This is “Chapter Wrap-Up: Summary of Cost Flows at Custom Furniture Company”, section 2.5 from the book Accounting for Managers (v. 1.0). For details on it (including licensing), click here.

For more information on the source of this book, or why it is available for free, please see the project's home page. You can browse or download additional books there. To download a .zip file containing this book to use offline, simply click here.

2.5 Chapter Wrap-Up: Summary of Cost Flows at Custom Furniture Company

Learning Objective

- Use a job costing system to track costs and evaluate profitability for each job.

Question: The goal of this section is to pull it all together for Custom Furniture Company. We begin by looking at revenue and cost information for May, including manufacturing and nonmanufacturing costs. Why is it important for companies like Custom Furniture Company to correctly classify and record costs such as direct materials (e.g., wood used for each table), salaries of administrative personnel, and rent on the factory?

Answer: Companies must be able to evaluate the profitability of each job and on a broader scale, evaluate the overall profitability of the company. This requires that all manufacturing and nonmanufacturing costs be classified and recorded correctly in the general journal. The following information shows how to accomplish this with transactions for the month of May at Custom Furniture Company.

Revenue and Cost Information for Custom Furniture Company

Question: How are the typical transactions for a manufacturing company recorded in the general journal?

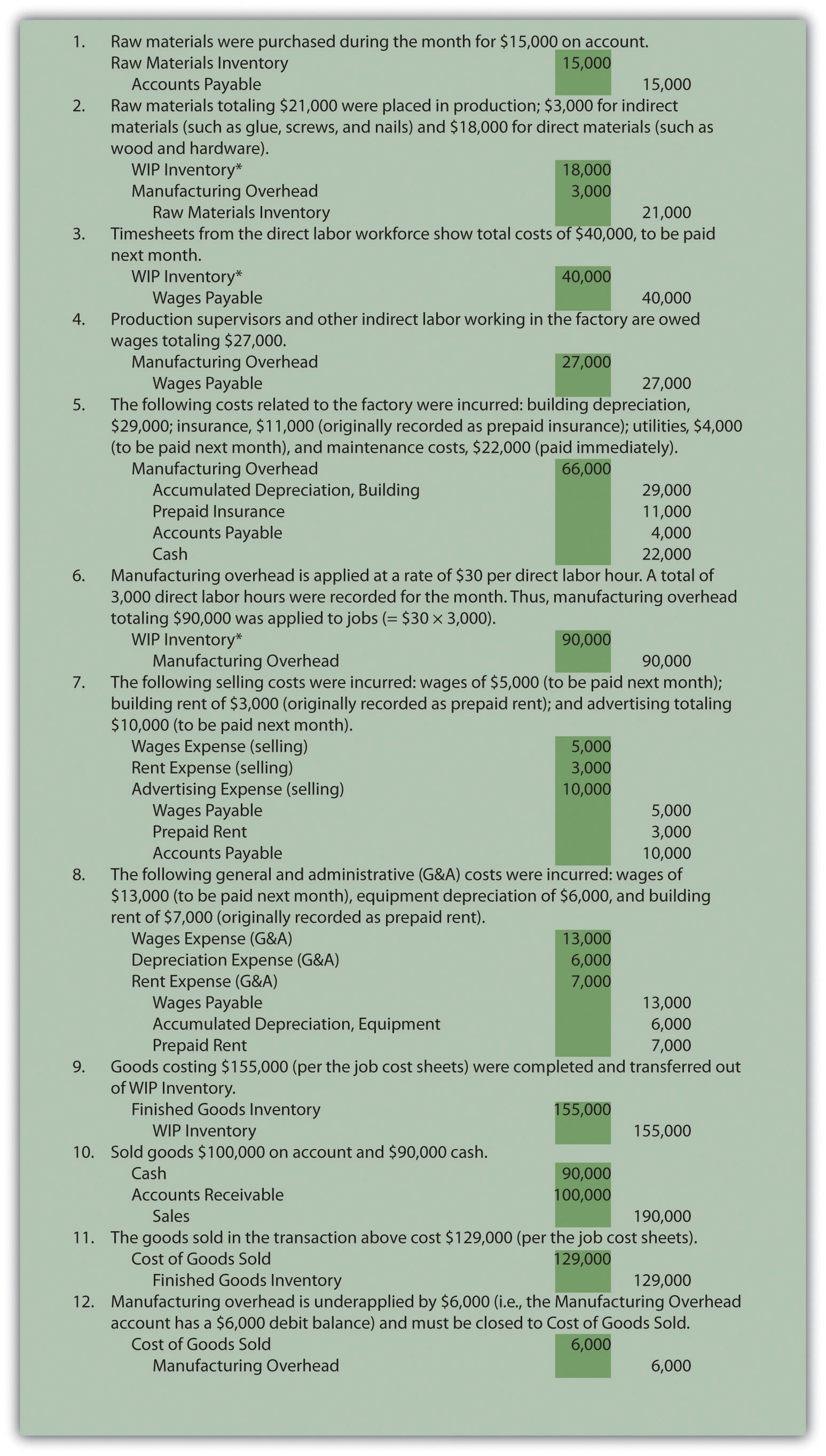

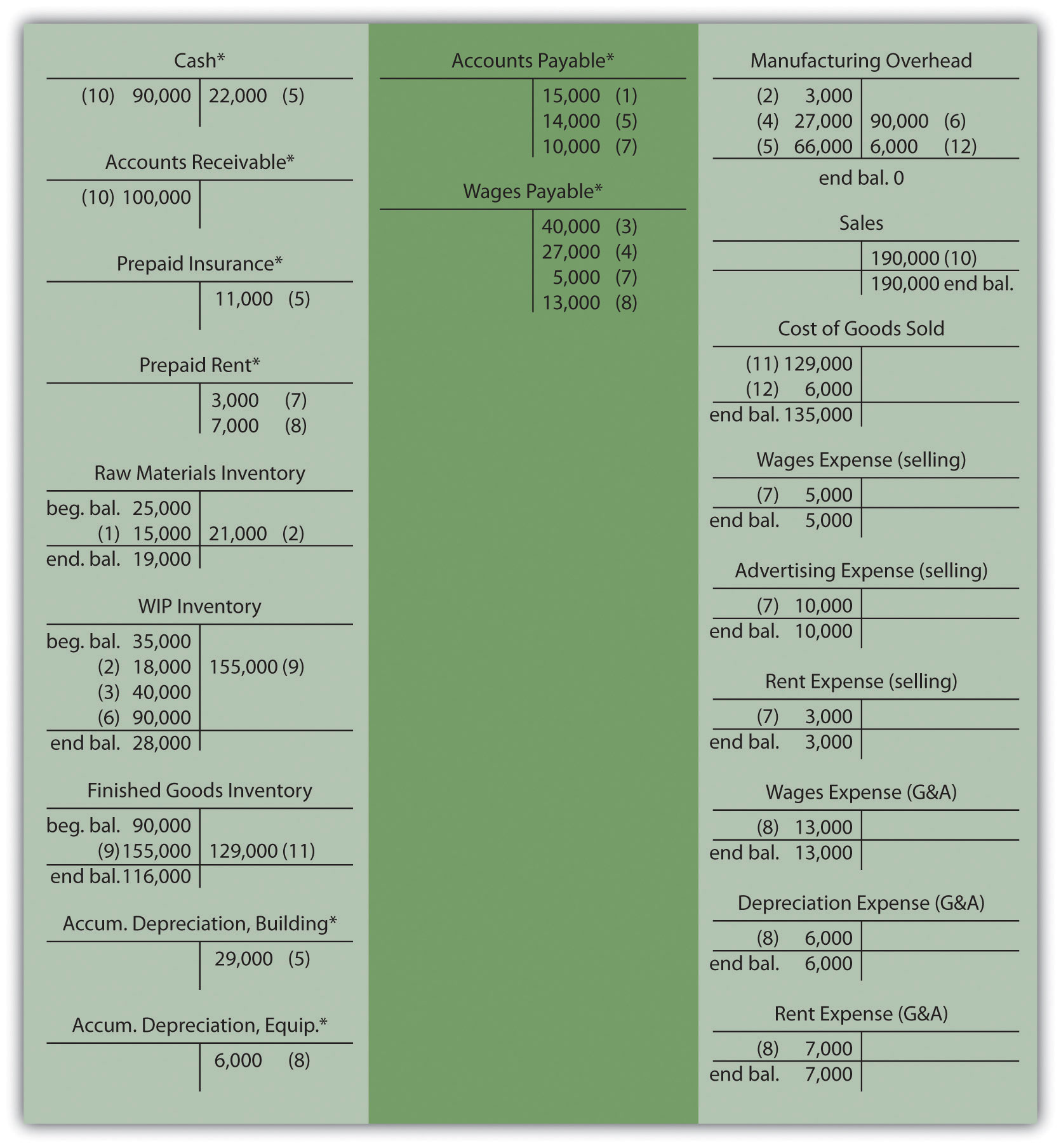

Answer: Figure 2.7 "Custom Furniture Company’s Journal Entries for May" shows Custom Furniture Company’s journal entries for May. Figure 2.8 "Custom Furniture Company’s T-Accounts" presents the same information in T-account format. (Note that each entry shows the total dollar amount for the month rather than individual transaction amounts.) If you understand how to make an entry summarized in total, you know how to make each individual (perhaps daily) entry. Beginning balances for raw materials inventory ($25,000), work-in-process inventory ($35,000), and finished goods inventory ($90,000) are shown in the T-accounts in Figure 2.8 "Custom Furniture Company’s T-Accounts". Although it is not necessary to refer back to Chapter 1 "What Is Managerial Accounting?" at this point, we should note that the beginning balance and transaction amounts used here for these three inventory accounts tie back to the three schedules presented in Chapter 1 "What Is Managerial Accounting?" (schedule of raw materials placed in production, schedule of cost of goods manufactured, and schedule of cost of goods sold).

Figure 2.7 Custom Furniture Company’s Journal Entries for May

*All debit amounts to work-in-process inventory are also recorded on the appropriate job cost sheets.

Figure 2.8 Custom Furniture Company’s T-Accounts

*Beginning and ending balances are only provided for inventory accounts since the focus of this chapter is on manufacturing costs that flow through the inventory accounts.

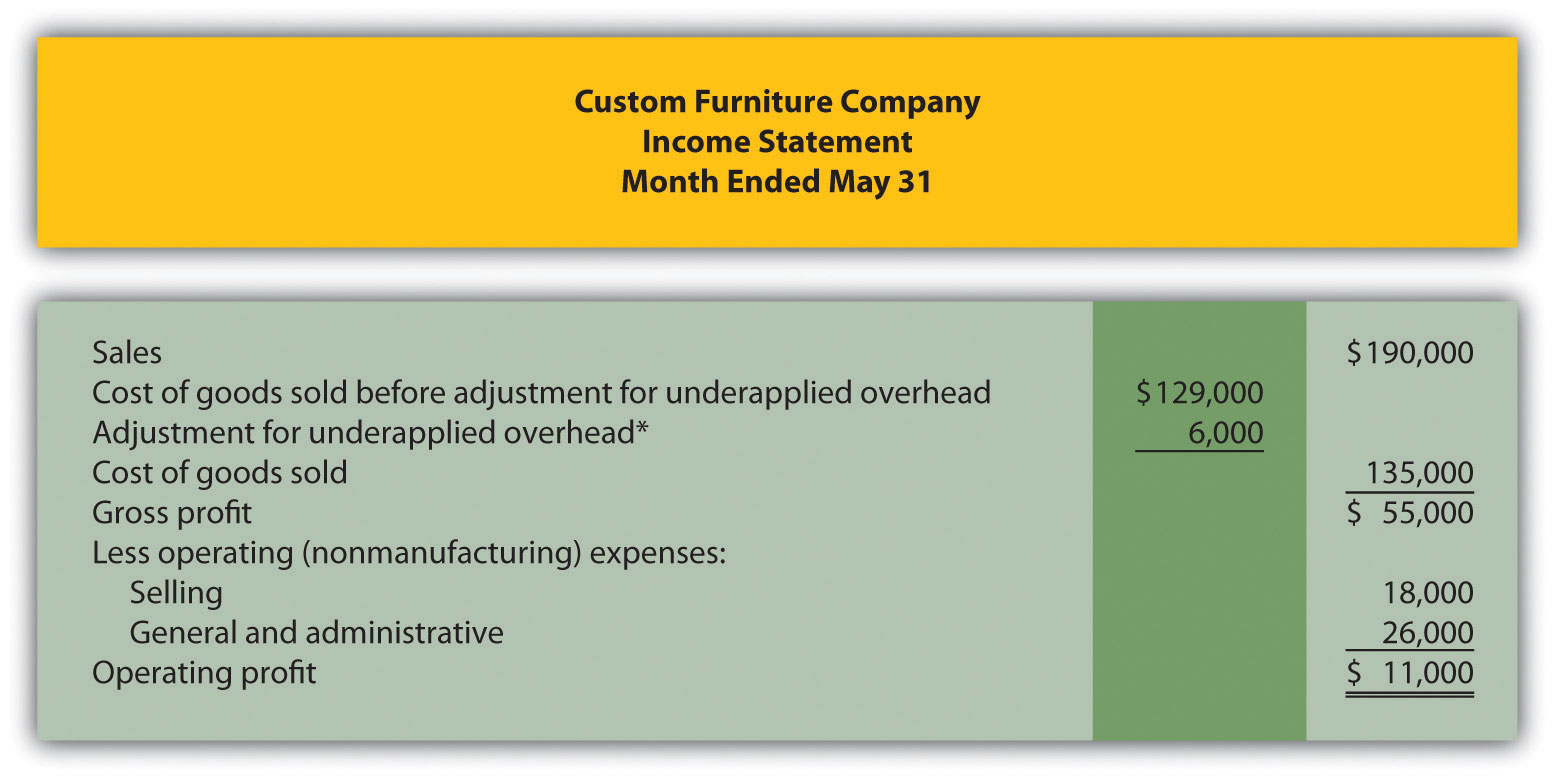

Question: Now that the information for the month of May has been recorded for Custom Furniture Company, we need to summarize this information to evaluate the profitability of the company and the profitability of jobs. How profitable was Custom Furniture for the month of May?

Answer: Custom Furniture Company’s income statement for the month of May, shown in Figure 2.9 "Custom Furniture Company’s Income Statement", indicates the company had operating profit of $11,000. This information comes directly from the T-accounts shown in Figure 2.8 "Custom Furniture Company’s T-Accounts".

Figure 2.9 Custom Furniture Company’s Income Statement

*See entry 12 in Figure 2.7 "Custom Furniture Company’s Journal Entries for May" and Figure 2.8 "Custom Furniture Company’s T-Accounts" for this adjustment. This represents the amount of overhead underapplied to jobs and closed out to cost of goods sold at the end of May. An alternative presentation is to simply show the cost of goods sold amount of $135,000 directly under sales.

