule

Let’s look at an example illustrating how to establish a reasonable transfer price using the economic transfer pricing rule. Umbrellas, Inc., has two divisions—Assembly and Marketing. In the past, all transfers of umbrellas from Assembly to Marketing were valued at the variable cost of $6 each. However, the Assembly division manager would like to raise the price to $9 per unit.

Which transfer price should be used to maximize company profit, $6 or $9? The answer depends on whether the selling division (Assembly) is below capacity or at capacity.

Transfer Pricing When Selling Division Is below Capacity

Question: Assume Assembly is below capacity. This means there is no opportunity cost of selling internally since no outside sales are forgone as a result of the transaction. What is the appropriate transfer price in this scenario?

Answer: Given this set of circumstances, the Assembly division should set the transfer price at its variable cost of $6 per unit as shown in “Key Equation: Transfer Pricing When below Capacity (Umbrellas, Inc.).” This ensures Marketing does not purchase the umbrellas from another supplier at an amount greater than Umbrella, Inc.’s variable cost.

Key Equation

Transfer Pricing When below Capacity (Umbrellas, Inc.)

*This is the variable cost for Assembly to produce each umbrella.

**Opportunity cost is zero since no outside sales are forgone as a result of making this internal sale.

If Assembly sets the transfer price higher than $6 per unit ($9 for example), thereby violating the economic transfer pricing rule, the risk is that Marketing might find another company willing to provide the umbrellas for an amount less than $9 and higher than $6. If Marketing chooses to buy umbrellas from an outside supplier for $7, for example, profit declines at Umbrella, Inc., because the company paid $1 more than necessary for each umbrella ($1 = $7 outside supplier price − $6 Umbrella, Inc.’s variable cost). Although Marketing looks better as an investment center buying from the outside for $7 because the cost is $2 less than the internal transfer price, the overall company is worse off because the $7 cost is $1 higher than if the umbrellas were produced internally.

Transfer Pricing When Selling Division Is at Capacity

Question: Now assume Assembly is at capacity. This creates an opportunity cost of selling internally, since outside sales must be forgone as a result of the transaction. What is the appropriate transfer price in this scenario?

Answer: Given this new set of circumstances for Umbrellas, Inc., the Assembly division should set the transfer price at its variable cost of $6 per unit plus the opportunity cost of selling internally. Assume the Assembly division sells the umbrellas to outside customers for $10 each. The opportunity cost of selling internally is $4 (= $10 market price − $6 variable cost). Thus the transfer price that maximizes company profit is $10 as shown in “Key Equation: Transfer Pricing When at Capacity (Umbrellas, Inc.).” Assembly is indifferent whether it sells internally for $10 or to outside customers for $10.

Key Equation

Transfer Pricing When at Capacity (Umbrellas, Inc.)

*This is the variable cost for Assembly to produce each umbrella.

**Opportunity cost is the revenue forgone of $4 by selling internally. Revenue forgone of $4 = $10 market price – $6 variable cost.

The economic transfer pricing rule works well when outside market prices are available (see Note 11.50 "Business in Action 11.5"). However, not all goods or services transferred from one division to another have a readily available outside market price. Thus other methods of establishing transfer pricing must be considered.

Business in Action 11.5

Transfer Pricing at General Electric

A review of the notes to General Electric’s annual report reveals the amount of “intersegment revenues” recorded for each of the company’s six segments. This is referring to revenue derived from transferring goods and services between divisions. The note also states that “sales from one component (segment) to another generally are priced at equivalent commercial selling prices.” It appears from this note that General Electric uses market price to establish transfer prices.

Source: General Electric, “2006 Annual Report,” http://www.ge.com.

Using Cost to Set Transfer Price

Question: Another approach to establishing a transfer price is to use the cost of the goods or services being transferred. How are these costs determined?

Answer: Transfer prices can be based on variable cost, full absorption cost, or cost-plus. Each approach is described next.

Variable Cost

Some companies simply use the selling division’s variable cost as the transfer price. However, the weakness in this approach is the selling division will not be able to mark up its products or services, and as a result, will not be able to generate a profit. This is not a problem for selling divisions treated as cost centers, but profit center and investment center managers will not be satisfied with such an approach.

Full Absorption Cost

Companies sometimes set the transfer price at the selling division’s full absorption cost. The selling division manager prefers to cover all costs rather than only variable costs, and using full-absorption cost accomplishes this goal. However, the company’s concern is the buying division might choose to purchase from an outside provider at a higher price than the differential cost plus opportunity cost but lower than the selling division’s full absorption cost. The result is a decision that does not maximize company profit.

Cost-Plus

Companies often add a markup to the selling division’s variable cost or full absorption cost to set the transfer price. This enables the selling division to earn a profit on internal transfers. Again, the risk is that the buying division might buy from an outside supplier at a higher price than differential cost plus opportunity cost, resulting in lower company profit.

Negotiating Transfer Prices

Question: If the general economic transfer pricing rule is not used, and the cost approach is not used, another alternative is to simply negotiate the transfer price. What are the potential weaknesses in negotiating a transfer price?

Answer: Investment center division managers are often expected to act independent of each other. In fact, many companies treat investment centers as separate businesses. To promote the autonomy of each division manager, companies often require the buying and selling divisions to negotiate a transfer price. This sounds reasonable in concept, but the same weakness exists here as with using costs to set a transfer price. The buying division may choose to purchase the goods or services from an outside supplier if negotiations break down, which may lead to a suboptimal decision for the company as a whole.

An additional weakness is the time required to negotiate a transfer price. Managers can spend significant amounts of time in negotiations when the time might be better spent more productively elsewhere in the division.

Choosing the Best Approach to Establish a Transfer Price

Question: Which transfer pricing approach is best?

Answer: There is no one “best” approach to establishing transfer prices. No two companies are identical, and the choice of a transfer pricing policy depends largely on the nature of the company. The most common approaches used in industry are presented in this appendix. The goal is to establish a transfer pricing policy that encourages managers to do what is in the best interest of the company while also serving the best interest of the division manager.

Key Takeaway

- The price used to value the transfer of goods or services between divisions within the same company is called a transfer price. Although there are different approaches for establishing a transfer price, the general economic transfer pricing rule states the transfer price should be set at differential cost to the selling division (normally variable cost) plus the opportunity cost of making the sale internally (none if the seller has idle capacity or selling price minus variable cost if the seller is at capacity). The goal is to establish a transfer pricing policy that encourages managers to do what is in the best interest of the company while also doing what is in the best interest of the division manager.

Review Problem 11.8

Maine Products, LLP, has two divisions—Chocolate and Mint. The Chocolate division typically sells its chocolate to the Mint division for $3 per pound, which covers variable costs. The Chocolate division sells to outside customers for $5 per pound. Use the general economic transfer pricing rule to address the following requirements:

- Calculate the optimal transfer price assuming the Chocolate division is below capacity.

- Calculate the optimal transfer price assuming the Chocolate division is at capacity.

Solution to Review Problem 11.8

-

Because the Chocolate division is below capacity, no outside customer sales are forgone as a result of selling internally. Thus the opportunity cost of selling internally is zero. The optimal transfer price is $3, calculated as follows:

*This is the variable cost per pound.

**Opportunity cost is zero since no outside sales are forgone as a result of selling internally.

-

Since the Chocolate division is at capacity, outside customer sales are forgone as a result of selling internally. Thus there is an opportunity cost of selling internally. The optimal transfer price is $5, calculated as follows:

*This is the variable cost per pound.

**Opportunity cost is the revenue forgone of $2 by selling internally (= $5 market price − $3 variable cost).

End-of-Chapter Exercises

Questions

- What is meant by the term decentralized organization?

- What are the advantages and disadvantages of decentralizing operations?

- Refer to Note 11.3 "Business in Action 11.1" Why would a growing college, such as Sierra College, decentralize operations?

- Refer to Note 11.4 "Business in Action 11.2" How did decentralization at Arthur Andersen contribute to the company’s downfall?

- Describe the three types of responsibility centers presented in the chapter.

- Describe at least three measures used to evaluate performance of investment center division managers.

- What are the two weaknesses of using segmented net income to evaluate managers of investment centers? What performance measures would you use to overcome these weaknesses?

- What is the primary advantage of using ROI rather than segmented net income or profit margin ratio to evaluate investment center managers?

- Describe operating profit margin and asset turnover, and explain how each of these ratios can be used to help division managers improve ROI.

- Describe the potential conflict that can occur between division manager goals and overall company goals when evaluating divisions using ROI.

- Refer to Note 11.25 "Business in Action 11.4" How did General Electric modify net income to evaluate each segment?

- Describe residual income (RI), and explain how RI can resolve the conflict between division manager goals and company goals often created by using ROI.

- Explain the difference between RI and economic value added.

- Refer to the Game Products, Inc., performance measures presented in Figure 11.11 "Five Performance Measures at Game Products, Inc.". Identify which measures you would recommend to the CEO of Game Products, and explain the reasoning behind your recommendation.

- Appendix. Describe the general economic transfer pricing rule.

Brief Exercises

- Evaluating Division Managers at Game Products, Inc. Refer to the dialogue at Game Products, Inc., presented at the beginning of the chapter. Why does the president want to give Carla Klesko, the Board Games division manager, a bonus? Does the CFO agree that Carla deserves a larger bonus than the other division managers? What performance measures would the CFO like to consider before awarding Carla a larger bonus?

-

Decentralizing Operations. Burton Electronics produces radios, computers, and navigation systems. Although all high level decisions are made at company headquarters by top management, rapid expansion and increasingly specialized products have caused the company to consider decentralizing into three divisions. Each division manager would be responsible for costs, revenues, and investments in assets.

Required:

- How should the company classify each division, as a cost center, profit center, or investment center? Explain.

- What are the potential advantages of decentralizing?

- What are the potential disadvantages of decentralizing?

-

Responsibility Centers. Aviation Products, Inc., operates primarily in the United States and has several segments:

- Accounting and finance: responsible for recording financial information and preparing financial reports.

- Human resources: responsible for hiring employees and maintaining personnel records.

- Retail stores: responsible for sales prices and all costs within each store.

- Advertising: responsible for promotional materials.

- Production: responsible for manufacturing company products.

- International operations: acts as an independent segment responsible for all facets of the business outside of the United States.

Required:

For each of the preceding segments, identify whether it is a cost center, profit center, or investment center. Explain your answer.