Analysis of Job Profitability at Custom Furniture Company

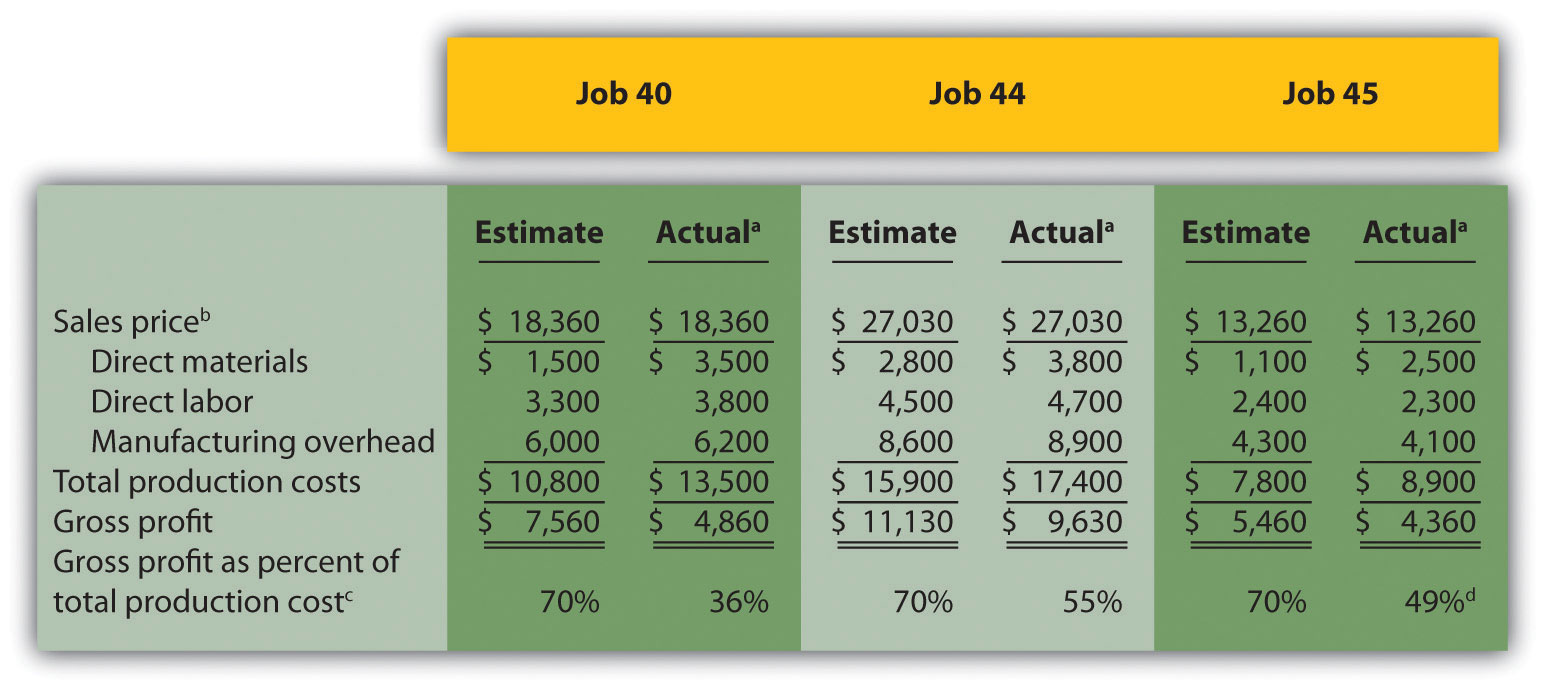

Recall from the beginning of the chapter that Dan Stevens, the owner of Custom Furniture Company, is concerned about the company’s profitability. Although Dan prices his furniture at 70 percent above estimated production costs, the company had only $11,000 in profits for the month of May, as shown in Figure 2.9 "Custom Furniture Company’s Income Statement". Dan asked Leslie (the accountant) to look into the accuracy of his estimates by reviewing actual production costs for the three costliest tables produced in May. As you read Leslie’s comments, be sure to look at the income statement in Figure 2.9 "Custom Furniture Company’s Income Statement" and the job cost estimates and actual results in Figure 2.10 "Job Cost Estimates Versus Actual Results for Custom Furniture Company".

Figure 2.10 Job Cost Estimates Versus Actual Results for Custom Furniture Company

a Product costs are from the job cost sheet, and the sales price is based on the original bid.

b Based on 70 percent markup of estimated total production costs. For example, job 40’s sales price of $18,360 = $10,800 × 170 percent.

c Equals gross profit divided by total production costs. Company target is 70 percent.

d Rounded.

| Leslie: | Dan, I have the production cost information you requested. |

| Dan: | Great! What did you find out? |

| Leslie: | Well, first I looked at the income statement for May. If you establish prices based on a 70 percent markup of production costs, then sales revenue should be 170 percent of cost of goods sold, and the resulting gross profit should be 70 percent of cost of goods sold. |

| Dan: | Sounds reasonable. Are we anywhere near these numbers? |

| Leslie: | Not really. Cost of goods sold for May total $135,000, so sales should be closer to $229,500 (that would be $135,000 times 170 percent), and gross profit should be closer to $94,500, which is $135,000 times 70 percent. As you can see on the income statement, we didn’t get very close to these numbers. |

| Dan: | Do you have any idea why? |

| Leslie: | I pulled together production cost information from our job costing system for the three highest-cost tables produced in May as you requested. |

| Dan: | And? |

| Leslie: | I compared the job cost sheet information for each item with your original estimates, and here’s what I found. It looks as if the problem is with direct materials. All three jobs show that direct material costs were significantly higher than you estimated. Direct labor and manufacturing overhead costs were pretty close. |

| Dan: | Wow, I’m surprised that direct material costs were so high. I’ll have to check into this further. I do recall wood costs increasing over the last couple of months, but not to this extent. |

| Leslie: | There are lots of potential causes for the increase in direct materials. Perhaps materials were wasted as a result of machine problems or because of inexperienced employees. |

| Dan: | Let’s try to nail down why my estimates are so far off so I can do a better job of estimating costs in the future. |

| Leslie: | Good idea—I’ll look into the direct materials costs and get back to you later this week. |

Question: Figure 2.10 "Job Cost Estimates Versus Actual Results for Custom Furniture Company" provides an in depth view of the costs associated with each job and the resulting profitability. How does this information help Custom Furniture Company plan for the future?

Answer: This information helps managers assess the profitability of individual jobs. Custom Furniture Company was able to identify areas of concern by comparing information from job cost sheets with Dan’s estimates. Dan and Leslie will have to do more research to find the cause of the high material costs. If changes cannot be made to the production process to reduce these costs, Dan may have to consider revising his estimates and raising prices on future jobs. The goal is to provide enough information for the company to make informed decisions about areas of concern, such as direct materials costs, and how much to charge for future jobs.

Key Takeaways

- Job costing systems can do more than simply track the costs of each job. Companies also use these systems to track revenue and the resulting profit for each job.

- A job costing system can be used to identify areas of concern by comparing the cost estimate prepared before starting the job with information on the completed job cost sheet. This type of analysis often leads to changes in the production process and revised estimates for future jobs.

Review Problem 2.5

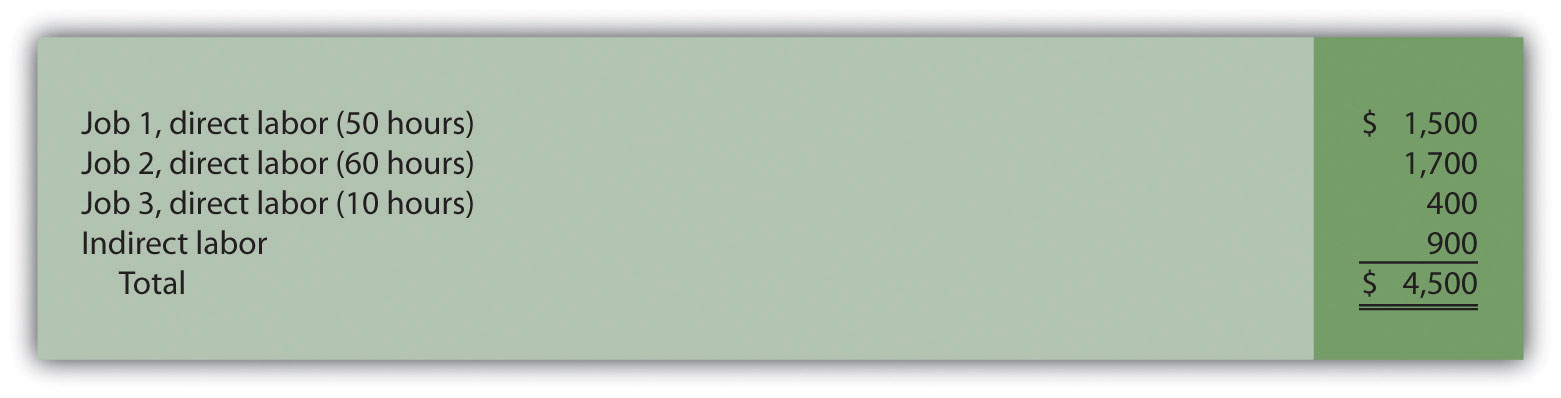

Farm Equipment, Inc., produces tractors and other farm machinery. Each piece of equipment is built to customer specifications. During May, its first month of operations, Farm Equipment, Inc., began working on three customer orders: jobs 1, 2, and 3. The following transactions occurred during May:

- Purchased production materials on account totaling $450,000

-

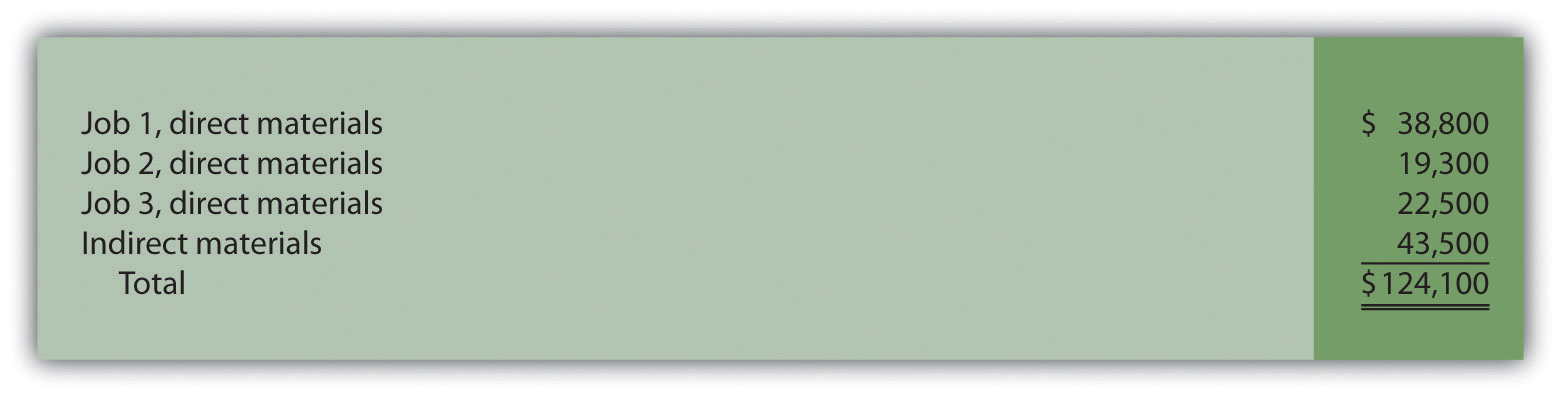

Processed material requisitions for the following items:

-

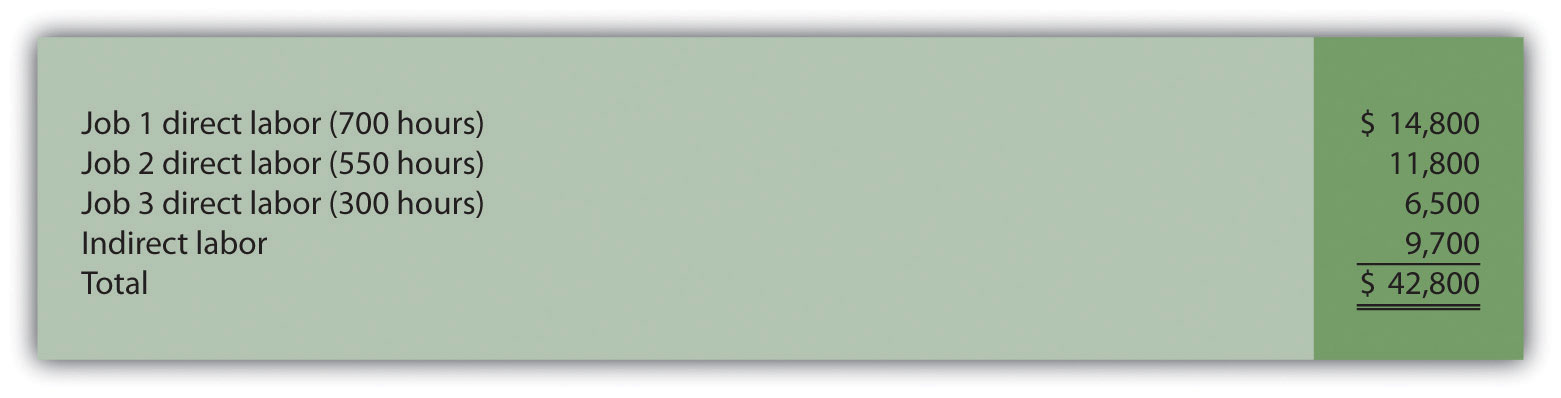

Processed timesheets showing the following:

- Applied overhead using a predetermined rate of 160 percent of direct labor cost

- Completed job 1 and transferred it to finished goods

- Delivered job 1 to the customer and billed her $140,000. (Hint: Two entries are required—one for the cost of the goods and another for the revenue.)

Required:

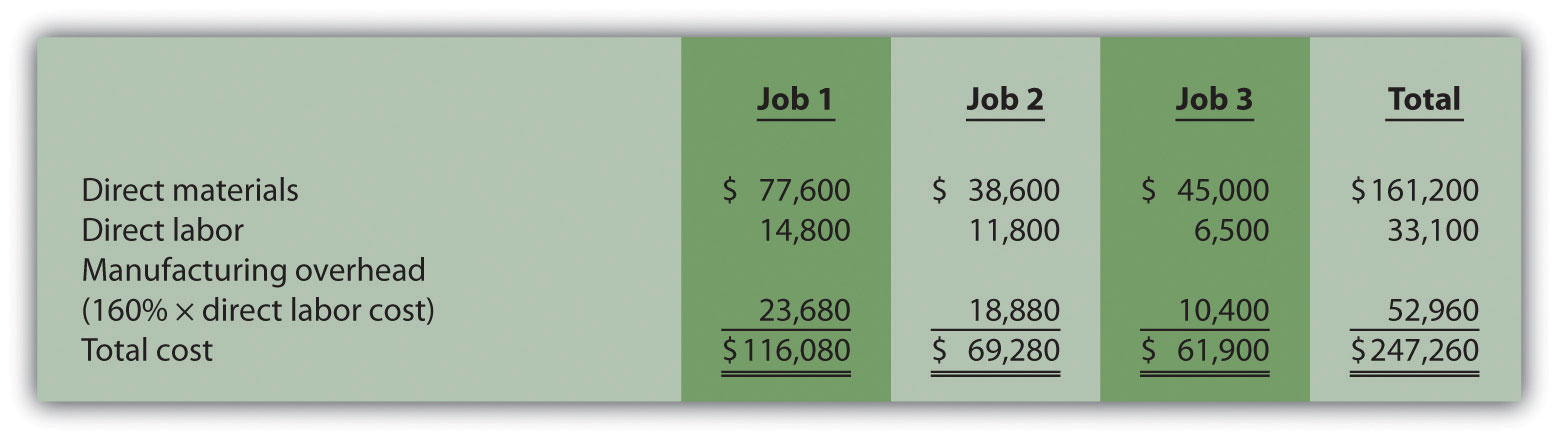

- Calculate the production costs incurred in May for each of the three jobs.

- Make the appropriate journal entry for each item described previously. Assume all payments will be made next month. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- How much gross profit did Farm Equipment, Inc., earn from the sale of job 1?