-

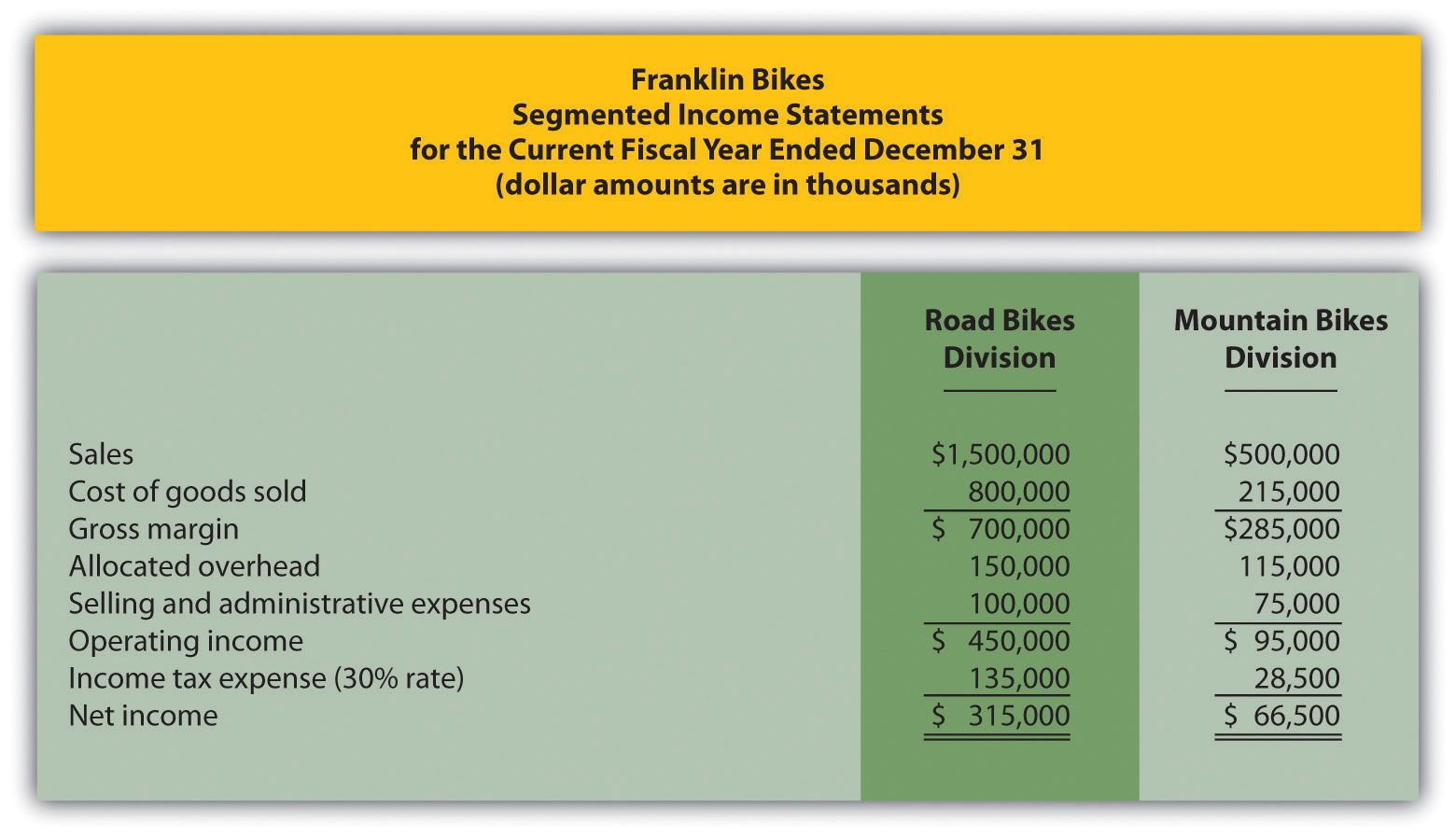

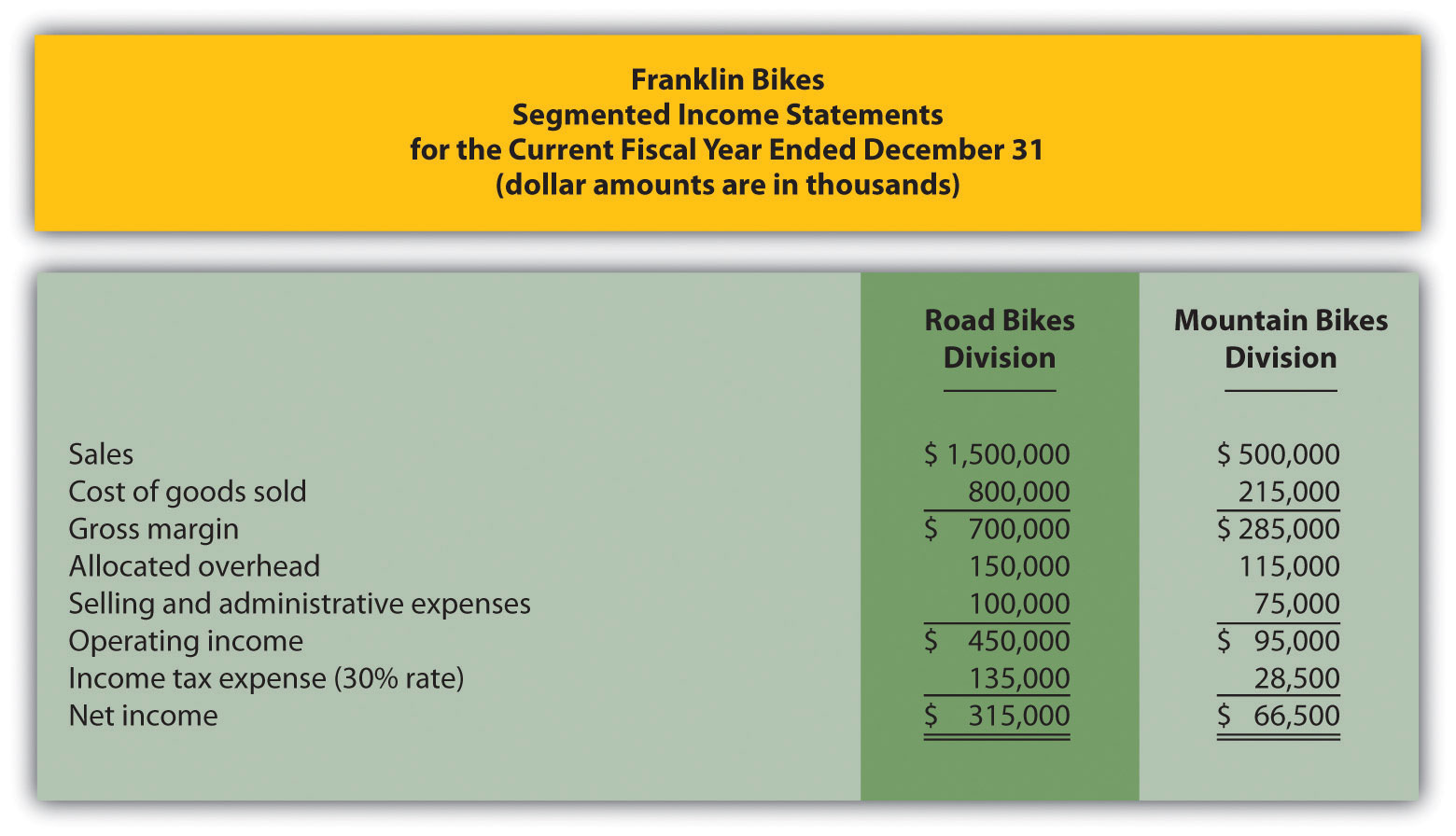

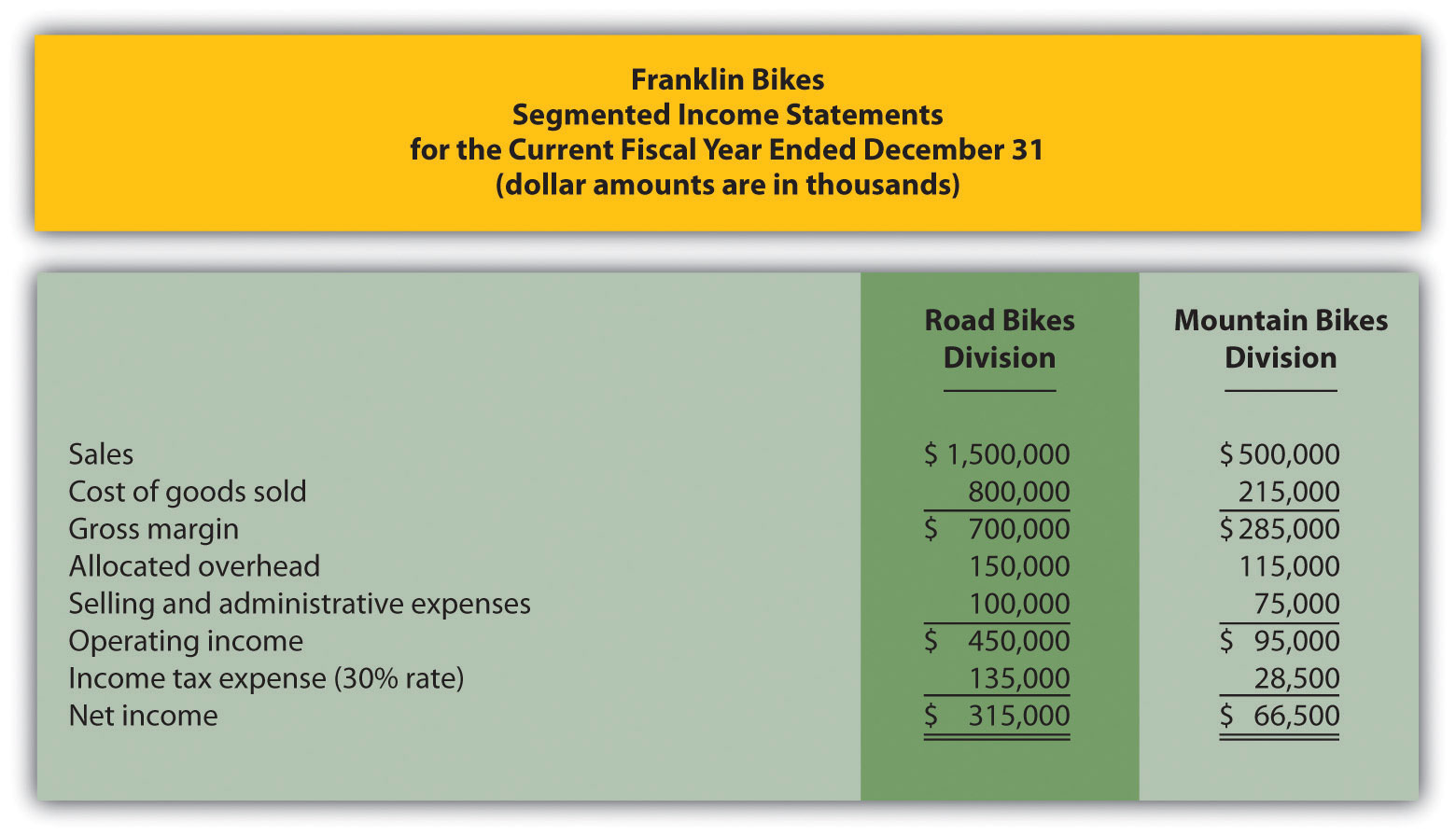

Segmented Net Income. Franklin Bikes has two divisions—Road Bikes and Mountain Bikes. Using the segmented income statements presented in the following, determine the profit margin ratio for each division.

-

Return on Investment (ROI). The segmented income statements presented as follows are for the two divisions of Franklin Bikes. (This is the same company as the previous exercise. This exercise can be assigned independently.) Assume the Road Bikes division had average operating assets totaling $4,500,000 for the year, and the Mountain Bikes division had average operating assets of $800,000. Calculate ROI for each division.

-

Residual Income (RI). The segmented income statements presented as follows are for the two divisions of Franklin Bikes. (This is the same company as the previous exercises. This exercise can be assigned independently.) Assume the Road Bikes division had average operating assets totaling $4,500,000 for the year, and the Mountain Bikes division had average operating assets of $800,000. The company’s cost of capital rate is 8 percent. Calculate RI for each division.

-

Economic Value Added (EVA). Computer Tech Company has two divisions—Hardware and Software. Adjustments have already been made to net operating profit after taxes (NOPAT) and average operating assets for the purposes of calculating EVA for each division. This adjusted information is shown as follows. Assume the company’s cost of capital is 12 percent. Calculate EVA for each division.

Hardware Division Software Division NOPAT—adjusted $ 810,000 $ 980,000 Average operating assets—adjusted 3,500,000 3,200,000 - (Appendix). What is the primary goal for an organization establishing a transfer pricing policy?