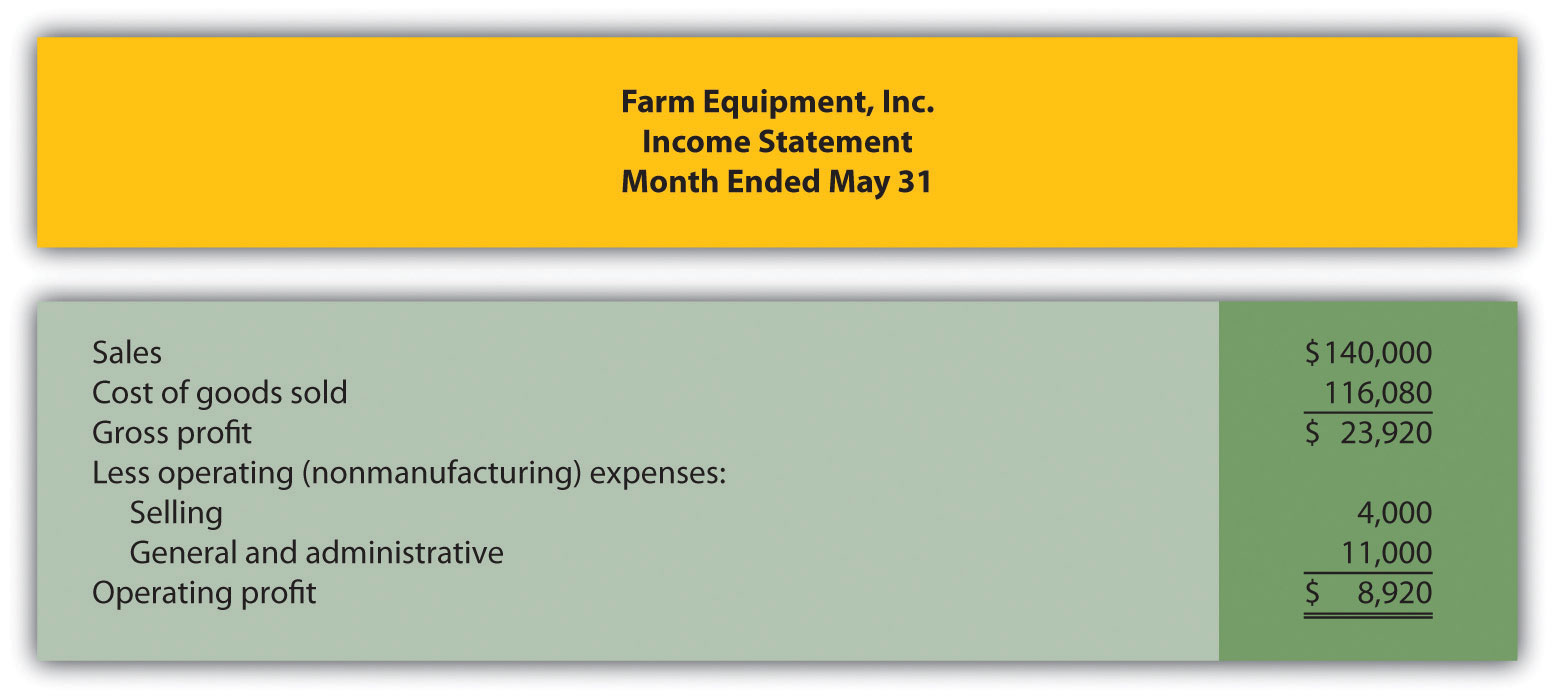

- Assuming selling costs totaled $4,000 and general and administrative costs totaled $11,000 in May, prepare an income statement for Farm Equipment, Inc., for the month. (Assume there is no adjustment to cost of goods sold for underapplied or overapplied overhead.)

Solutions to Review Problem 2.5

-

-

*$161,200 comes from the total for direct materials in part a.

*$33,100 comes from the total for direct labor in part a.

*$52,960 comes from the total for manufacturing overhead in part a.

- Farm Equipment, Inc., made $23,920 in gross profit from the sale of job 1 ($23,920 = $140,000 revenue – $116,080 cost).

-

End-of-Chapter Exercises

Questions

- Describe the characteristics of companies likely to use a job costing system. Explain how these characteristics differ from companies likely to use a process costing system.

- What information is included on the materials requisition form?

- What is the purpose of a job cost sheet? Describe the information typically included on a job cost sheet.

- What information is included on a timesheet?

- What is the purpose of using a predetermined overhead rate?

- Review Note 2.23 "Business in Action 2.1" Explain why Boeing likely uses a job costing system. How does the information that comes from a job costing system help Boeing make better decisions?

- What is a normal costing system, and why do companies tend to use a normal costing system to apply overhead to jobs rather than using actual overhead costs?

- Describe the two important factors in selecting an overhead allocation base.

- What cost information is recorded on the debit side of the manufacturing overhead account, and what information is recorded on the credit side?

- When is manufacturing overhead underapplied? When is it overapplied?

- What two options are available when closing the manufacturing overhead account at the end of the period, depending on the significance of the balance?

- How might a job costing system used by a service organization differ from a job costing system used by a manufacturing organization?

- Review Note 2.27 "Business in Action 2.2" Why is it important for movie studios to have accurate costs for each movie produced?

- How does a job costing system help a company evaluate the profitability of jobs?

Brief Exercises

- Product Costs at Custom Furniture Company. Refer to the dialogue between Dan and Leslie at Custom Furniture Company that appears at the beginning of the chapter. What is Dan concerned about, and how did Leslie propose to help?

-

Job Costing Versus Process Costing. Indicate whether each of the firms listed in the following would use job costing or process costing.

- Oil refinery

- Builder of pools

- Cereal producer

- Legal firm

- Upholstery repair shop

- Sport drink producer

- Toner cartridge producer

- Landscape design firm

-

Job Costing Versus Process Costing. Indicate whether each of the firms listed in the following would use job costing or process costing.

- Custom home builder

- Dairy farm

- Surgical unit of hospital

- Candy bar producer

- Auto body repair shop

- Producer of basketballs

- Producer of T-shirts

- Plumber

-

Recording Purchase and Transfer of Raw Materials in T-Accounts. The following transactions occurred during the month of October:

October 5 Raw materials totaling $15,000 were purchased on account. October 8 Direct materials totaling $6,000 were placed in production. October 10 Indirect materials totaling $1,000 were placed in production. Required:

- Set up T-accounts for raw materials inventory, work-in-process inventory, manufacturing overhead, and accounts payable.

- Use the T-accounts established in part a to record the transactions for October.

- Calculating Predetermined Overhead Rate. Manufacturing overhead costs totaling $1,000,000 are expected for this coming year. The company also expects to use 20,000 in direct labor hours. Calculate the predetermined overhead rate and provide a one-sentence description of how the rate will be used in a job costing system.

-

Service Organization Accounts. Provide the account name commonly used by service companies for each of the following accounts used in a manufacturing environment.

- Raw materials inventory

- Work-in-process inventory

- Finished goods inventory

- Cost of goods sold

- Manufacturing overhead

- Evaluating Profitability of Jobs. Refer to the job cost information in Figure 2.10 "Job Cost Estimates Versus Actual Results for Custom Furniture Company". Why is Custom Furniture Company comparing estimated product costs to actual product costs for each of the three jobs? Briefly summarize the results of this comparison.

Exercises: Set A

-

Raw Materials Inventory Journal Entries. The balance in Sedona Company’s raw materials inventory account was $110,000 at the beginning of September. Raw materials purchased during the month totaled $50,000. Sedona used $17,000 in direct materials and $8,000 in indirect materials for the month.

Required:

-

Prepare separate journal entries to record the following items:

- Raw materials purchased for the month, assuming all purchases were on account

- The transfer of direct materials into production

- The transfer of indirect materials into production

- Prepare a T-account for raw materials inventory and include the beginning balance for September. Post the appropriate items from the journal entries in part a to this account, and calculate the ending balance in raw materials inventory.