Exercises: Set A

-

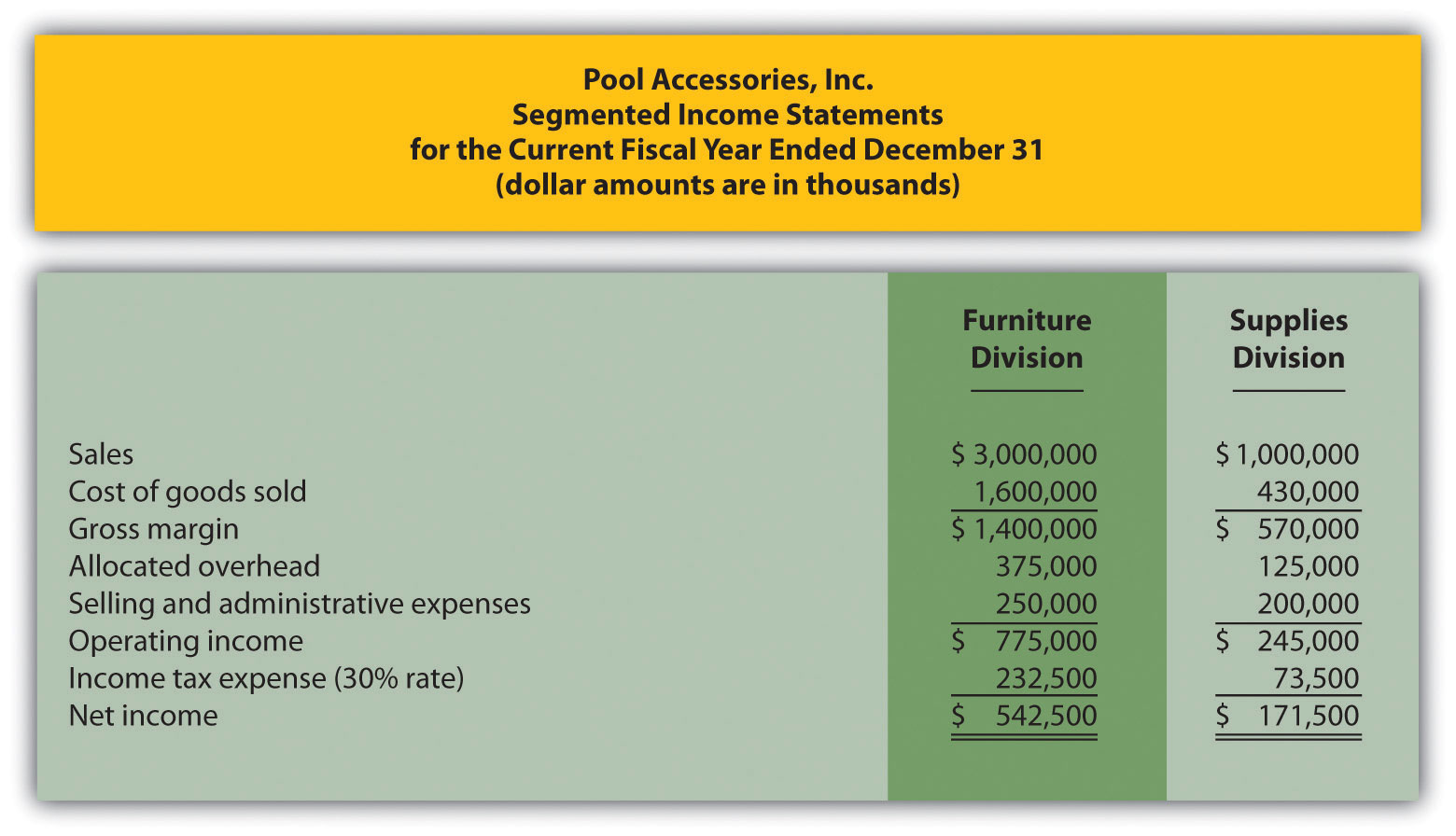

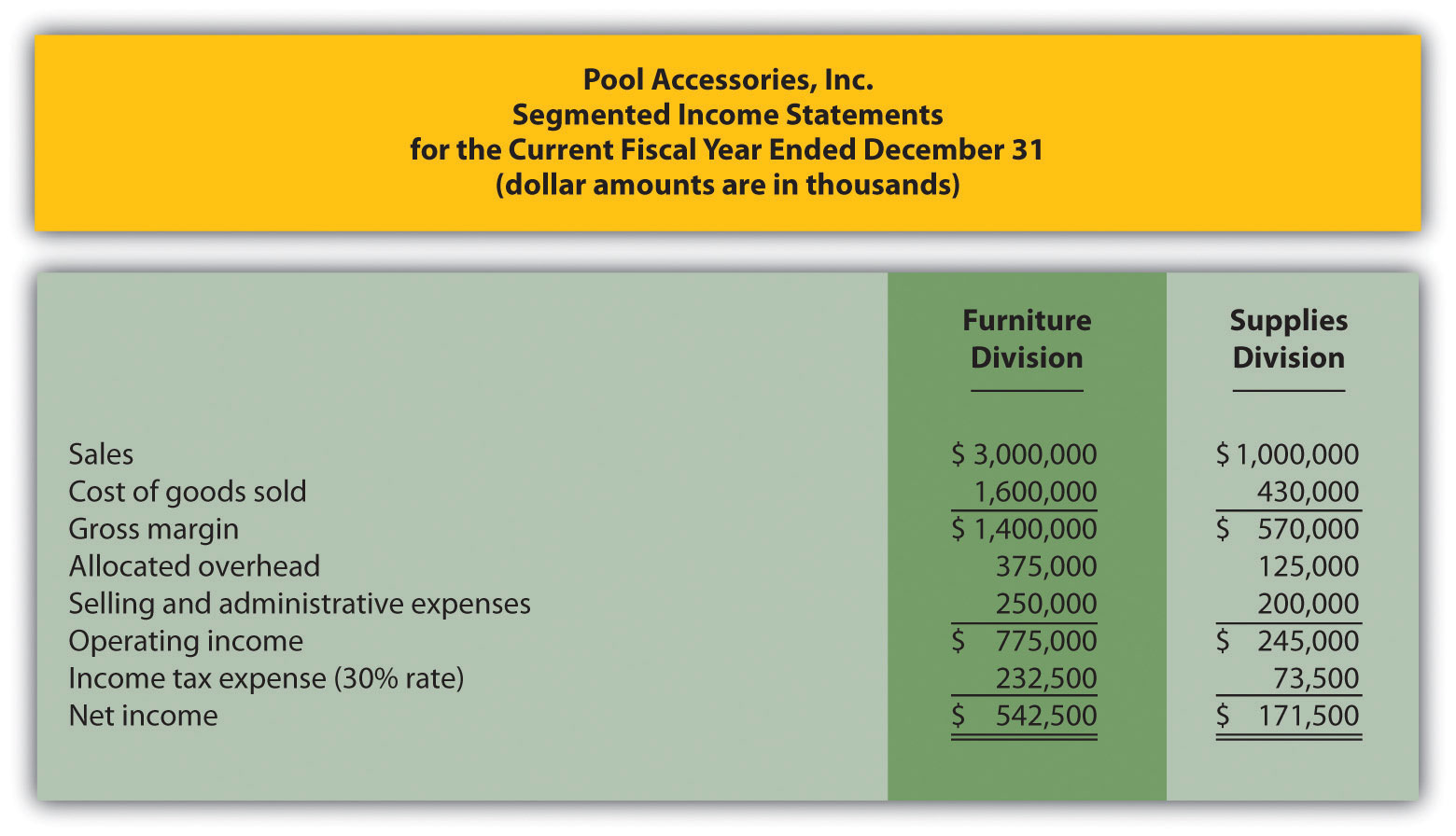

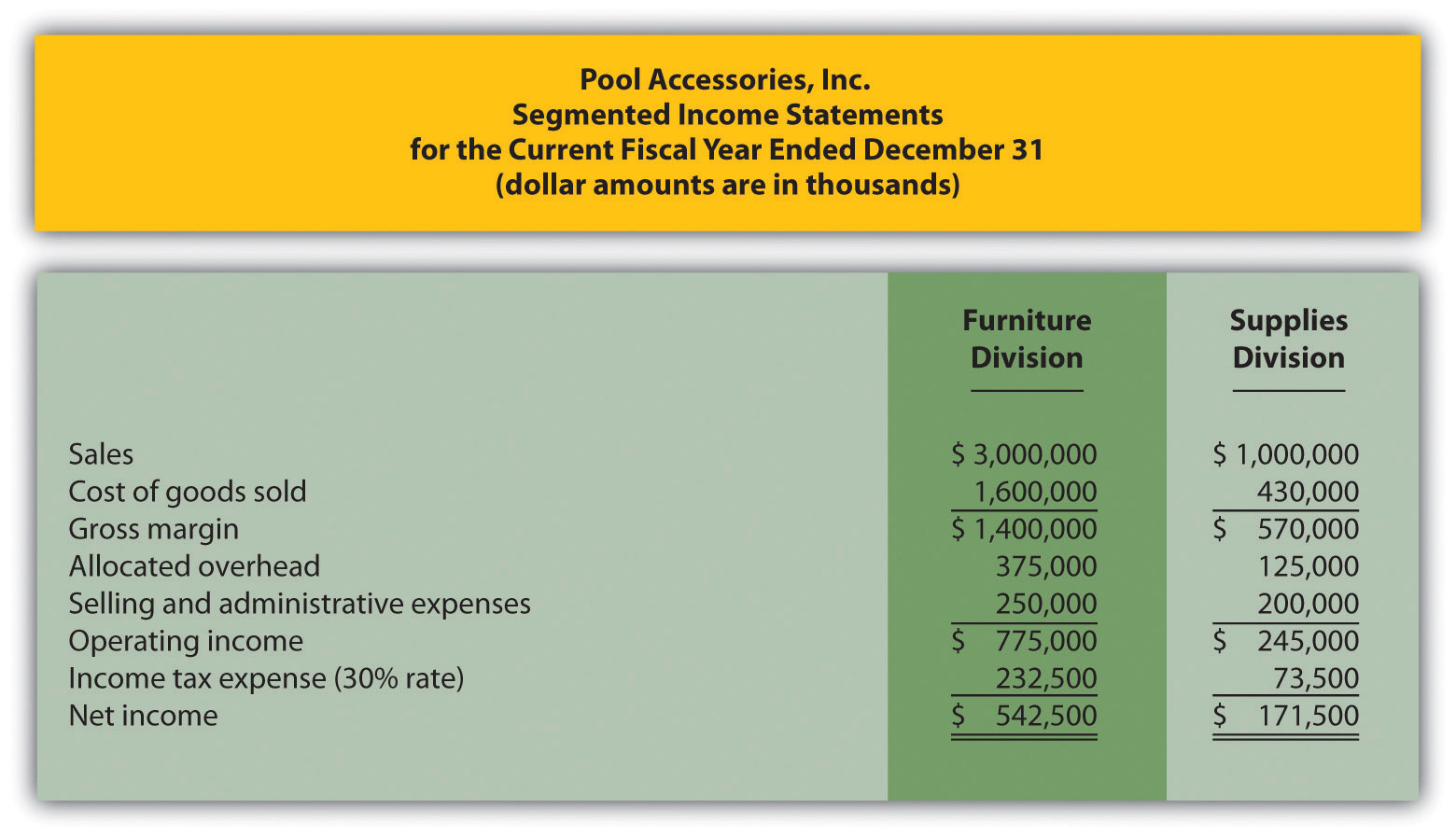

Segmented Net Income. Pool Accessories, Inc., has two divisions—Furniture and Supplies. The following segmented financial information is for the most recent fiscal year ended December 31.

Furniture Division Supplies Division Sales $3,000,000 $1,000,000 Cost of goods sold 1,600,000 430,000 Allocated overhead 375,000 125,000 Selling and administrative expenses 250,000 200,000 Assume the tax rate is 30 percent.

Required:

- Prepare a segmented income statement using the format presented in Figure 11.3 "Segmented Income Statements (Game Products, Inc.)". Include the profit margin ratio for each division at the bottom of the segmented income statement.

- Using net income as the measure, which division is most profitable? Explain why this conclusion might be misleading.

- What does the profit margin ratio tell us about each division? Why do organizations often use profit margin ratio to evaluate division performance rather than simply using net income?

-

ROI. Pool Accessories, Inc., has two divisions—Furniture and Supplies. (This is the same company as the previous exercise. This exercise can be assigned independently.) Segmented income statement information for the most recent fiscal year ended December 31 is shown as follows. Assume the Furniture division had average operating assets totaling $6,500,000 for the year, and the Supplies division had average operating assets of $1,750,000.

Required:

- Calculate ROI for each division.

- What does ROI tell us about each division? Indicate why this measure is useful in evaluating investment centers.

-

ROI Using Operating Profit Margin and Asset Turnover. Pool Accessories, Inc., has two divisions—Furniture and Supplies. (This is the same company as the previous exercises. This exercise can be assigned independently.) Segmented income statement information for the most recent fiscal year ended December 31 is shown as follows. Assume the Furniture division had average operating assets totaling $6,500,000 for the year, and the Supplies division had average operating assets of $1,750,000.

Required:

- For each division, calculate operating profit margin, asset turnover, and resulting ROI.

- Which division has the highest ROI? For the division that has the lowest ROI, what can be done to improve this ratio?

-

RI. Pool Accessories, Inc., has two divisions—Furniture and Supplies. (This is the same company as the previous exercises. This exercise can be assigned independently.) Segmented income statement information for the most recent fiscal year ended December 31 is shown as follows. Assume the Furniture division had average operating assets totaling $6,500,000 for the year, and the Supplies division had average operating assets of $1,750,000. Assume the cost of capital rate is 10 percent.

Required:

- Calculate RI for each division.

- What does RI tell us about each division?

-

Solving Unknowns for ROI. The following information is for two divisions at Kayak Company.

Lake Division Ocean Division Sales ? $900,000 Operating income ? $108,000 Operating profit margin 8.0 percent ? Average operating assets $150,000 $600,000 Asset turnover 1.7 ? ROI ? ? Required:

Find the missing information for each division.

-

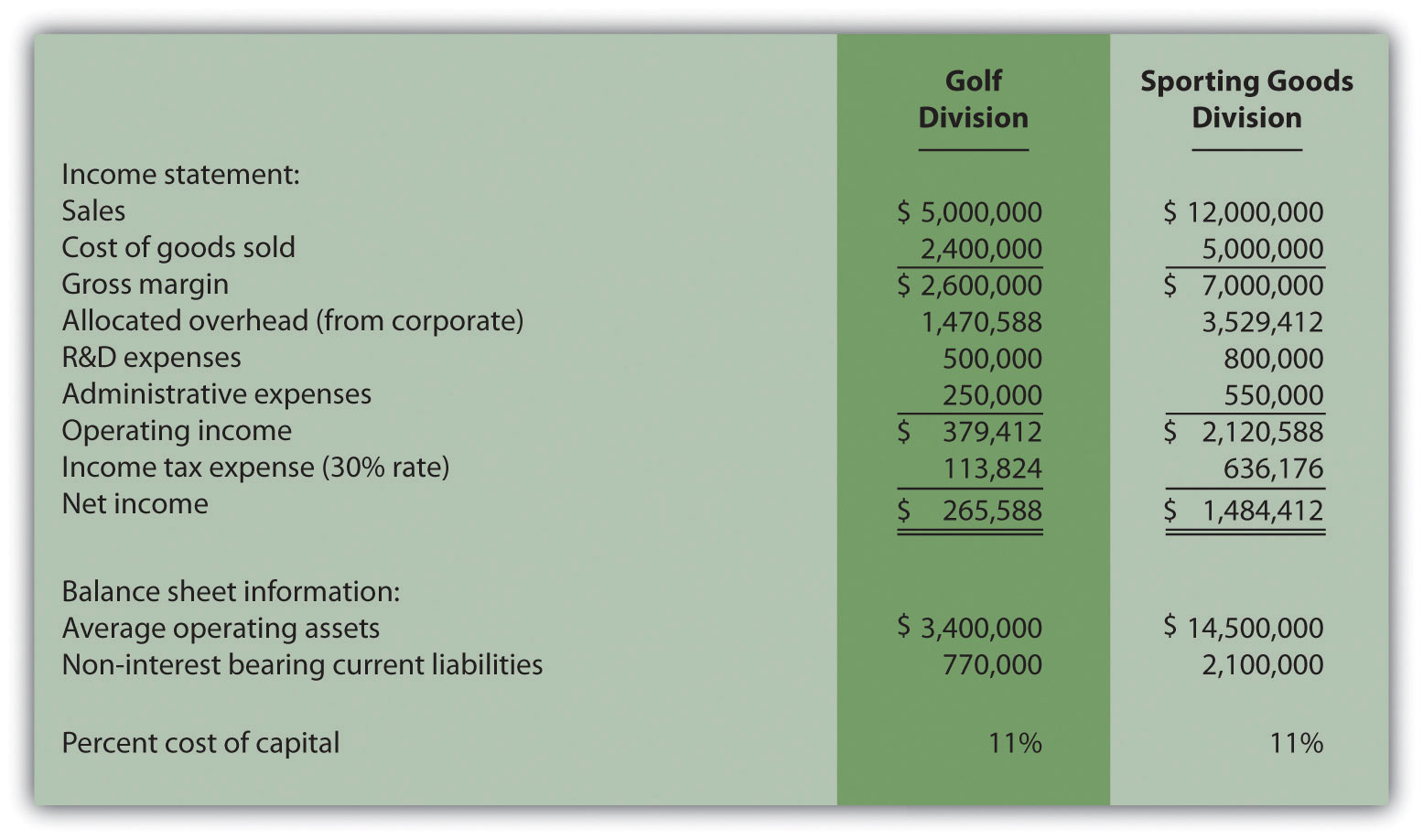

EVA. Links Company produces golf clubs and other sporting goods accessories. The following information is for each division at Links for the most recent fiscal year.

To calculate EVA, the management requires adjustments for R&D and noninterest bearing current liabilities as outlined in the following.

Research and development will be capitalized and amortized over several years resulting in an increase to average operating assets of $400,000 for the Golf division and $650,000 for the Sporting Goods division. On the income statement, R&D expense for the year will be added back to operating income; then R&D amortization expense for one year will be deducted. The current year amortization expense will total $100,000 for the Golf division and $150,000 for the Sporting Goods division.

Noninterest bearing liabilities will be deducted from average operating assets.

Required:

Calculate EVA for each division and comment on your results.

-

(Appendix) Transfer Pricing. Creative Colors, Inc., a producer of paint, has two divisions—Paint division and Can division. Each division manager is evaluated based on profit produced by each division.

The Can division sells its cans to the Paint division for $2 per case to cover variable costs. The Can division also sells to outside customers for $3 per case.

Required:

- Using the general economic transfer pricing rule, calculate the optimal transfer price assuming the Can division is below capacity.

- Using the general economic transfer pricing rule, calculate the optimal transfer price assuming the Can division is at capacity.