-

-

Work-in-Process Inventory Journal Entries. The balance in Reid Company’s work-in-process inventory account was $300,000 at the beginning of March. Manufacturing costs for the month are as follows:

Direct materials $ 40,000 Direct labor $ 70,000 Manufacturing overhead applied $200,000 Cost of goods manufactured $290,000 Required:

-

Prepare separate journal entries to record the following items. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- Direct materials placed in production for the month

- Direct labor used during the month, assuming employees will be paid next month

- Manufacturing overhead applied for the month

- Transfer of cost of goods manufactured to finished goods

- Prepare a T-account for Work-in-process inventory and include the beginning balance for March. Post the appropriate items from the journal entries in part a to this account, and calculate the ending balance in work-in-process inventory.

-

-

Cost of Goods Sold Journal Entries. The balance in Blue Oak Company’s finished goods inventory account was $25,000 at the beginning of September. Cost of goods manufactured for the month totaled $17,000, and cost of goods sold totaled $14,000.

Required:

-

Prepare separate journal entries to record the following items. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- Cost of goods manufactured for the month

- Cost of goods sold for the month

- Prepare a T-account for finished goods inventory and include the beginning balance for September. Post the appropriate items from the journal entries in part a to this account, and calculate the ending balance in finished goods inventory.

-

-

Income Statement (with cost of goods sold adjustment). Rambler Company had the following activity for the year ended December 31.

Sales revenue $2,050,000 Selling expenses $ 575,000 General and administrative expenses $ 330,000 Cost of goods sold (before adjustment) $ 700,000 Underapplied overhead $ 23,000 Required:

Prepare an income statement for year ended December 31.

-

Manufacturing Overhead Allocation Base and Calculating the Cost of Jobs. Pyramid Company expects to incur $3,000,000 in manufacturing overhead costs this year. During the year, it expects to use 40,000 direct labor hours at a cost of $600,000 and 80,000 machine hours.

Required:

- Prepare a predetermined overhead rate based on direct labor hours, direct labor cost, and machine hours.

- Why might Pyramid Company prefer to use machine hours to allocate manufacturing overhead?

- Using each of the predetermined overhead rates calculated in part a and the data that follows for job 128, determine the cost of job 128.

Direct materials $6,000 Direct labor $4,000 (200 hours at $15 per hour) + (100 hours at $10 per hour) Machine time 700 hours

Exercises: Set B

-

Raw Materials Inventory Journal Entries. The balance in Clay Company’s raw materials inventory account was $45,000 at the beginning of April. Raw materials purchased during the month totaled $55,000. Clay used $48,000 in direct materials and $14,000 in indirect materials for the month.

Required:

-

Prepare separate journal entries to record the following items:

- Raw materials purchased for the month, assuming all purchases were on account

- The transfer of direct materials into production

- The transfer of indirect materials into production

- Prepare a T-account for raw materials inventory and include the beginning balance for April. Post the appropriate items from the journal entries in part a to this account, and calculate the ending balance in raw materials inventory.

-

-

Work-in-Process Inventory Journal Entries. The balance in the work-in-process inventory account of Verdi Production, Inc., was $900,000 at the beginning of May. Manufacturing costs for the month are as follows:

Direct materials $ 340,000 Direct labor $ 810,000 Manufacturing overhead applied $ 660,000 Cost of goods manufactured $1,960,000 Required:

-

Prepare separate journal entries to record the following items. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- Direct materials placed in production for the month

- Direct labor used during the month, assuming employees will be paid next month

- Manufacturing overhead applied for the month

- Transfer of cost of goods manufactured to finished goods

- Prepare a T-account for work-in-process inventory and include the beginning balance for May. Post the appropriate items from the journal entries in part a to this account, and calculate the ending balance in work-in-process inventory.

-

-

Cost of Goods Sold Journal Entries. The balance in Posada Company’s finished goods inventory account was $650,000 at the beginning of March. Cost of goods manufactured for the month totaled $445,000, and cost of goods sold totaled $470,000.

Required:

-

Prepare separate journal entries to record the following items. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- Cost of goods manufactured for the month

- Cost of goods sold for the month

- Prepare a T-account for finished goods inventory and include the beginning balance for March. Post the appropriate items from the journal entries in part b to this account, and calculate the ending balance in finished goods inventory.

-

-

Income Statement (with cost of goods sold adjustment). Statton Company had the following activity for the year ended December 31.

Sales revenue $4,000,000 Selling expenses $ 825,000 General and administrative expenses $ 470,000 Cost of goods sold (before adjustment) $1,900,000 Overapplied overhead $ 109,000 Required:

Prepare an income statement for year ended December 31.

-

Manufacturing Overhead Allocation Base and Calculating the Cost of Jobs. Elko Company expects to incur $800,000 in manufacturing overhead costs this year. During the year, it expects to use 10,000 direct labor hours at a cost of $200,000 and 4,000 machine hours.

Required:

- Prepare a predetermined overhead rate based on direct labor hours, direct labor cost, and machine hours.

- Why might Elko Company prefer to use direct labor hours or direct labor costs, rather than machine hours, to allocate manufacturing overhead?

- Using each of the predetermined overhead rates for Elko Company calculated in part a and the data that follows for job 15B, determine the cost of job 15B.

Direct materials $1,750 Direct labor $860 (30 hours at $12 per hour) + (50 hours at $10 per hour) Machine time 20 hours

Problems

-

Actual and Applied Manufacturing Overhead. Marine Products, Inc., incurred the following actual overhead costs for the month of June.

Indirect materials $20,000 Indirect labor $18,000 Rent $ 3,000 Equipment depreciation $ 6,500 Overhead is applied based on a predetermined rate of $12 per machine hour, and 5,100 machine hours were used during June.

Required:

- Prepare a journal entry to record actual overhead costs for June. Assume that labor costs will be paid next month and that rent was prepaid.

- Prepare a journal entry to record manufacturing overhead applied to jobs during June.

- Create a T-account for manufacturing overhead, post the appropriate information from parts a and b to this account, and calculate the ending balance.

- Is manufacturing overhead overapplied or underapplied? Using the balance in the manufacturing overhead account calculated in part c, prepare the journal entry to close manufacturing overhead to cost of goods sold.

-

Actual and Applied Manufacturing Overhead. Quincy Company incurred the following actual overhead costs for the month of February.

Indirect materials $335,000 Indirect labor $275,000 Factory depreciation $ 18,000 Factory utilities $ 9,500 Overhead is applied based on a predetermined rate of $2 per direct labor dollar (200 percent of direct labor cost), and direct labor costs were $300,000 for the month.

Required:

- Prepare a journal entry to record actual overhead costs for February. Assume indirect labor costs and utilities will be paid next month.

- Prepare a journal entry to record manufacturing overhead applied to jobs during February.

- Create a T-account for manufacturing overhead, post the appropriate information from parts a and b to this account, and calculate the ending balance.

- Is manufacturing overhead overapplied or underapplied? Using the balance in the manufacturing overhead account calculated in part c, prepare the journal entry to close manufacturing overhead to cost of goods sold.

-

Calculating the Cost of Jobs, Making Journal Entries, and Preparing an Income Statement. Racing Bikes, Inc., produces custom bicycles for professional racers. Each bike is built to customer specifications. During July, its first month of operations, Racing Bikes began production of four customer orders—jobs 1 through 4. The following transactions occurred during July.

- Purchased bike parts totaling $14,400

-

Processed material requisitions for the following items:

-

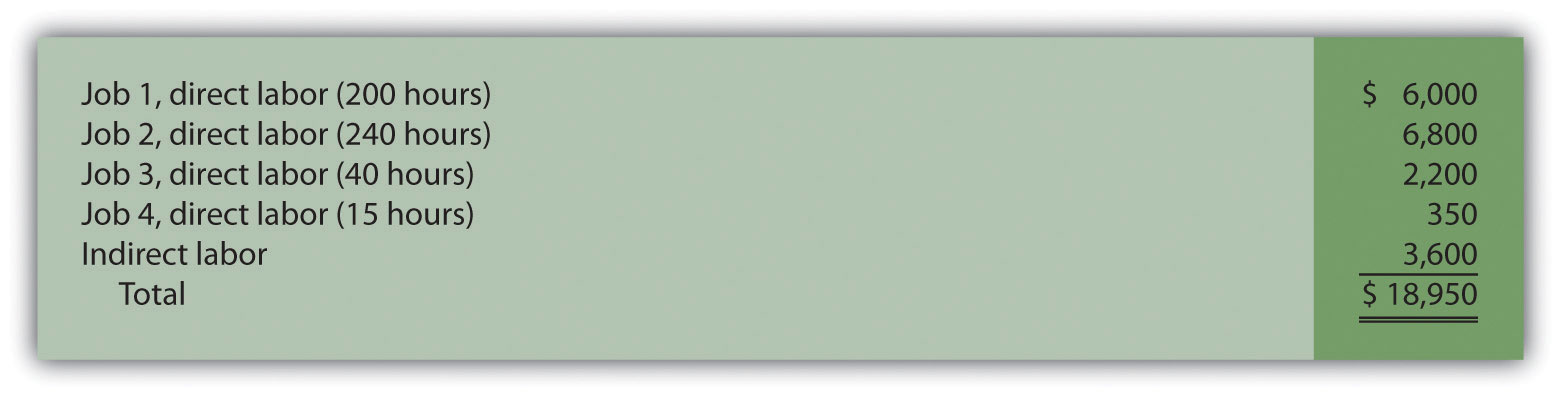

Processed timesheets showing the following:

- Applied overhead using a predetermined rate of $30 per direct labor hour

- Completed and transferred to finished goods jobs 1, 2, and 3

- Delivered jobs 1 and 2 to customers, billing them $6,000 for job 1 and $3,500 for job 2 (Hint: Two entries are required—one for the cost of the goods and another for the revenue.)

Required:

- Calculate the production costs incurred in July for each of the four jobs.

- Make the appropriate journal entry for each transaction described previously (1 through 6). Assume all payments will be made next month. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- How much gross profit did Racing Bikes, Inc., earn from the sale of job 2?

- Assume selling costs totaled $1,000 and that general and administrative costs totaled $2,200. Prepare an income statement for Racing Bikes for the month of July. (Assume there is no adjustment to cost of goods sold for underapplied or overapplied overhead.)

-

Calculating the Cost of Jobs, Making Journal Entries, and Preparing an Income Statement. Classic Boats, Inc., produces custom wood boats. Each boat is built to customer specifications. During April, its first month of operations, Classic Boats began production of three customer orders—jobs 1 through 3. The following transactions occurred during April.

- Purchased production materials totaling $225,000

-

Processed material requisitions for the following items:

-

Processed timesheets showing the following:

- Applied overhead using a predetermined rate of 160 percent of direct labor cost

- Completed job 1 and transferred it to finished goods

- Delivered job 1 to the customer and billed her $70,000. (Hint: Two entries are required—one for the cost of the goods and another for the revenue.)

Required:

- Calculate the production costs incurred in April for each of the three jobs.

- Make the appropriate journal entry for each of the six transactions described previously. Assume all payments will be made next month. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- How much gross profit did Classic Boats earn from the sale of job 1?

- Assume selling costs totaled $2,000 and general and administrative costs totaled $5,500. Prepare an income statement for Classic Boats for the month of April. (Assume there is no adjustment to cost of goods sold for underapplied or overapplied overhead.)

-

Calculating the Cost of Jobs and Making Journal Entries for a Service Company. Sampson & Associates provides accounting services. It began jobs 1 through 3 in the first week of January. The following transactions occurred that week.

- Purchased supplies on account totaling $1,500

- Used supplies totaling $800 for various jobs

-

Processed timesheets showing the following:

- Applied overhead using a predetermined rate of $10 per direct labor hour.

- Completed job 1 and billed the customer $3,000. (Hint: Two entries are required—one for the cost of services and another for revenue.)

Required:

- Calculate the costs incurred in January for each of the three jobs.

- Make the appropriate journal entry for each item described previously. Assume all payments will be made next month. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- How much gross profit did Sampson & Associates earn from job 1?

-

Calculating the Cost of Jobs and Making Journal Entries for a Service Company. Management Consulting, Inc., provides consulting services and began operations on September 1. It began jobs 1 through 4 during the first half of September. The following transactions occurred during that time.

- Purchased supplies on account totaling $6,000

- Used supplies totaling $3,200 for various jobs

-

Processed timesheets showing the following:

- Applied overhead using a predetermined rate of 120 percent of direct labor cost

- Completed jobs 1 and 2 and billed the customers $20,000 and $21,000, respectively. (Hint: Two entries are required—one for the cost of services and another for revenue.)

Required:

- Calculate the costs incurred in September for each of the four jobs.

- Make the appropriate journal entry for each item described previously. Assume all payments will be made next month. (Hint: Use Figure 2.7 "Custom Furniture Company’s Journal Entries for May" as a guide.)

- How much gross profit did Management Consulting, Inc., earn from job 1 and job 2?

- What is the amount in work in process at the end of the first half of September?

-

Closing Manufacturing Overhead: Two Approaches. Olympia Company incurred actual manufacturing overhead costs of $630,000 during the year ended December 31, 2012. A total of $570,000 in overhead was applied to jobs. At December 31, 2012, work-in-process inventory totals $200,000, and finished goods inventory totals $400,000. Cost of goods sold before adjustments totals $1,400,000 for the year.

Required:

- Is overhead underapplied or overapplied?

- Close the manufacturing overhead account, assuming the balance is immaterial.

- Close the manufacturing overhead account, assuming the amount is material.

-

Closing Manufacturing Overhead: Two Approaches. Placer Company incurred actual manufacturing overhead costs of $260,000 during the year ended December 31, 2012. A total of $350,000 in overhead was applied to jobs. At December 31, 2012, work-in-process inventory totals $100,000, and finished goods inventory totals $300,000. Cost of goods sold before adjustments totals $600,000 for the year.

Required:

- Is overhead underapplied or overapplied?

- Close the manufacturing overhead account, assuming the balance is immaterial.

- Close the manufacturing overhead account, assuming the amount is material.

One Step Further: Skill-Building Cases

-

Ethics: Shifting Hours Using Job Costing. Shawney Accountancy Corporation provides accounting services. It uses a job costing system to track each client’s revenues and costs. The firm is currently working on two jobs. The first job, preparing tax returns for Bantem Corporation, was bid at $25,000 and had budgeted costs of $18,000. The second job, performing a review of internal controls for Maxum Company, was bid at 50 percent above actual costs. The following conversation took place between Kelly (a manager) and Ron (senior staff working for Kelly).

Kelly: Ron, I just reviewed timesheets for the two jobs we’re working on, and it appears we are quickly approaching the budget of $18,000 for the Bantem job. Ron: Yes, we’re having trouble completing the Bantem job in the hours budgeted. Kelly: This is the first year on the Bantem job, and budgeting for first-year clients is always difficult. Ron: I’m sure we can retain this job next year with a little bump in the bid—perhaps to $29,000. Kelly: That’s fine for next year, but I have to answer to my boss for this year’s results. Why don’t we take some of the pressure off by charging some time from the Bantem job to the internal control project we have with Maxum Company? We’re under budget with the Maxum job, and they are paying us based on actual costs plus a 50 percent markup. Ron: Can we do that? Kelly: We don’t do it often, but in cases like this, we have to get creative. Required:

- Why is there an incentive to inflate the hours charged to the Maxum job?

- What should Ron do? (You may want to refer to the IMA’s ethical standards discussed in Chapter 1 "What Is Managerial Accounting?".)