Exercises: Set B

-

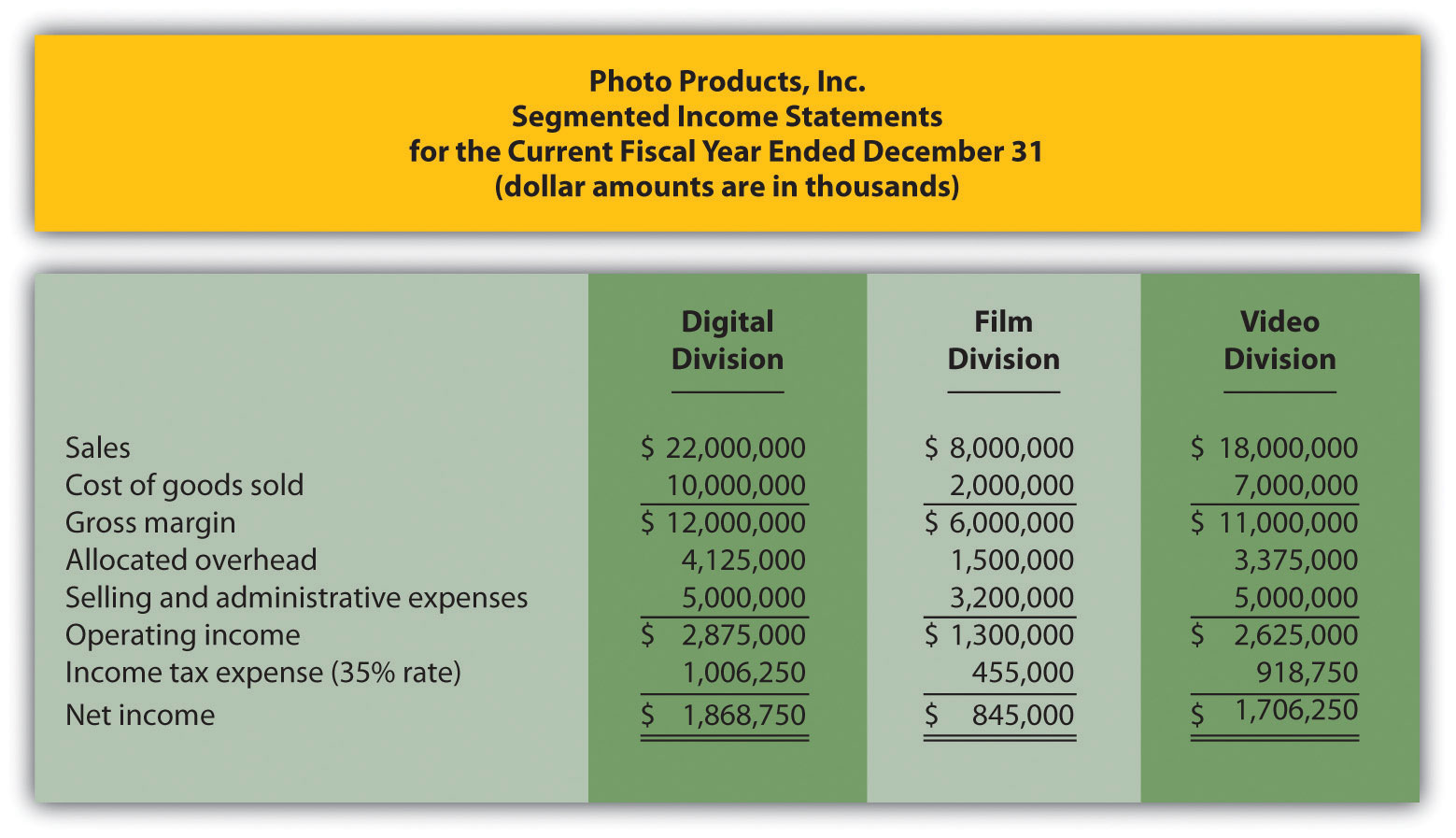

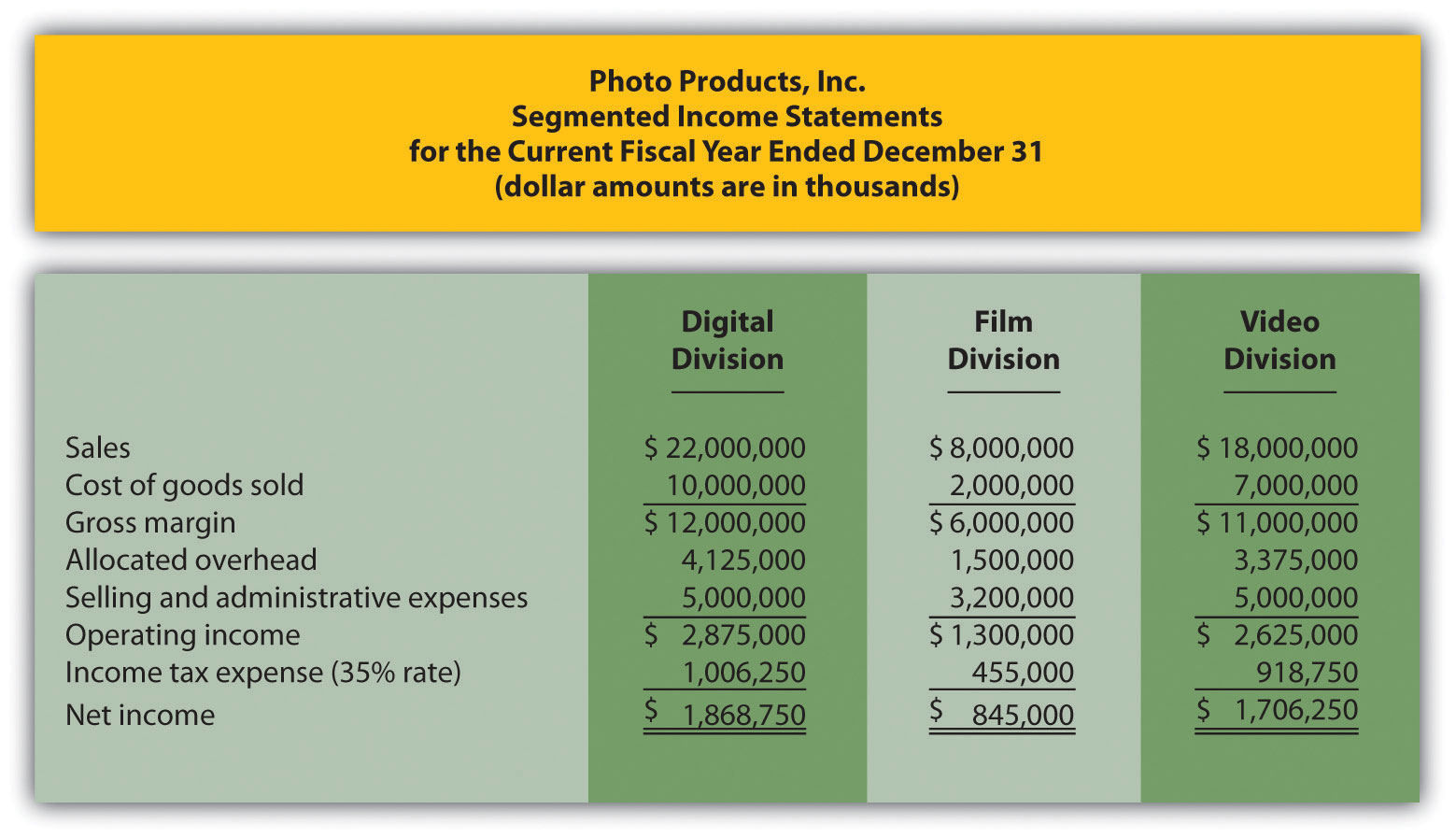

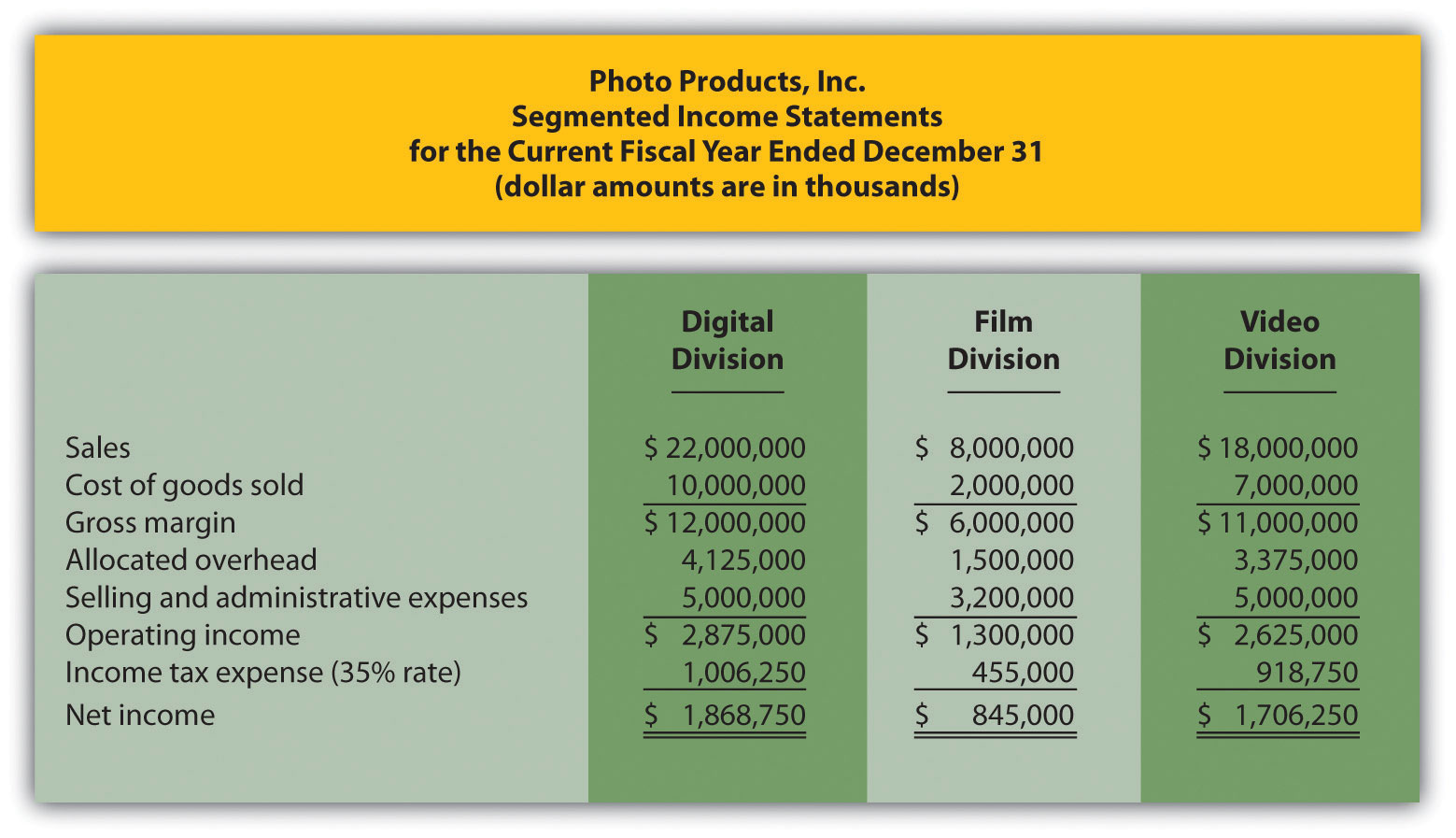

Segmented Net Income. Photo Products, Inc., has three divisions—Digital, Film, and Video. The following segmented financial information is for the most recent fiscal year ended December 31.

Digital Division Film Division Video Division Sales $22,000,000 $8,000,000 $18,000,000 Cost of goods sold 10,000,000 2,000,000 7,000,000 Allocated overhead 4,125,000 1,500,000 3,375,000 Selling and administrative expenses 5,000,000 3,200,000 5,000,000 Assume the tax rate is 35 percent.

Required:

- Prepare a segmented income statement using the format presented in Figure 11.3 "Segmented Income Statements (Game Products, Inc.)". Include the profit margin ratio for each division at the bottom of the segmented income statement.

- Using net income as the measure, which division is most profitable? Explain why this conclusion might be misleading.

- What does the profit margin ratio tell us about each division? Why do organizations often use profit margin ratio to evaluate division performance rather than simply using net income?

-

ROI. Photo Products, Inc., has three divisions—Digital, Film, and Video. (This is the same company as the previous exercise. This exercise can be assigned independently.) Segmented income statement information for the most recent fiscal year ended December 31 is shown as follows. Assume average operating assets totaled $15,000,000 for the Digital division, $6,500,000 for the Film division, and $17,500,000 for the Video division.

Required:

- Calculate ROI for each division.

- What does ROI tell us about each division? Indicate why this measure is useful in evaluating investment centers.

-

ROI Using Operating Profit Margin and Asset Turnover. Photo Products, Inc., has three divisions—Digital, Film, and Video. (This is the same company as the previous exercises. This exercise can be assigned independently.) Segmented income statement information for the most recent fiscal year ended December 31 is shown as follows. Assume average operating assets totaled $15,000,000 for the Digital division, $6,500,000 for the Film division, and $17,500,000 for the Video division.

Required:

- For each division, calculate operating profit margin, asset turnover, and resulting ROI.

- Which division has the highest ROI? For the division that has the lowest ROI, what can be done to improve this ratio?

-

RI. Photo Products, Inc., has three divisions—Digital, Film, and Video. (This is the same company as the previous exercises. This exercise can be assigned independently.) Segmented income statement information for the most recent fiscal year ended December 31 is shown as follows. Assume average operating assets totaled $15,000,000 for the Digital division, $6,500,000 for the Film division, and $17,500,000 for the Video division. Assume the cost of capital rate is 16 percent.

Required:

- Calculate RI for each division.

- What does RI tell us about each division?

-

Solving Unknowns for ROI. The following information is for two divisions at Arrowhead, Inc.

North Division South Division Sales $1,200,000 $400,000 Operating income $ 132,000 $ 40,000 Operating profit margin ? ? Average operating assets $1,000,000 ? Asset turnover ? ? ROI ? 8.0 percent Required:

Find the missing information for each division.

-

EVA. Sailboats, Inc., sells sailboat parts and accessories and provides rigging services. The following information is for each division at Sailboats, Inc., for the most recent fiscal year.

To calculate EVA, management requires adjustments for marketing and noninterest bearing current liabilities as outlined in the following.

Marketing will be capitalized and amortized over several years resulting in an increase to average operating assets of $100,000 for the Sales division and $65,000 for the Services division. On the income statement, marketing expense for the year will be added back to operating income; marketing amortization expense for one year will be deducted. The current year amortization expense will total $30,000 for the Sales division and $15,000 for the Services division.

Noninterest bearing liabilities will be deducted from average operating assets.

Required:

Calculate EVA for each division and comment on your results.

-

(Appendix) Transfer Pricing. Gail’s Gardening has two divisions—Retail and Nursery. The Retail division sells plants and supplies. The Nursery division takes tree seedlings and grows them to healthy young plants before selling the trees internally to the Retail division and to outside customers. Each division manager is evaluated based on profit produced by each division.

The Nursery division sells its trees to the Retail division for $4 per tree to cover its variable costs. The Nursery division also sells to outside customers for $6 per tree.

Required:

- Using the general economic transfer pricing rule, calculate the optimal transfer price assuming the Nursery division is below capacity.

- Using the general economic transfer pricing rule, calculate the optimal transfer price assuming the Nursery division is at capacity.

Problems

-

Segmented Net Income, ROI, and RI. Custom Auto Company has two divisions—East and West. The following segmented financial information is for the most recent fiscal year:

East Division West Division Sales $2,000,000 $4,000,000 Cost of goods sold 800,000 2,040,000 Allocated overhead 600,000 1,200,000 Selling and administrative expenses 360,000 380,000 The East division had average operating assets totaling $1,800,000 for the year, and the West division had average operating assets of $2,600,000. Assume the cost of capital rate is 8 percent, and the company’s tax rate is 30 percent. Division managers are responsible for sales, costs, and investments in assets.

Required:

- What type of responsibility center is each division at Custom Auto Company? Explain.

- Prepare a segmented income statement using the format presented in Figure 11.3 "Segmented Income Statements (Game Products, Inc.)". Include the profit margin ratio for each division at the bottom of the segmented income statement.

- Calculate ROI for each division.

- Calculate RI for each division.