-

Internet Project: Automation and Overhead Allocation. Over the past several decades, manufacturing companies have tended to move away from direct labor and more toward automation (i.e., using machinery rather than people to produce products).

Required:

- Use the Internet to find several examples of companies that have made the shift toward an automated production environment. Write a one-page summary of your findings, and include specific information indicating what type of automation is being used.

- How might this shift to automation affect the allocation base used to allocate overhead to products?

-

Group Project: Labor Costs at General Motors and Toyota. Both General Motors (GM) and Toyota have production facilities in Texas. GM’s plant was built in 1956 on a 249-acre site and has since undergone billions of dollars in renovations. Toyota’s plant was built in 2006 on 2,000 acres. Each plant has a production capacity of 200,000 vehicles per year. GM averages close to 22 assembly labor hours per vehicle (no data on labor hours per vehicle are available for Toyota). The labor cost per vehicle is $1,800 for GM, which uses a unionized labor force, and $800 for Toyota, which uses nonunion labor. (Based on Lee Hawkins Jr. and Norihiko Shirouzu, “A Tale of Two Auto Plants,” Wall Street Journal, May 24, 2006.)

Required:

Form groups of two to four students and respond to the following items:

- Provide at least two reasons for the significant difference in assembly labor cost per vehicle for GM and Toyota.

- What other production costs should be considered in evaluating the efficiency of each plant?

Comprehensive Cases

-

Journal Entries, Closing Manufacturing Overhead, and Preparing an Income Statement. Benning, Inc., is a defense contractor that uses job costing. Because the firm uses a perpetual inventory system, the three supporting schedules to the income statement (the schedule of raw materials placed in production, the schedule of cost of goods manufactured, and the schedule of cost of goods sold) are not necessary. Inventory account beginning balances at January 1, 2012, are listed as follows.

Raw materials inventory $ 500,000 Work-in-process inventory $ 700,000 Finished goods inventory $1,800,000 You will be recording the following transactions, which summarize the activities that occurred during the year ended December 31, 2012:

- Raw materials were purchased for $300,000 on account.

- Raw materials totaling $420,000 were placed in production, $60,000 for indirect materials and $360,000 for direct materials.

- The raw materials purchased in transaction 1 were paid for.

- A total cost of $800,000 for direct labor, shown on the timesheets, was recorded as wages payable.

- Production supervisors and other indirect labor working in the factory were owed $540,000, recorded as wages payable.

- Wages owed, totaling $1,200,000, were paid. (These wages were previously recorded correctly as wages payable.)

-

The costs listed in the following related to the factory were incurred during the period. (Hint: Record these items in one entry with one debit to manufacturing overhead and four separate credits):

Building depreciation $580,000 Insurance (prepaid during 2012, now expired) $220,000 Utilities (on account) $ 80,000 Maintenance (paid cash) $440,000 - Manufacturing overhead was applied at a rate of $20 per machine hour, and 90,000 machine hours were utilized during the year. (Hint: No need to calculate the predetermined overhead rate since it is already given to you here.)

- Miscellaneous selling costs totaling $430,000 were paid. These costs were recorded in an account called selling expenses.

- Miscellaneous general and administrative costs totaling $265,000 were paid. These costs were recorded in an account called G&A expenses.

- Goods costing $2,030,000 (per the job cost sheets) were completed and transferred out of work-in-process inventory.

- Goods were sold on account for $3,800,000.

- The goods sold in transaction 12 had a cost of $2,570,000 (per the job cost sheets).

- Payments totaling $3,300,000 from credit customers related to transaction 12 were received.

Required:

- Prepare T-accounts for raw materials inventory, work-in-process inventory, finished goods inventory, manufacturing overhead, and cost of goods sold. Enter the beginning balances for the inventory accounts. (Manufacturing overhead and cost of goods sold are temporary accounts and thus do not have a beginning balance.)

- Prepare a journal entry for each transaction from 1 through 14 in a format like the one in Figure 2.7 "Custom Furniture Company’s Journal Entries for May", and where appropriate, post each entry to the T-accounts set up in requirement a. Note that these entries reflect the flow of costs through the inventory and cost of goods sold accounts for the year. Label each entry in the T-accounts by transaction number, include a short description (e.g., direct materials and manufacturing overhead applied), and total each T-account.

- Based on the balance in the manufacturing overhead account prepared in requirement b, prepare a journal entry to close the manufacturing overhead account to cost of goods sold.

- Prepare an income statement for the year ended December 31, 2012. Remember to adjust cost of goods sold for any underapplied or overapplied overhead.

- Why is cost of goods sold adjusted upward on the income statement?

-

Journal Entries, Closing Manufacturing Overhead, and Preparing an Income Statement. Sierra Nursery Company grows a variety of plants and sells them to local nurseries. Raw materials consist of such items as seeds and the fertilizer required to grow plants from the seedling stage to a viable, saleable plant. Sierra Nursery uses a job costing system to track revenues and costs associated with customer orders. Because the firm uses a perpetual inventory system, the three supporting schedules to the income statement (the schedule of raw materials placed in production, the schedule of cost of goods manufactured, and the schedule of cost of goods sold) are not necessary. Inventory account beginning balances at January 1, 2012, are as follows:

Raw materials inventory $50,000 Work-in-process inventory $60,000 Finished goods inventory $90,000 You will be recording the following transactions, which summarize the activities that occurred during the year ended December 31, 2012:

- Raw materials were purchased for $30,000 on account.

- Raw materials totaling $41,000 were placed in production, $5,000 for indirect materials and $36,000 for direct materials.

- The raw materials purchased in transaction 1 were paid for.

- A total cost of $140,000 for 9,000 hours of direct labor, shown on the timesheets, was recorded as wages payable.

- Production supervisors and other indirect labor working in the nursery were owed $134,000, recorded as wages payable.

- Wages owed totaling $180,000 were paid. (These wages were previously recorded correctly as wages payable.)

-

The costs listed in the following related to the nursery were incurred during the period. (Hint: Record these items in one entry with one debit to manufacturing overhead and four separate credits):

Equipment depreciation $22,000 Rent (prepaid during 2012) $36,000 Utilities (on account) $33,000 Maintenance (paid cash) $19,000 - Manufacturing overhead was applied at a rate of $30 per direct labor hour. (Hint: No need to calculate the predetermined overhead rate since it is already given to you here.)

- Miscellaneous selling costs totaling $63,000 were paid. These costs were recorded in an account called selling expenses.

- Miscellaneous general and administrative costs totaling $18,000 were paid. These costs were recorded in an account called G&A expenses.

- Goods costing $478,000 (per the job cost sheets) were completed and transferred out of work-in-process inventory.

- Goods were sold on account for $780,000.

- The goods sold in transaction 12 had a cost of $415,000 (per the job cost sheets).

- Payments totaling $380,000 from credit customers related to transaction 12 were received.

Required:

- Prepare T-accounts for raw materials inventory, work-in-process inventory, finished goods inventory, manufacturing overhead, and cost of goods sold. Enter the beginning balances for the inventory accounts. (Manufacturing overhead and cost of goods sold are temporary accounts and thus do not have a beginning balance.)

- Prepare a journal entry for each transaction from 1 through 14 in a format like the one in Figure 2.7 "Custom Furniture Company’s Journal Entries for May", and where appropriate, post each entry to the T-accounts set up in requirement a. Note that these entries reflect the flow of costs through the inventory and cost of goods sold accounts for the year. Label each entry in the T-accounts by transaction number, include a short description (e.g., direct materials and manufacturing overhead applied), and total each T-account.

- Based on the balance in the manufacturing overhead account prepared in requirement b, prepare a journal entry to close the manufacturing overhead account to cost of goods sold.

- Prepare an income statement for the year ended December 31, 2012. Remember to adjust cost of goods sold for any underapplied or overapplied overhead.

- Why is cost of goods sold adjusted downward on the income statement?