- Summarize the answers to parts a, b, and c using the format presented in Figure 11.11 "Five Performance Measures at Game Products, Inc.". What does this information tell us about each division?

-

Investment Decisions Using ROI and RI. (Note: the previous problem must be completed before working this problem.) Assume each division of Custom Auto Company is considering separate investment opportunities expected to yield a return of 10 percent, well above the company’s minimum required rate of return of 8 percent. Each investment opportunity will require $1,000,000 in average operating assets and yield operating income of $100,000.

Required:

- Using the information presented in the previous problem, and the new investment proposal information presented previously, calculate each division’s overall ROI assuming the new investment is accepted.

- Compare your results in part a to each division’s ROI prior to the new investment (calculated in the previous problem). Which division(s) will likely accept the proposal and which will likely reject the proposal using ROI as the measure? Explain.

- Using the information presented in the previous problem, and the new investment proposal information presented previously, calculate each division’s overall RI assuming the new investment is accepted.

- Compare your results in part c to each division’s RI prior to the new investment (calculated in the previous problem). Which division(s) will likely accept the proposal and which will likely reject the proposal using RI as the measure? Explain.

- Assume the goal is to maximize company profit. Which measure do you think is best in deciding whether to accept a new investment proposal, ROI or RI? Explain.

-

Segmented Net Income, ROI, and RI; Making Investment Decisions. Quality Cycles, Inc., has two divisions—Cruisers and Racers. The following segmented financial information is for the most recent fiscal year:

Cruisers Division Racers Division Sales $6,000,000 $10,000,000 Cost of goods sold 2,500,000 4,000,000 Allocated overhead 375,000 625,000 Selling and administrative expenses 2,100,000 3,950,000 The Cruisers division had average operating assets totaling $5,700,000 for the year, and the Racers division had average operating assets of $9,600,000. Assume the cost of capital rate is 10 percent, and the company’s tax rate is 30 percent.

Required:

- Prepare a segmented income statement using the format presented in Figure 11.3 "Segmented Income Statements (Game Products, Inc.)". Include the profit margin ratio for each division at the bottom of the segmented income statement.

- Calculate ROI for each division.

- Calculate RI for each division.

- Summarize the answers to parts a, b, and c using the format presented in Figure 11.11 "Five Performance Measures at Game Products, Inc.". What does this information tell us about each division?

- Assume each division of Quality Cycles, Inc., is considering separate investment opportunities expected to yield a return of 16 percent, well above the company’s minimum required rate of return of 10 percent. Each investment opportunity will require $4,000,000 in average operating assets and yield operating income of $640,000.

- Using the information presented at the beginning of this problem, and the new investment proposal information presented previously, calculate each division’s overall ROI assuming the new investment is accepted.

- Compare your results in requirement e.1 to each division’s ROI prior to the new investment (calculated in requirement b). Which division(s) will likely accept the proposal and which will likely reject the proposal using ROI as the measure? Explain.

- Using the information presented at the beginning of this problem, and the new investment proposal information presented previously, calculate each division’s overall RI assuming the new investment is accepted.

- Compare your results in requirement e.3 to each division’s RI prior to the new investment (calculated in requirement c). Which division(s) will likely accept the proposal and which will likely reject the proposal using RI as the measure? Explain.

- Assume the goal is to maximize company profit. Which measure do you think is best in deciding whether to accept a new investment proposal, ROI or RI? Explain.

-

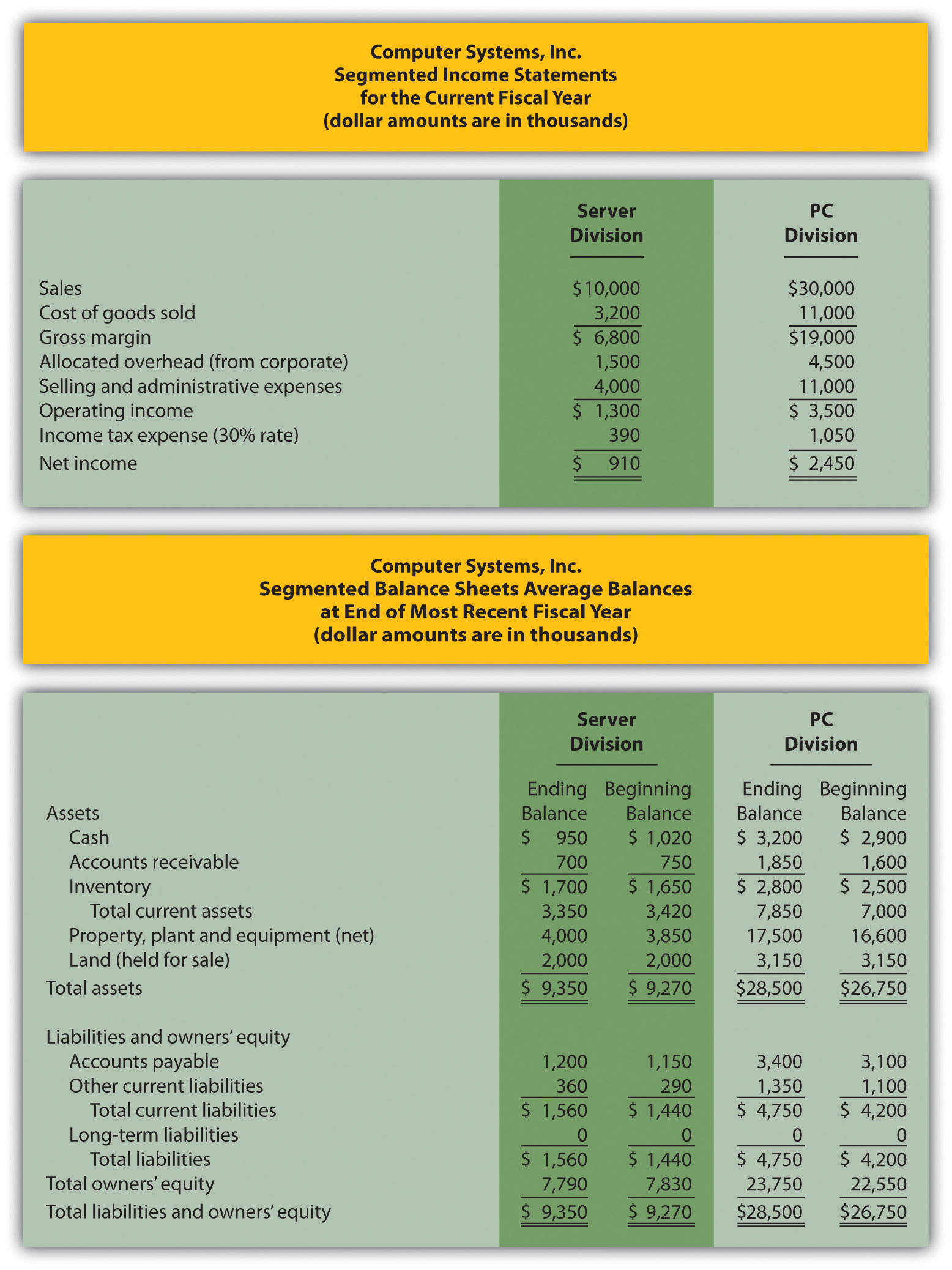

Operating Profit Margin, Asset Turnover, and ROI. Financial information for Computer Systems, Inc., for the most recent fiscal year appears as follows. All dollar amounts are in thousands.

Required:

- Calculate average operating assets for each division. (Hint: land held for sale is not an operating asset.)

- Calculate operating profit margin, asset turnover, and ROI for each division.

- What does this information tell us about each division?

-

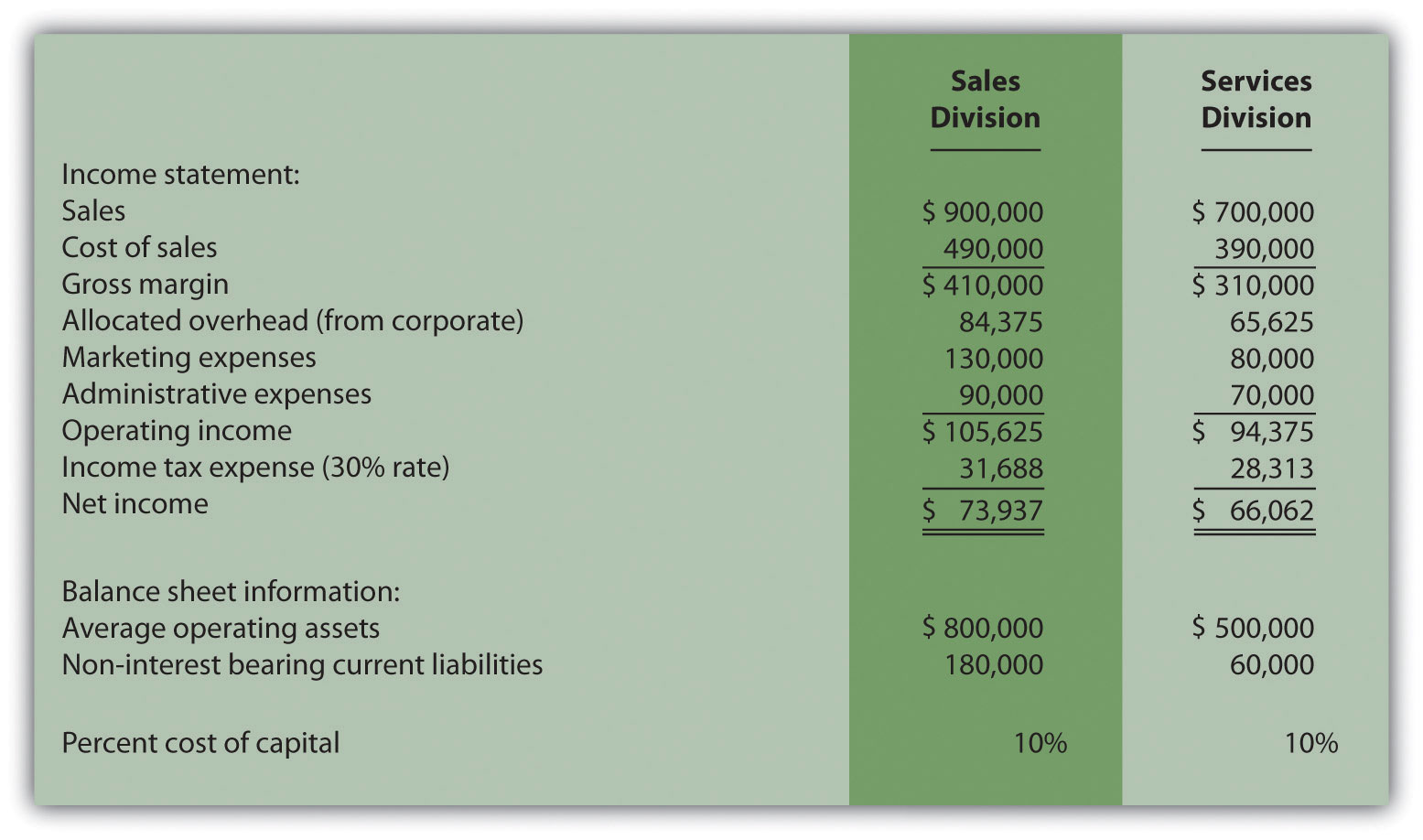

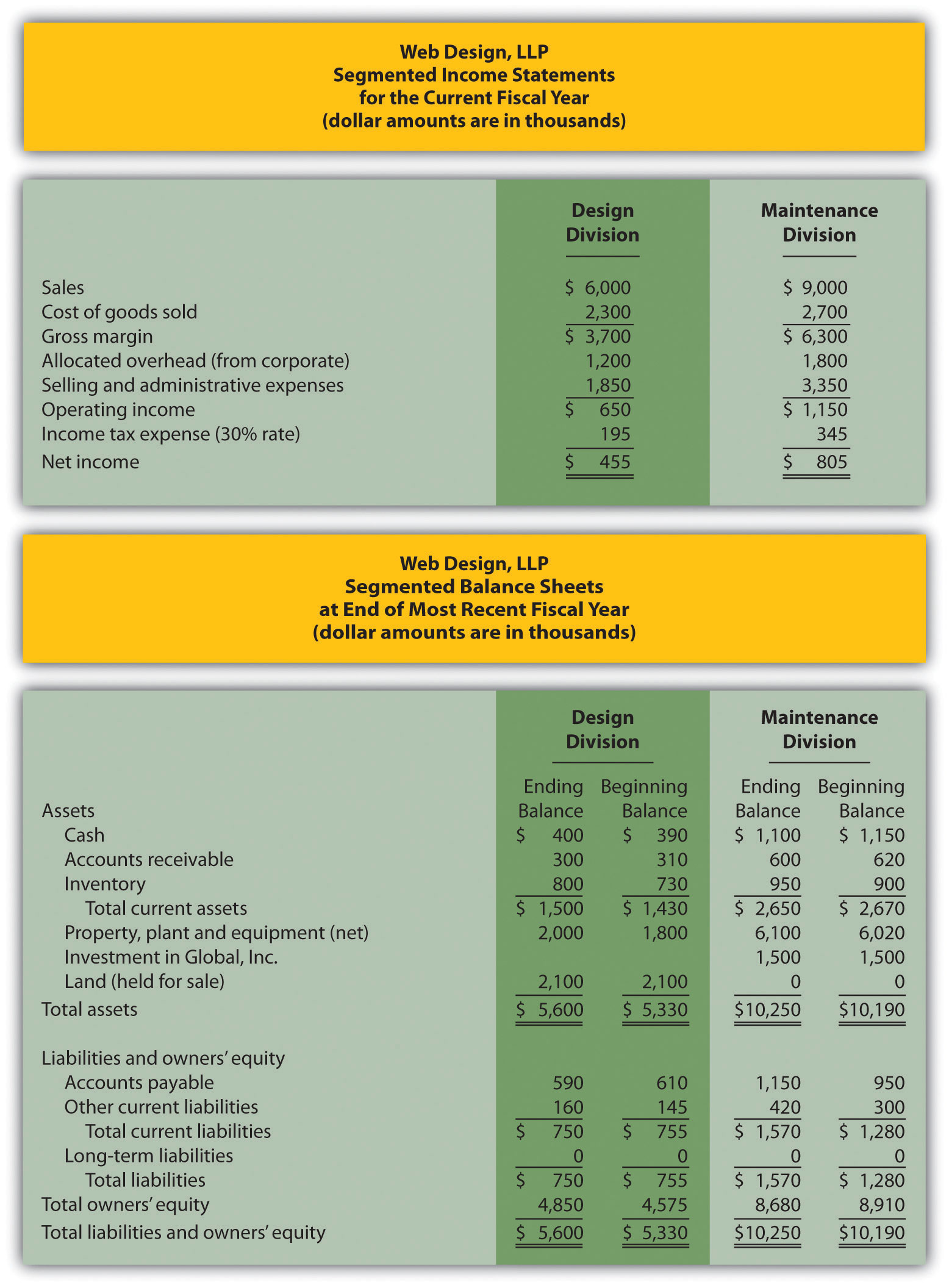

Operating Profit Margin, Asset Turnover, ROI, and RI. Financial information for Web Design, LLP, for the most recent fiscal year appears as follows. All dollar amounts are in thousands.

Required:

- Calculate average operating assets for each division. (Hint: land held for sale and investments in Global, Inc., are not operating assets.)

- Calculate operating profit margin, asset turnover, and ROI for each division.

- Calculate RI for each division assuming a cost of capital rate of 12 percent.

- What does the information from requirements b and c tell us about each division?

-

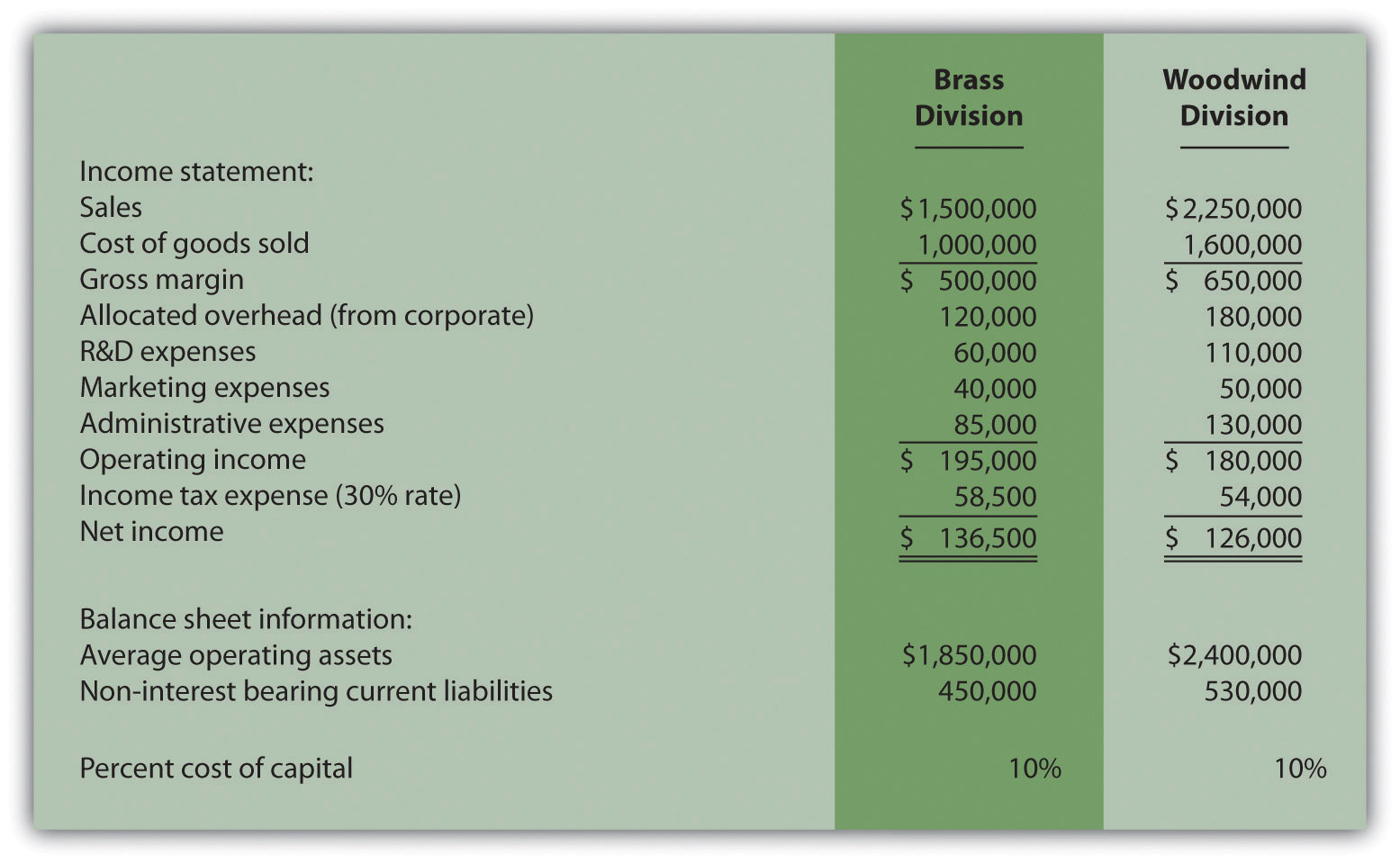

EVA. Conner, Inc., produces brass and woodwind music instruments. The following information is for each division at Conner for the most recent fiscal year.

To calculate EVA, management requires adjustments for R&D expenses, marketing expenses, and noninterest bearing current liabilities as outlined in the following.

Research and development will be capitalized and amortized over several years resulting in an increase to average operating assets of $40,000 for the Brass division and $80,000 for the Woodwind division. On the income statement, R&D expenses for the year will be added back to operating income; R&D amortization expense for one year will be deducted. The current year amortization expense will total $20,000 for the Brass division and $30,000 for the Woodwind division.

Marketing will be capitalized and amortized over several years resulting in an increase to average operating assets of $30,000 for the Brass division and $38,000 for the Woodwind division. On the income statement, marketing expenses for the year will be added back to operating income; marketing amortization expense for one year will be deducted. The current year amortization expense will total $10,000 for the Brass division and $12,000 for the Woodwind division.

Noninterest bearing current liabilities will be deducted from average operating assets.

Required:

- Calculate EVA for each division. What do the results show us for each division?

- Why does EVA typically require adjustments to operating income and average operating assets?

-

(Appendix) Transfer Pricing, Service Company. Kathy Kraven is the CEO and president of Legal Solutions, Inc. She oversees the company’s two divisions—Human Resources and Litigation. The Human Resources division provides legal services to personnel departments at various clients who need help creating personnel policies and manuals. The Litigation division provides legal services to support clients in litigation. Litigation often asks for help from Human Resources when faced with issues surrounding personnel policies but also has the option of seeking help outside the firm. Currently, Human Resources is below capacity and uses variable cost as its price for providing services to Litigation.

Since each division is evaluated by how much profit it generates, Human Resources would like to increase the price charged to Litigation. Litigation is steadfast against any such change. Kathy Kraven has stepped in and established the following policy: effective immediately, Human Resources will charge Litigation variable costs plus 20 percent for any services rendered internally.

Required:

- Why is the Human Resources division manager concerned about the price it charges to Litigation?

- Why is the Litigation division manager concerned about an increase in price charged by the Human Resources division?

- Do you think Kathy’s plan is effective? Explain.

- What other options are available for establishing transfer pricing?

-

(Appendix) Transfer Pricing, Retail Company. Fred’s Fishing Supplies has two divisions, Lake and Deep Sea. Each division manager is evaluated based on profit produced by each division. The Lake division often sells a certain graphite fishing rod internally to the Deep Sea division for $50 per rod to cover variable costs. The Lake division also sells the same graphite rod to outside customers for $60 per rod. The Deep Sea division manager has the option of purchasing a similar rod from an outside supplier for $56.

Required:

- Using the general economic transfer pricing rule, calculate the optimal transfer price assuming the Lake division is below capacity.

- Using the general economic transfer pricing rule, calculate the optimal transfer price assuming the Lake division is at capacity.

- The company’s CEO recently established the following policy: all internal transfers will be made at variable cost plus 20 percent. Assume the Lake division is operating below capacity. As the Deep Sea division manager, what would you do: purchase internally or purchase from an outside supplier? Why? How will your decision impact overall company profit?

One Step Further: Skill-Building Cases

- Segments at Hewlett-Packard. Refer to Note 11.12 "Business in Action 11.3" Why do you think Hewlett-Packard separates its operations into seven segments?

- Transfer Pricing at General Electric (Appendix). Refer to Note 11.50 "Business in Action 11.5" How does General Electric establish transfer prices? What does this approach imply with regards to the products and services being provided?

-

Group Activity—Decentralizing Operations. Each of the following scenarios is being considered at two separate companies.

- Walker Wood Products manufactures custom garage doors and custom furniture. The company recently experienced significant growth and top management would like to separate the company into two divisions—Garage and Furniture.

- Iron Manufacturing produces iron fencing for residential and commercial properties. The company recently experienced significant growth and top management would like to separate the company into two divisions—Residential and Commercial.

Required:

Form groups of two to four students. Each group is to perform the following requirements for the scenario assigned:

- Identify the potential advantages and disadvantages of decentralizing into two divisions and allowing the manager of each division to have complete control over operations.

- Discuss the findings of your group with the class.

- Internet Project—Economic Value Added. Stern Stewart & Company is a global consulting firm that pioneered the development of the EVA concept. Go to the Stern Stewart & Company Web site at http://www.sternstewart.com. Review the information provided at this Web site and write a one-page report summarizing the information you found to be most interesting. Also submit a printed copy of the information from the Web site with your report.

-

Creating a Segmented Income Statement Using Excel. Pool Accessories, Inc., has two divisions—Furniture and Supplies. The following segmented financial information is for the most recent fiscal year ended December 31.

Furniture Division Supplies Division Sales $3,000,000 $1,000,000 Cost of goods sold 1,600,000 430,000 Allocated overhead 375,000 125,000 Selling and administrative expenses 250,000 200,000 Assume the tax rate is 30 percent.

Required:

- Prepare an Excel spreadsheet similar to Figure 11.3 "Segmented Income Statements (Game Products, Inc.)" showing Pool Accessories’ segmented income statement and profit margin ratio for each division.

Comprehensive Case

-

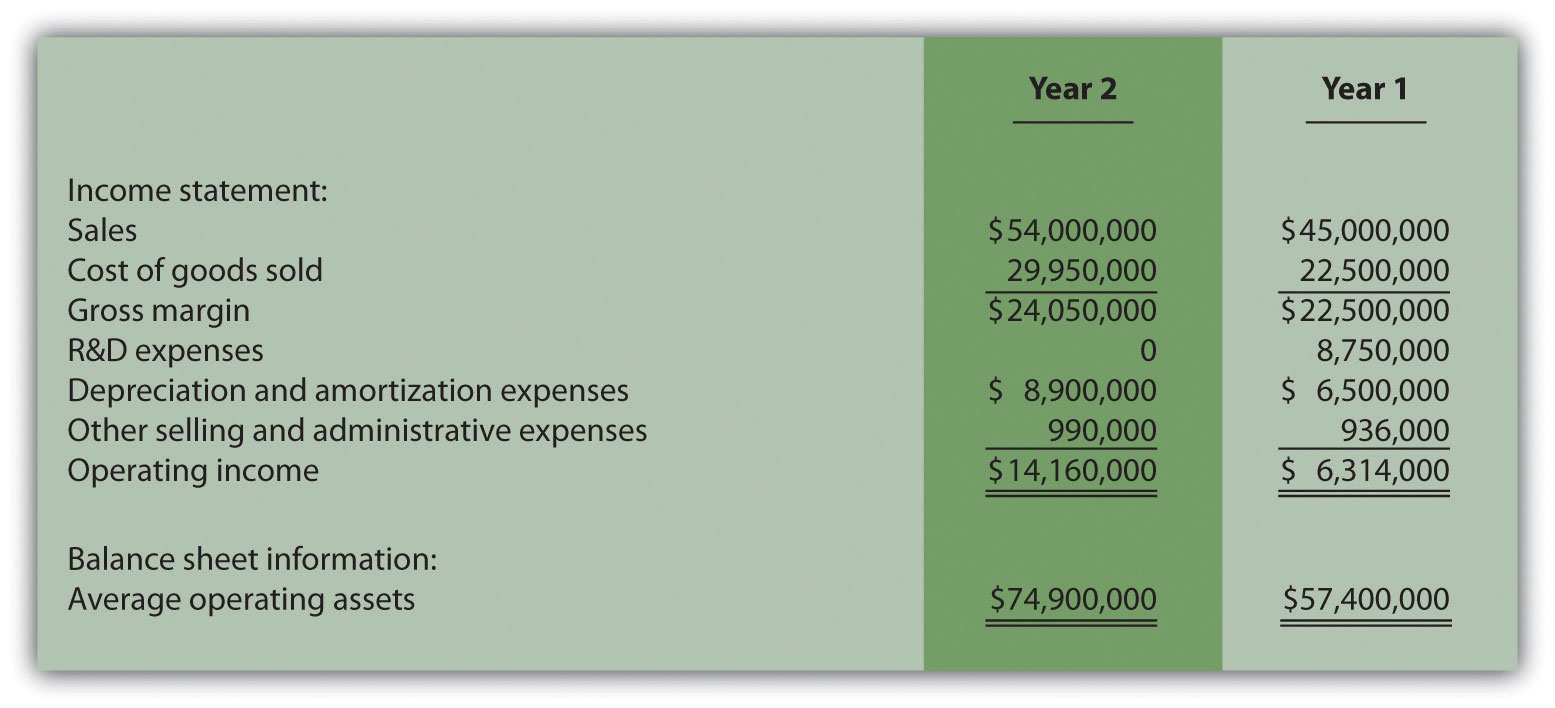

Ethics and ROI. Computer chip makers incur significant costs for research and development. Some research and development projects result in technologies used in new computer chips. Other research and development projects do not result in a useable technology. Because of the unpredictable nature of R&D activities, U.S. GAAP require that R&D costs be expensed in the period incurred.

Integrated Circuits, Inc. (ICI), produces computer chips and invests heavily in R&D. The firm has been struggling in recent years, and as a result, the board of directors hired a new top management group with the clear purpose of improving profitability. The board proposed a compensation package providing top managers with an annual bonus if the company’s operating income this coming year (year 2) increases 10 percent compared to year 1 and ROI remains above the 11 percent level achieved in year 1.

The new top management group is willing to accept this proposal, but only if costs related to successful R&D activities are capitalized and amortized over five years for internal reporting purposes. Their argument is most R&D activities benefit future years, and U.S. GAAP unfairly requires all R&D costs to be expensed in the period incurred, regardless of whether the activities are successful. This treatment by U.S. GAAP provides a disincentive for managers to invest in R&D projects that are vital to the company’s future survival. The board of directors agrees with this assertion and grants the new management group their request to capitalize costs for successful R&D activities over five years.

One year has passed with the new management group in place, and their financial results are presented as follows (for year two), along with last year’s information (year one). The entire $10,000,000 spent on R&D in year 2 was for unsuccessful projects since management decided to go a different direction with the company’s technology at the end of year 2. Nevertheless, top management capitalized the entire $10,000,000 and amortized these costs over 5 years as reflected in the year 2 financial results. (Note: of this amount, $2,000,000 is included in depreciation and amortization expense for year 2, and $8,000,000 is included in average operating assets for year 2.)

Required:

- Based on the financial data presented, calculate ROI for each year and the percent change in operating income from year 1 to year 2. Does the new management group qualify for the bonus?

- Prepare revised financial information in the same format as presented previously assuming none of the $10,000,000 in year 2 R&D costs are capitalized and amortized. (Hint: Amounts for year 1 will remain the same. Income statement and balance sheet amounts for year 2 will change.) Calculate the revised ROI for year two, and the revised percent change in operating income from year one to year two. Based on your results, would the new management group qualify for the bonus?

- Is the new management group’s treatment of R&D costs for year 2 ethical?

- How should the board of directors respond to the new management group’s assertion that $10,000,000 in R&D costs should be capitalized in year 2?

-

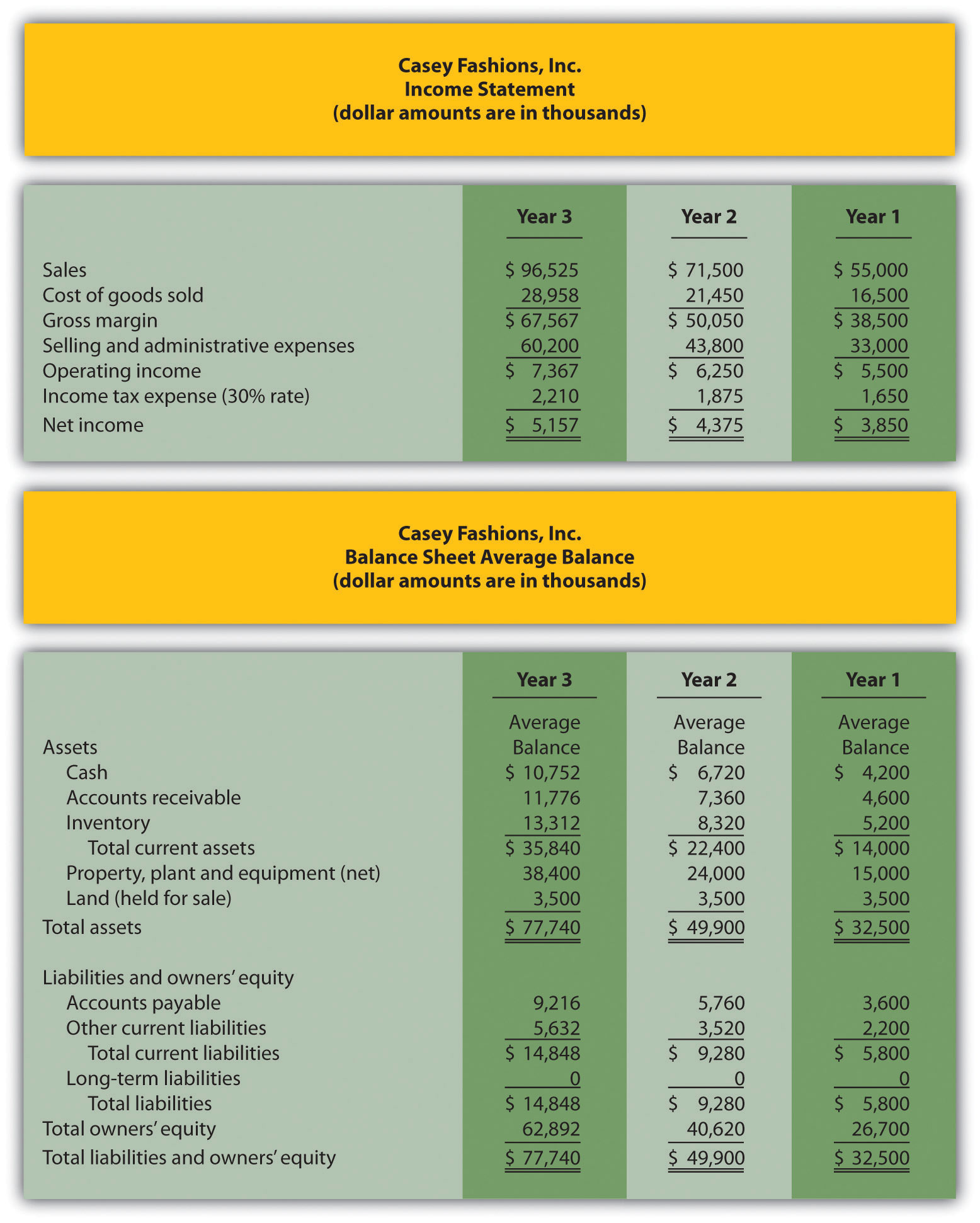

Performance Evaluation Methods. Casey Fashions, Inc., sells clothing throughout North America. The company’s compensation committee, made up of five members from the board of directors, is meeting to discuss the CEO’s contract, which expires next month. The committee is currently reviewing financial information for the three most recent fiscal years: year 3 (most recent), year 2, and year 1 (shown as follows).

The income statement indicates sales increased 30 percent from year 1 to year 2 and 35 percent from year 2 to year 3. Net income increased 14 percent from year 1 to year 2, and 18 percent from year 2 to year 3. One member on the committee, Chris Carson, would like to offer the CEO a multiyear extension with a significant bump in salary and thousands of shares of stock options. When questioned why, Chris pointed to the positive results reflected on the income statement.

Another committee member, Mary Nichols, agrees with Chris that income statement trends look great, but she would like to review other measures of performance as well. Mary has asked you to come up with two measures of performance that go beyond simply looking at the income statement.

Required:

- Calculate ROI for each of the three years. Note that balance sheet amounts presented for each year are already average balances (i.e., no need to calculate average balances). Assume land held for sale is not an operating asset.

- Calculate RI for each of the 3 years assuming the company’s cost of capital rate is 12 percent.

- Prepare a written report to the compensation committee summarizing and explaining your findings in part a and b.